Brand, branches, and bodies

Hard look at numbers belies some assumptions—and stresses where improvement is needed

- |

- Written by Mike Moebs

- |

- Comments: DISQUS_COMMENTS

Mike Moebs, "The Prairie Economist," takes a look at three historically critical components of banking. How are the relationships among them, and of each in relation to industry productivity, really changing?

Mike Moebs, "The Prairie Economist," takes a look at three historically critical components of banking. How are the relationships among them, and of each in relation to industry productivity, really changing?

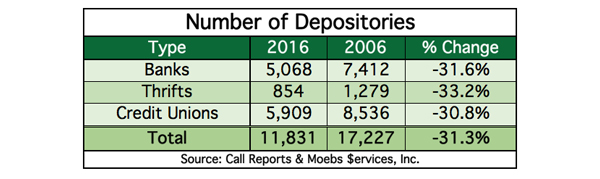

In the past decade, nearly 5,400 financial institutions have closed shop—an overall reduction of 31.3% from 2006. The average annual loss is about 540 financial institutions per year, or three every two days for ten years. Interestingly, each type of depository—bank, thrift, credit union—has lost about the same percentage of institutions.

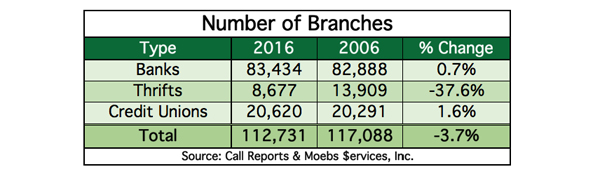

Many depositories show reductions in both their branches and their employees. Branches have been minimized by 3.7% or 4,357 locations. Simultaneously, the number of employees have also fallen by 4.1% or 98,325 employees.

That’s the equivalent of a couple of small cities, if you put them all together.

Similar trends, but differing responses

Currently there are 11,831 financial institutions of all three types with 112,731 branches and 2,319,983 employees. However, the summary numbers don’t tell the whole story.

When taking a look at types of depositories, thrifts stand out. Although the number of thrifts is falling each year, thrifts are becoming more efficient. They are doing so by greatly reducing both branches and employees. This is not the case for banks and credit unions.

Will the ups and downs of charters, branches, and employees hurt depository brands? Which strategy works best?

Why the decline in institutions?

The decline of financial institutions comes from several factors.

One component speeding up this decline is familiar: technology.

The internet and phone apps have enabled remote access to accounts, making it easier for the small-town American to have access to large Wall Street banks. In years past, for most practical purposes, these institutions were not available in their locations. As a result, the smaller depositories lose customers and are being forced to sell or merge.

A second component of the decline in depositories are the complexities of regulations, specifically the passage of the Dodd-Frank Act in 2010 where community banks, thrifts, or credit unions are required to employ four people for compliance where prior to 2010 they had half a person.

Branch change may not result from what you think

In 1997 Bill Gates said, “Banking is necessary, banks are not.” Change is coming fast to banks, thrifts, and credit unions due to fintech companies and other technically savvy players. Traditional institutions are competing with such players as Wal-Mart, Apple, Starbucks, and Amazon.

Due to the increase in outside competition and digital services, depositories are finding the need to reduce branches, and consequently employees, to become more digitally savvy and competitive.

As shown in the table, “Number of Branches,” both banks and credit unions have increased the number of branches over the past ten years. However, as noted, thrifts have shown a decrease.

With the onslaught of technology driven marketing and service, thrifts are making the correct move while banks and credit unions are not.

From 2006 through 2012 banks added 6,144 branches. Since 2012 banks have lost 5,598 branches. So, in the past ten years banks have netted an increase of 546 branches. Banks have been very sticky to reduce the number of branches.

Credit unions are similar to banks. Since 2006 through 2010 credit unions added 1,140 branches. Then in 2011 and 2012 they lost 926 branches. Since 2012 credit unions have added 115 more branches. The net addition over 10 years: 329 credit union branches.

Thrifts have lost a net 5,232 branches since 2006. Yet, since 2013 thrifts have added 719.

Let’s put this in some relative perspective. Overall thrifts have reduced branches 37.6% since 2006, while banks have increased 0.7% and credit unions increased 1.6%.

The bottom line is, with the exception of thrifts, depositories have been very slow in reducing branches. Branch reduction means more resources are available to allocate to IT and digital marketing.

But employee count has fallen, hasn’t it?

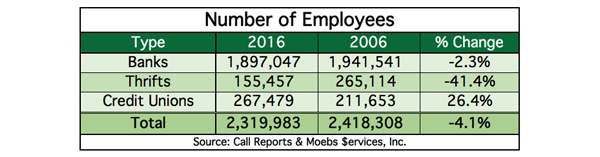

Again, the aggregate numbers don’t tell the story. Look at the chart, "Number of Employees."

Since 2006, banks have reduced bodies by 2.3%. Yet, employee count has been up and down three times for banks over the past 10 years. Overall banks have shed 44,494 employees since 2006.

Thrifts have significantly reduced worker count by 109,657 employees. While thrifts have been adding workers in the past two years, the net for 10 years is a decline of 41.4% in workforce.

Credit unions, with the exception of 2009, have added 55,826 employees since 2006, or a net increase of 26.4%.

To put this in perspective, about half of the resources of financial institutions are employee costs.

While many other sectors of the U.S. economy such as manufacturing and farming have become more efficient with less workers, this has not been the case for many financial institutions. Regarding bodies:

• Thrifts are headed in the right direction.

• Banks have the right direction, but not enough steam to make the business model very efficient—yet.

• Credit unions are definitely headed the wrong way, which is also reflected in their higher operating expenses.

What is the ultimate outcome?

The best definition of generic banking is: “Banking is information in motion” (John Naisbitt, Megatrends, 1982).

Technology is advancing financial information, while regulation is acting as a rising barrier to continuation of banking as we know it (soon “knew it”).

This is the counter to Bill Gates’ comment that banking is not necessary.

There is a massive transformation going on with depositories.

How far the fall? I say it will bottom out with about 4,000 banks, 4,000 credit union, thrifts being incorporated into banks and/or credit unions, and fintech firms being regulated both in consumer compliance and capital.

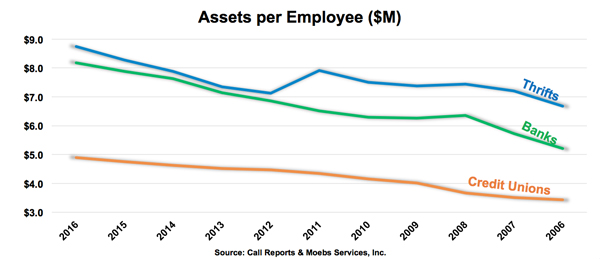

There is one measure which will dictate the results: Assets Per Employee. This measure incorporates: type of institution, size, capital, regulation, branches, and number of employees. This productivity measure, is shown as a graph, below.

In the past ten years, banks and thrifts have increased their productivity. For banks, this measure went from $5.2 million of assets per employee for banks to $8.2 million today. For thrifts, this rose from $6.7 million to $8.7 million for the same ten-year period from 2006 to 2016.

Credit unions are operating at 40% to 60% of what banks and thrifts achieve, and overall, need to become much more efficient if they hope to continue to compete.

But all three financial institutions need to be advancing and increasing productivity to match the fintechs.

The alternative is to be left behind for the archaeologists to examine.

Semper,

Mike Moebs

(Mike will respond to questions at [email protected])

Danielle Martorano, Victoria Mier, and J.V. Proesel all contributed to this article.

Tagged under Bank Performance, Management, Lines of Business, Blogs, Community Banking, The Prairie Economist, Feature, Feature3,