Preparing for passing $10 billion mark

SNL Report: Dodd-Frank threshold becoming familiar tale for banks, regulators. MOE strategy popular

- |

- Written by SNL Financial

SNL Financial, part of S&P Global Market Intelligence, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial, part of S&P Global Market Intelligence, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Kiah Lau Haslett and Zain Tariq, SNL Financial staff writers

Almost six years into the Dodd-Frank Act, banks crossing the $10 billion asset threshold are increasingly well prepared, thanks to well laid-out expectations from the OCC.

That is not to say that the process has become any cheaper or less rigorous since the passage of the monumental finance reform law in 2010, but the process has become a more familiar and standard narrative for those in the industry and for the regulators assisting them with the transition.

Bill Haas, deputy comptroller for mid-sized bank supervision, told S&P Global Market Intelligence that the OCC has early conversations with mid-sized community banks about strategy and growth and considerations to capital planning, operational risk, and stress testing. For banks closer to the $10 billion asset threshold, regulators also outline the OCC's heightened risk management expectations for banks.

"From our mindset, crossing the $10 billion threshold isn't and shouldn't be all that daunting," he said. "Part of that engagement is to reduce the anxiety level and provide clarity and transparency over what the expectations would be, but again it's the planning ahead and thinking ahead [for institutions] that is really critical."

A big deal

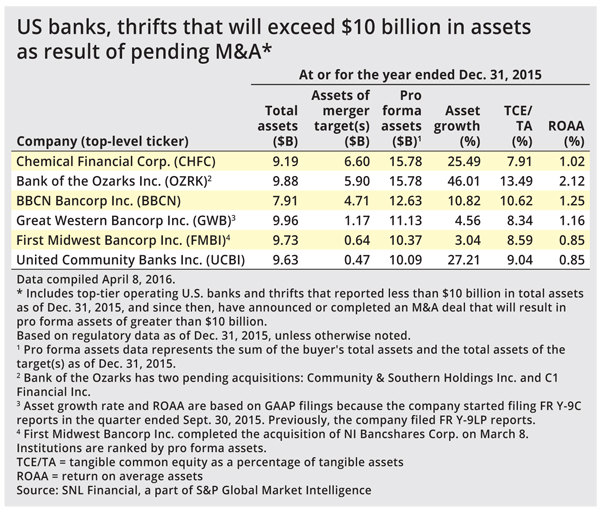

Strategic planning for $10 billion remains pivotal for growing community banks, given that mergers and acquisitions remain a popular method for banks seeking to cross it. There are currently five banks that will exceed $10 billion in assets with the assistance of a pending deal, according to S&P Global Market Intelligence.

Two of the deals are being touted by management as mergers of equals. Management of Troy, Mich.-based Talmer Bancorp Inc. did not shop the bank around for a better price or different partner before agreeing to merge with Midland, Mich.-based Chemical Financial Corp., according to President and CEO David Provost, speaking on the Jan. 26 merger conference call.

The deal will hurdle Chemical, which had $9.19 billion at the end of 2015, across the threshold to more than $15 billion at the pro-forma company. But it also spares Talmer, which had $6.60 billion at the end of 2015, the trouble of facing its own $10 billion dilemma if it had remained independent.

The pro forma company expects to incur pretax Durbin costs of $5 million in 2017 and $10 million in 2018 associated with the legislative reduction of interchange income from debit cards at banks with more than $10 billion. The pro forma company also expects annual pretax incremental cost of $2 million in compliance costs related to advanced supervisory requirements, mainly the FDIC insurance and stress testing. Chemical Financial reported $13.90 million in credit card and bank card interchange fees in 2015 while Talmer reported $5.81 million in interchange fees, based on data filed in the Form Y-9C with regulators.

Korean banks BBCN Bancorp Inc. and Wilshire Bancorp Inc. are also leveraging the MOE structure to cross $10 billion. BBCN Chairman, President, and CEO Kevin Kim said the deal will require the banks to enhance their existing infrastructure and create a more comprehensive and defined risk management framework and process, according to the bank's December 2015 call announcing the deal.

Kim also said the banks would begin planning their regulatory road map "immediately." The pro forma company is expected to have a projected loss in revenue of about $1.5 million, said BBCN CFO Douglas Goddard; he attributed the lower figure to low penetration of debit card products in BBCN's deposit base. BBCN Bancorp and Wilshire Bancorp did not disclose total interchange fees in their Form Y-9Cs for 2015. Banks only have to report the metric if it comprises a high enough threshold of noninterest income.

Bank of the Ozarks Inc. embodies another approach, stringing together the acquisitions of Community & Southern Holdings Inc. and C1 Financial Inc. in the latter part of 2015 to heartily jump over the $10 billion threshold in the first quarter. The bank finished 2015 with assets of $9.88 billion, delaying the impact of Durbin until July 2017, said Chairman and CEO George Gleason during the fourth-quarter 2015 earnings call.

The bank expects to lose $5.35 million annually because of Durbin; management also expects annualized additional compliance costs to increase by about $3.4 million in 2016 and $1.9 million in 2017. Bank of the Ozarks did not disclose total interchange fees in 2015. Banks only have to report the metric if it comprises a high enough threshold of noninterest income. Community & Southern Holdings reported $248,000 in credit card and bank card interchange fees in 2015 while C1 Financial reported $1.262 million in interchange fees in 2015, based on data filed in the Form Y-9C with regulators.

A long, costly road

Some executives at banks approaching $10 billion in assets have publicly said that they have been planning for the threshold for years, in an attempt to bake in expenses and show regulators that they are prepared for heightened regulatory scrutiny.

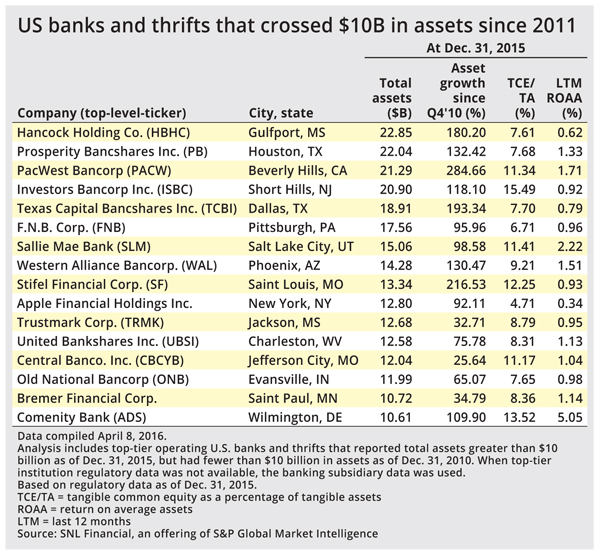

Evansville, Ind.-based Old National Bancorp assembled a "$10 billion readiness" project in 2012 to highlight internal areas where operations needed to be strengthened or improved; it breached the threshold when it recorded $10.39 billion in assets in the second quarter of 2014. The bank had $11.99 billion in assets at the end of 2015 and has a pending deal with Madison, Wis.-based Anchor BanCorp Wisconsin Inc., which had $2.25 billion in assets at the end of 2015.

Old National's Chief Risk Officer Candice Rickard said the bank focused on governance, staffing and systems at the beginning of its preparations, including the creation of a risk appetite statement. Over the quarters, changes included the bank's DFAST submission process, shifting methodologies that the bank used to calculate its allowance for loan and lease losses, and upgrading its asset-liability management software.

It also hired staff that had a strong statistics background in the banking space. It also focused on enhancing its BSA-AML, HMDA, and fair-lending compliance. Old National's bank card and credit card interchange fee income was $24.2 million for 2014, according to S&P Global Market Intelligence; in 2015, its interchange fees sank to $19.7 million.

"It's expensive. You have to be prepared to deal with that," said CFO Chris Wolking.

The regulators

Crossing $10 billion in assets denotes a shift in a bank's relationship with its regulators, including the notable additions of the Consumer Financial Protection Bureau as a direct examiner and the Dodd-Frank Stress Tests.

The OCC currently offers voluntary submission into the heightened supervision standards to institutions near or just over the threshold, in advance of a formal filing; it was offered to six national banks and thrifts in 2016, with four accepting the opportunity and two deferring until next year, Haas said.

Old National participated in the unofficial voluntary submission in March 2015, which allowed it to interface with the OCC and ensure it was making appropriate progress toward its official DFAST submission due in July. Even though the bank was not fully ready for the process, the OCC gave the bank feedback that contained areas that could potentially become "Matters Requiring Attention" in an official filing, Old National's Rickard said.

She added that the bank has had only limited interactions with the CFPB, including a cursory overview of the bank, but that they will be conducting an on-site visit later.

That seems in line with standard protocol, according to emailed comments from Samuel Gilford, CFPB spokesperson. He said generally the regional CFPB manager will reach out to an institution several months before the institution would fall under the bureau's supervisory jurisdiction, with talks focusing on the examination process, risk-based prioritization and expectations around and importance of "robust" compliance management systems, among other things. He said there is no standard for when the CFPB will conduct its first exam at institutions that have recently fallen under its jurisdiction.

"We prioritize our exams based on our risk assessments, looking across both bank and nonbank markets. To that end, we also review banks to get a baseline look at their compliance management systems and other major product areas," Gilford wrote, adding that the regulator looks at product line based on potential to cause consumer harm, the size of the product market, the entity's market share and risks that are inherent in its operations and offerings. "We prioritize relatively larger players with a more dominant presence given their ability to impact more consumers than relatively small players."

This article originally appeared on SNL Financial’s website under the title,"$10 billion becoming familiar tale for banks, regulators"

Tagged under Management, CSuite, Community Banking, M&A, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story