SNL Report: Banks push for yield to combat margin pressure

SNL Report: Squeezing what more they can find

- |

- Written by SNL Financial

By Harish Mali & Nathan Stovall, SNL Financial staff writers

Margin pressure is unlikely to abate for banks as loan growth remains relatively weak, interest rates continue to be low, and banks still hold sizable amounts of lower-yielding securities on their balance sheets.

Banks have relied on their securities portfolios for earnings in recent years and increasingly have sought out higher-yielding credit products and, in particular, municipal bonds to bolster earnings as interest rates remain low. The low-rate environment has caused banks to purchase new securities at lower yields. This, combined with lackluster loan growth and high levels of cash balances, has led to margin pressure.

Banks with more than $1 billion in assets saw their margins decline to 3.28% in the fourth quarter from 3.39% in the linked quarter and 3.54% a year earlier, according to FDIC's latest Quarterly Banking Profile. Banks with less than $1 billion in assets also experienced continued margin compression in the fourth quarter, as their margins fell to 3.70% in the period from 3.77% in the third quarter and 3.83% a year earlier.

Margin pressure has become more pronounced as securities and cash have steadily become larger portions of bank balance sheets. Securities portfolios and loan balances overall in terms of their relative size on bank balance sheets both showed signs of stabilizing in the second half of 2012. But cash and cash equivalents continued to grow, leaving institutions with large blocks of excess liquidity that is also weighing on net interest margins.

A less-profitable balance point

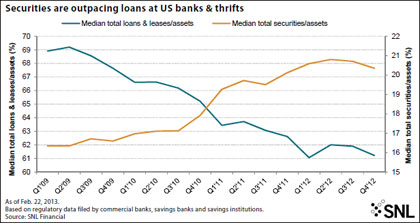

Securities portfolios remained sizable portions of bank balance sheets at the end of 2012. Securities totaled 20.35% of assets at the end of the fourth quarter while loans totaled just 61.22% of assets, compared to 20.71% and 61.91%, respectively, in the third quarter. Three years ago, loans comprised 67.65% of assets and securities totaled just 16.60%, according to SNL data.

Loans have comprised smaller portions of bank balance sheets as underwriting standards have tightened and the slow economic recovery has generated few credits that meet banks' new standards. Most bankers have said that loan growth has come from market share gains rather than underlying economic growth, and that does not seem to have changed much. Banks grew loans by 2.96% from year-ago levels in the fourth quarter, while banks with less than $10 billion in assets grew loans by just 0.60% from a year earlier, according to SNL data.

Institutions have accordingly maintained large balances of securities to bolster their income. Banks with high balances of securities face the possibility holding interest rate risk in their investment portfolios and seeing their positions threatened when rates eventually rise. Rates increased modestly during the fourth quarter, with the yield on the 10-year Treasury rising to 1.78% from 1.65% at the end of the third quarter and the yield on the five-year Treasury climbing to 72 basis points from 62 basis points at the end of the third quarter.

For a larger version of this chart, click on the image or click here.

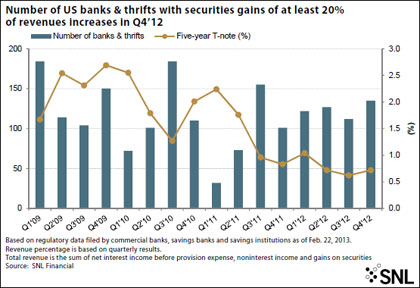

For a larger version of this chart, click on the image or click here.

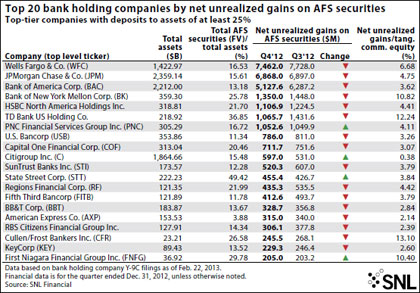

The upward movement in rates might have caused some banks to take advantage of what gains they had in their portfolios before a shift in rates turned them away. In fact, the number of banks reporting securities gains accounting for at least 20% of their revenue rose to the highest level in five quarters, increasing to 135 from 112 in the third quarter and 101 a year earlier.

Institutions that harvested gains might be pleased having witnessed rates increase somewhat in first two months of the first quarter. The yield on the 10-year Treasury rose to 2.05% by mid-February from 1.78% at the end of 2012 but renewed concern over the debt crisis in Europe, and in particular Italy, caused investors to seek safety in Treasuries more recently, pushing the yield back down to 1.88%.

The yields are still historically low. Any banks cashing in on gains would face the difficulty of finding a place to deploy excess liquidity while generating an attractive yield. In recent quarters, more and more banks have turned away from more vanilla securities like Treasuries and agencies and opted to purchase credit products such as CMBS, CMOs and in particular municipal bonds as they search for yield.

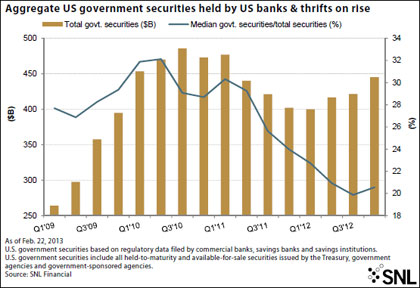

For a larger version of this chart, click on the image or click here.

Ongoing challenge for bankers

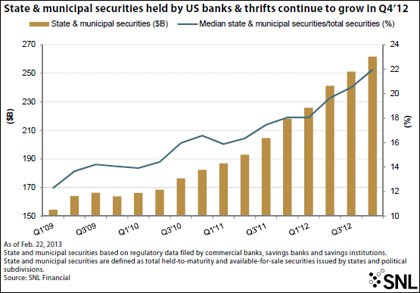

The trend continued in the fourth quarter, though the amount of Treasuries and agencies in bank investment portfolios might have stabilized. Treasuries and agencies totaled 20.56% of banks' securities at the end of the fourth quarter, compared to 19.87% in the third quarter and 28.69% two years ago. Meanwhile, state and municipal securities rose to 21.96% of banks' securities in the fourth quarter from 20.51% in the third quarter and 16.57% two years ago, according to SNL data.

Banks could be taking on credit risk when expanding their holdings of municipal securities, but Janney Montgomery analysts said in a recent report that the greatest near-term risk facing munis actually stems from macro issues such as expected cutbacks from federal spending.

The Janney analysts said in a late January report providing their 2013 outlook for municipal credit that macro factors such as headline risk from the debt ceiling debate and the threat of sequestration, slower economic growth, and continued fallout from the European debt crisis will drive credit and market dynamics in 2013.

Favored status for muni securities

However, they do not expect a sectorwide downward shift of municipal credit conditions and believe extremely distressed municipals will remain "outliers." They accordingly suggested that buyers of munis consider overall credit quality when selecting bonds for their portfolios.

PIMCO's Bill Gross took a similar position in his December investment outlook and listed high-quality municipal bonds among his investment picks given the structural changes he sees in the economy.

Many investors have increased their exposure to munis in search of yield. Investors could also find yield in many nonagency U.S. RMBS, which offer yields similar to high-yield bonds, PIMCO noted in a January strategy spotlight. Those bonds may offer opportunities for greater returns as the housing market continues to show "nascent" signs of recovery, the company said.

For a larger version of this chart, click on the image or click here.

"In fact, even when assuming house price appreciation of close to zero over the next few years, PIMCO still finds that in many cases the risk-return trade-off for nonagency mortgages is more attractive than that for comparable high yield corporate bonds," the company wrote.

Banks could look to those securities to bolster yields and potentially stave further margin pressure. But, that pressure seems unlikely to completely dissipate as loan growth remains challenged, the competition for quality credits like certain commercial loans remains fierce, and interest rates remain low despite modest increases.

For a larger version of this chart, click on the image or click here.

Tagged under Financial Trends,