Bank M&A falls in ’16, a rebound in question

Population of buyers of smaller banks shrinking

- |

- Written by S&P Global Market Intelligence

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

By Nathan Stovall and Zander Luke, S&P Global Market Intelligence staff writers

Bank M&A activity has slowed fairly considerably year, and while the rationale for deals still exists, few expect a material pickup anytime soon.

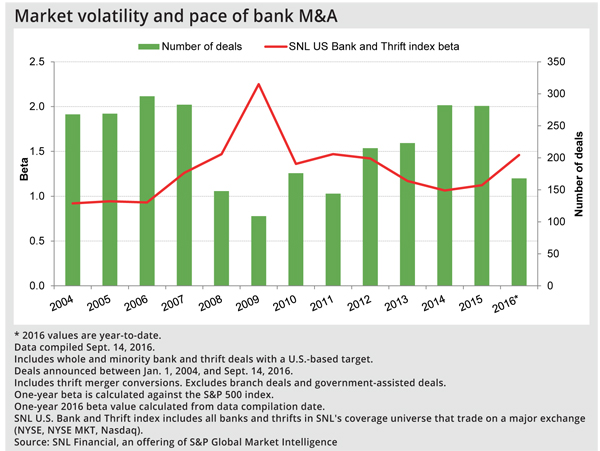

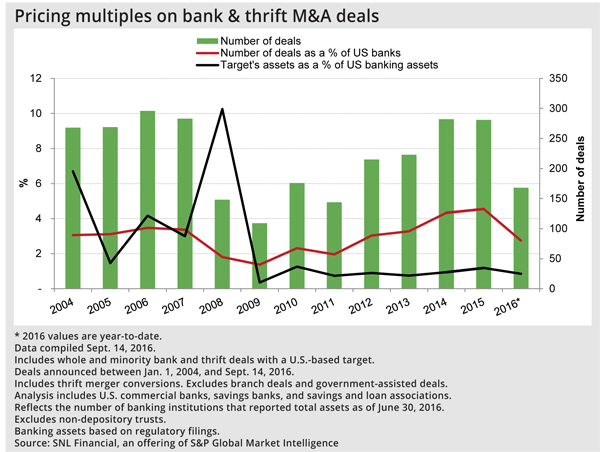

Through mid-September, there have been 168 announced bank deals in 2016, or 238 annualized, down close to 15% from the 287 deals announced in 2015. (S&P Global published this article on Oct. 3.)

This year, announced bank deals have equated to nearly 2.8% of banks in the industry, the lowest level of consolidation since 2011. In 2015, announced bank deals equated to nearly 4.6% of banks in the industry, the highest percentage of consolidation since at least 2004. From 2004 to 2013, the measure ranged from 1.4% to 3.4%.

Value of M&A currency slips

The slowdown in bank M&A activity has followed erosion in bank stock currencies. As buyers' capacity to pay waned, deal multiples dropped in kind.

Bank stocks took considerable hits early this year, largely due to macroeconomic concerns. As oil prices headed lower, fears that a global economic slowdown could lead to a U.S. recession weighed on the market. Some investors also grew concerned that the credit cycle could be turning.

The SNL Bank & Thrift Index fell as low as 134% of tangible book value in early February but has bounced back since then, rising to roughly 149%. They are still below the levels witnessed at year-end 2015, when the bank group traded at nearly 165% of tangible book value, down slightly from 175% at the close of 2014.

While the bank group has rebounded from the lows in February, the markets have remained fairly volatile. Swings in the market have often stemmed from global events like Brexit and other developments that changed the outlook for interest rates.

The prospect of rate hikes has often led to sell offs in bank stocks, despite many investors arguing that higher rates will offer relief to depressed net interest margins.

As the outlook for rates remains uncertain, so does the forecast for M&A activity. Bank advisers presenting in late September at the 8th annual M&A Symposium hosted by S&P Global Market Intelligence said they do not expect a significant pickup in deals as the pool of buyers could be shrinking while seller expectations remain fairly high.

They said that M&A in Texas, once of a hotbed of deal activity, has slowed notably with decreases in oil prices. Through mid-September, 13 deals surfaced in Texas, representing 7.4% of all U.S. bank deal activity. That is down on an annualized basis from 22 deals in 2015 and 27 deals in 2014, when Texas transactions equated to 7.9% and 9.5% of all U.S. bank deal activity.

Big bank deals scare and to remain so

While 2016 has brought several large deals, those transactions are unlikely to pick up any time soon. Sullivan & Cromwell LLP Senior Chairman H. Rodgin Cohen said at the M&A Symposium that the nation's largest banks remain on the "no buy" list by regulators, keeping the pool of buyers equipped for sizable deals to a minimum.

Five bank deals with values over $1 billion have been announced so far in 2016, flat with the prior year. In each of 2014, 2013 and 2012, just two bank deals with values over $1 billion surfaced, while three deals apiece with values over $1 billion were announced in 2011 and 2010.

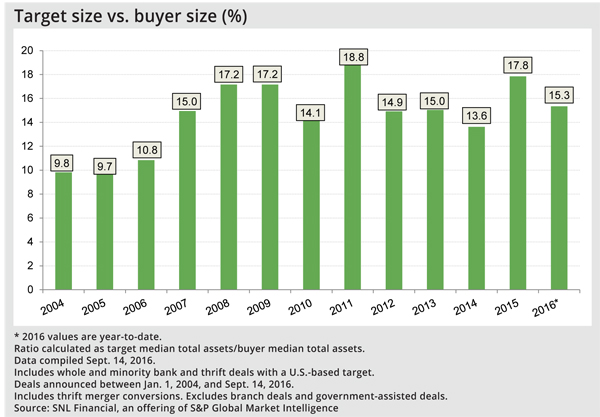

The vast majority of transactions have involved smaller institutions, and that seems unlikely to change soon. There might even be fewer institutions looking to acquire smaller banks since those deals often do not move the needle that much and could prove more trouble than they are worth for some would-be buyers.

Rory McKinney, managing director and co-head of investment banking at D.A. Davidson, said at the M&A Symposium that the buyer landscape represents the biggest threat to bank M&A today, as the universe of potential acquirers of small banks is shrinking.

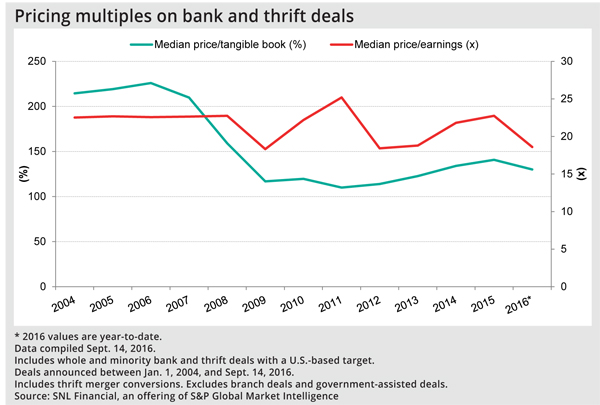

If there are fewer acquirers, it stands to reason that pricing could come under further pressure. Bank deal prices fell to a median of 130.0% of tangible book value and 18.6x earnings through mid-September, compared to 140.7% and 22.8x earnings in 2015, and 134.1% of tangible book and 21.8x in 2014.

Banks that have held off on selling for some time with hopes of fetching higher prices in the future could find themselves disappointed. C.K. Lee, a managing director in the financial institutions group at Commerce Street Capital, encouraged banks to have a sales strategy in place so they can strike the iron while it is hot.

"I think there is a backlog of deals that needs to be cleared and I think it's going to have an impact downward on pricing. A lot of these folks' expectations are unreasonable and I think they're going to get an education," Lee said at the M&A Symposium.

This article originally appeared on S&P Global Market Intelligence’s website under the title, "Bank M&A falls in ’16, a rebound in question"

Tagged under Management, CSuite, Community Banking, M&A,

Related items

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story

- JP Morgan Drops Almost 5% After Disappointing Wall Street

- Banks Compromise NetZero Goals with Livestock Financing

- OakNorth’s Pre-Tax Profits Increase by 23% While Expanding Its Offering to The US

- One in Five Oppose Fed’s Proposed Changes to Regulation II