Balancing business and personal credit risk profiles

Avoid financial storms by multiple views of business borrowers

- |

- Written by Torsten Gerwien, principal business consultant, Experian

In February 2014, Atlanta, Ga., was hit by a powerful snowstorm that caused devastation and panic. Yet, the damage that the city endured was caused less by the storm itself and more by lack of preparation. Many later reported that they never saw it coming, but they could have. Unfortunately, slight variances in weather forecasting (as well as a general misunderstanding of the difference between a storm watch and a storm warning) led to catastrophic traffic jams and statewide gridlock. However, with just slight improvements in forecasting and the ability to get the warning out earlier, Atlanta could have seen a much different result.

For commercial creditors, similar slight improvements in forecasting can lead to better results when managing the credit risk of small-business portfolios. By making a simple adjustment to how they assess risk, commercial creditors can more accurately filter prospective borrowers or be alerted sooner to potential problems.

Historically, when lending to small businesses, many creditors have chosen to review the business-owner’s consumer credit profile to assess credit risk, rather than the business’s credit report.

The familiarity with consumer credit data can lure a lender into complacency: “What additional information can a business credit score provide, anyway?”

It’s true that there is a strong correlation between a business-owner’s consumer-credit profile and their business’s credit profile, causing many lenders to assume that the results of these reviews are interchangeable.

But what about cases where the two profiles aren’t in agreement?

After all, making an incorrect assessment on a small business’s credit risk can cost a creditor thousands—perhaps tens of thousands—of dollars.

A recent Experian study quantified just how important it can be to review both a small firm’s credit profile, as well as its owner’s consumer profile when assessing risk. This can be aided by using a “blended” score, which combines the profile of both a small business and its owners.

Study methodology

To determine the connection between the credit risk of a small business and that of the business’s owner, Experian analyzed data from its Entity Linkage Service, which makes it possible to examine credit histories of both the business itself along with the consumer credit of a business owner.

The study analyzed 80,000 consumer credit profiles that were linked to businesses and tracked the records over a 15-quarter period, from March 2010 to September 2013, in order to observe both good and bad credit behavior.

For its conclusions to be as predictive as possible, the study looked at businesses and their owners who were in good financial health as of March 2010. For the purposes of this study, a “bad business” was determined to be one where at least 50% of outstanding balances were 91-plus-days delinquent. For the owner, at least 35% of outstanding trades were 90-plus-days delinquent.

Where they synch, where they don’t

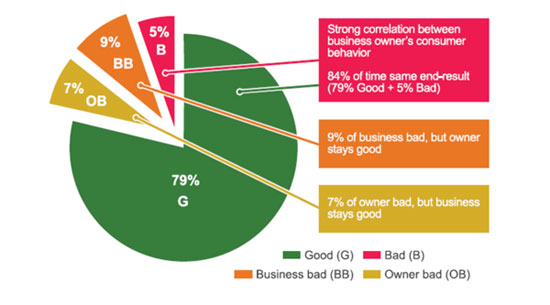

It was determined that in 84% of all cases, a good or bad credit profile for a business was also reflected in the business-owner’s consumer profile. While 84% seems like a significant majority, it seldom meets the standards for risk-management best practices.

Few lenders can afford to be wrong 16% of the time, whether it’s overlooking a prospective client (when the business stays good, but the owner goes bad) or lending to a high-risk borrower (when the business goes bad, but the owner stays good).

Those creditors that understand the slight variances between a business-owner’s credit file and a business’s credit file have an advantage when evaluating credit risk.

Additionally, in 16% of the cases analyzed, the business-owner’s consumer credit profile and the business’s credit profile were not aligned. For example, in 9% of cases, when the business profile became bad, the owner’s profile still remained good. Conversely, in the remaining 7% of credit profiles studied, the business’s credit remained strong, even while the owner’s credit deteriorated.

Early warnings from the personal side

Another notable reason why it’s important to examine both a business credit profile as well as the business owner’s is that at times a creditor can get an early indication that both credit profiles may go bad.

This is understandable as many small-business owners will begin to rely on their personal credit to help keep the business going during troubled times, or conversely, they may choose to tap into their small-business credit to address consumer credit shortfalls. Or personal credit issues may be a distraction from running the business.

The lag time between the two can be substantial, and having access to both scores (or to a blended score) offers lenders an earlier opportunity to intervene when necessary or take preemptive measures as appropriate.

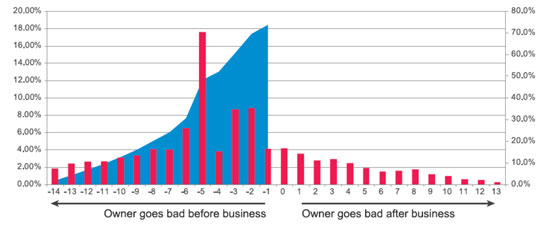

For example, let’s take the 5% of cases when both the business’s and the business owner’s credit profiles went bad. In these cases, the study found there was an advantage to using the business-owner’s consumer profile.

In 74% of the cases where both profiles became derogatory, the owner’s profile went bad prior to the business, indicating that credit grantors need to be particularly vigilant of their extension to that business for the next 18 months.

However, while the owner’s consumer credit report can be a leading indicator when both profiles go bad, the business’s credit profile can also be a leading indicator of risk. In the remaining 26% of cases, a small business begins to show signs of financial hardship before there is any indication on the owner’s consumer profile.

For a larger version, click on the image.

For a larger version, click on the image.

Score as an indicator of a business going bad

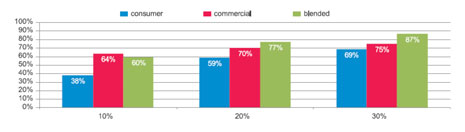

To understand which type of credit score is the leading indicator of a business actually going bad, the study examined three risk scoring models: commercial Intelliscore Plus, blended Intelliscore Plus, and consumer VantageScore.

A blended score has the unique advantage of combining the owner’s consumer and commercial information to get a more comprehensive view of credit behavior for the business. With a blended score, the lender need not determine if one score is better than another.

The study measured the percentage of bad dollars (as measured by dollars 91-plus-days delinquent) captured in the worst scoring 10%, 20%, and 30% of the population by each score.

In practice, this is a critical component to the bottom-line profitability of a creditor. Over the rolling 12-month observation window, a total balance of $32.4 million became 91-plus-days delinquent. By observing the worst-scoring 30%, the blended model was able to capture 5.9 million more bad dollars and 3.8 million more dollars compared to the consumer and commercial score, respectively.

For a larger version, click on the image.

For a larger version, click on the image.

The bottom line is that using either the owner’s or the business’s credit report alone will give you only about 84% accuracy in managing your commercial credit risk. The use of combined scores offers the opportunity to increase that accuracy. For many lenders, getting increased accuracy for that remaining 16% can be critical.

Credit grantors relying only on consumer credit principles to evaluate the owner of a small business are leaving their portfolios open to unnecessary risk. Commercial credit risk management is enhanced when the use of business-owner credit data is recognized as an industry best practice. The more lenders that actively report and access this information, the more accurate it becomes.

Just as Atlanta would have clearly benefitted from a more detailed prediction of the pending snowstorm, lenders will be able to uncover new opportunities and minimize risk by using a business-owner’s consumer credit report and a business’s credit report to get a more complete and accurate view of a small-business customer’s looming storm cloud.

Tagged under Risk Management, HowTo, Credit Risk, Feature,