After Sandy: Helping customers with insurance, post-disaster

Tips for when confused victims seek trusted advisors' input

- |

- Written by Scott Simmonds

Hurricanes, floods, tornadoes, grass fires, and hail storms affect whole communities. Your bank customers may come to you for advice. Here are some points that may help with those conversations, whether your people have been hit by Sandy or will be by the next disaster.

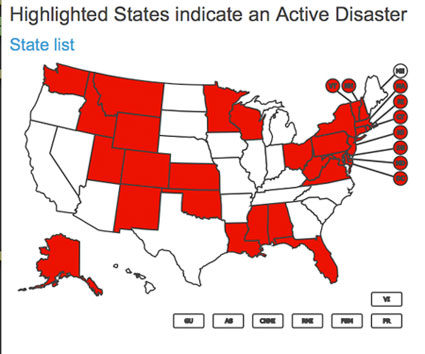

As bad as Hurricane Sandy was, many areas around the country are coping with disasters and their aftermath. This map, taken from FEMA's homepage, shows active disasters as of Nov. 29. Click here or on the image to go to the live map.

Quick hits about hurricanes and property insurance coverage

A critical point is for the banker and the insured to understand clearly what the coverage actually covers.

Flood is not covered by standard homeowners insurance nor by standard commercial property insurance. For most of us, the only place to buy flood insurance is through the National Flood Insurance Program, offered by the Federal Emergency Management Agency. If your customer has only one insurance policy covering their home they probably don't have flood insurance.

Insurers consider the storm-surge caused by wind driving water inland to be flood and not covered by standard property insurance.

In some parts of the country it is common for standard property insurance policies to also exclude wind damage. Your customer will then need to buy three insurance policies: homeowner's insurance, wind insurance, and flood insurance.

Many policies have separate wind deductibles, often described as a percentage of the amount of coverage. A 3% wind deductible on a $300,000 home is a $9,000 deductible.

In Florida, wind deductibles are expressed as an annual dollar amount. Everyplace else, the deductibles are per-storm.

Some homeowner policies include coverage for backup of sewers and drains. That means your residential customers might have coverage for water that comes up through their basement floor drains.

Under standard property insurance, if wind destroys the home and then a flood picks up the debris, the wind damage is covered. If both wind and flood damage a building, the wind damage is covered, the flood damage is not.

Businesses have the additional exposure of the loss of business profits and the expenses that might continue after a building is destroyed. There might be flood insurance to pay for the damage but probably no coverage on the loss of income caused by flood.

There are secondary causes. Suppose that a flood causes a gas leak and that the leak then causes a fire. The resulting fire is covered by standard property insurance.

Trees that fall in the yard in a storm are not covered (the insurer won't pay for the value of the tree nor the cost to remove it). If a tree lands on the house causing damage the repair to the building is covered, including the cost to remove the tree.

Most property insurance policies will respond to rain damage if the building is first damaged first by wind, allowing the rain to enter the structure.

Rain that infiltrates the home without damage to the home is not covered, such as if wind lifts the shingles, but does not damage them. Damage from rain that leaks into a home from improperly sealed (or open) windows is not covered.

Car insurance includes flood coverage if your customers buy comprehensive coverage, that is, other than collision coverage, on their auto policies.

Q&A about property claims

Here are some issues about property insurance claims in general:

Q. When should you report a claim?

A. I suggest that most homeowners and small business owners not report a loss until there is more than $2,500 of damage. Small claims could hurt an insured's ability to buy insurance in the future. However, you'll find that some customers may have no choice but to turn in claims smaller than $2,500.

Customers must be advised to use their own judgment based on their own financial situation. In many cases it's better to just repair the damage. I, myself, wouldn't turn in a claim under $5,000. I have high deductibles on my policies too.

But there is a downside to not reporting claims. If two months after repairs are made the insured finds that there is more damage, the insurer may be unwilling to step forward. The company may give the policy holder a hard time because the insured delayed reporting. Your insurer may have reason to deny the claim.

Q. When you do decide to report a claim, who should you call?

A. The insured should call the insurance company directly. Most insurance companies have a 24-hour claim hotline--use it. Working directly with the insurance company may speed things up. Centralized claim call centers are equipped to handle many calls at once.

A local agent may be swamped with calls in a community-wide event. In most cases large claims will be handled by the insurer anyway. Policy holders should record the name of the person spoken with and any information or instructions given.

The call center is step one. In most cases, an adjuster will be assigned to the case.

But do contact the insurance agent too. The insured should tell the agent that the claim has been reported to the insurer, and that the agent is expected to be the policy holder's advocate in the process.

Here's my advice to owners in this context: "Talk with your adjuster about your policy and the peril that caused your damage. If you don't like what you hear, talk with your agent."

Q. What is a public adjuster, and is it advisable to use one?

A. In most parts of the country there are insurance adjusters who work for insurance policyholders. Called public adjusters, these insurance specialists can help the insured through the claim process. It's likely in the wake of the disaster that the policy holder will hear from public adjusters. Most will charge a fee of approximately 10% of the loss. Hiring a public adjuster has disadvantages besides the cost--many insurance company adjusters and insurance agents are antagonistic to public adjusters. However, many claimants have great experience with hiring their own adjuster.

Q. What should the policy holder do in the wake of the damage?

A. A critical step is to document the damage and everything done on the property. For example, the owners should take pictures of the damage before starting the cleanup. Nothing should be thrown away before the adjuster okays that. Video is preferred.

In addition, the owner should take steps to protect the property from further loss. Policies require that insureds protect their property from further damage or theft. This includes these steps:

- • Patch roofs temporarily.

- • Cover broken windows or holes in walls with plywood, canvas, or plastic.

- • If household furnishings are exposed to weather, move them to a safe location for storage.

The owners should retain receipts for what monies spent and submit them to the insurance company for reimbursement.

Q. How can the insured party maximize their recovery?

A. A key step is to stay on the case: The insured should follow up with the insurance company and be persistent. The company's adjuster should call the insured within 12 hours a receiving report of a claim. If no call is made, the owner should call the insurance company again. Get your agent involved.

Here is how I would advise a disaster victim:

"You must be an advocate for yourself. You must document everything you do and everything adjusters and your insurance agent tell you. You must follow up persistently. The squeaky wheel gets the grease.

"You must be polite but firm. Always find out what the next step will be. Force the adjuster or agent to commit to when they will do what they promise to do. If they say they will call you back in two hours, you call them when two hours and fifteen minutes has gone by. If they promise an answer by Friday at 3:00 PM, you call them when they have not called you by 3:15 PM.

"Document and confirm everything. Realize that even in the best of circumstances this is going to be frustrating. Even if you get the best insurance agent and the best adjuster working for you, this process is going to be a hassle and cost you plenty of time. The worse the damage, the more hassle.

"Accept that your life is going to be interrupted and deal with it. Anticipate problems and failures in the system. Be ready to stand up for yourself."

Q. Where does the burden of proof lie, when an insured files a claim?

A. It's the insured's responsibility to prove what property they have lost. Lists of property, photographs, and receipts will all help in the process. Listing property is a long and laborious process. It is also emotional.

Items of unusual value may require receipts or appraisals.

Q. What issues come up when the values of insured items come under review?

A. Understanding valuation can be critical. How does the policy value the covered property? There is a big difference between coverage for the replacement cost of an object and its depreciated value (called actual cash value). And the same policy can be a mix and match. For example, some policies cover the building for replacement cost but use depreciated value for personal property such as furniture, electronics, and clothing.

Q. What about all the out-of-pocket ancillary costs that come in the aftermath of a disaster?

A. It's important that policyholders press to be paid for their additional costs.

Most homeowner policies cover temporary living expenses after a storm or other major damage. This may include the cost of a hotel or rental of an apartment. In most cases, insurance will pay for the increased cost of living made necessary because of the destruction to the home. Commercial property insurance should include extra expense coverage and loss of income protection to pay the loss of profits and the increased cost of getting back into business. Victims should discuss this with adjusters and agents.

Q. Who orchestrates the repairs?

A. Finding a contractor to repair the damage is the insured's responsibility. The adjuster may make recommendations or advise.

The insured must obtain written estimates from contractors before the work starts. Adjusters will want to be a part of the negotiation process.

Bankers should caution customers to be wary of contractors who show up right after a storm or fire. More than a few homeowners have been taken advantage of by the unscrupulous.

Local, well-known contractors are probably the best bet unless the property is in a disaster zone. Reputations matter. Past experience matters. References should be obtained and checked out. Check and double check references. A mistake in hiring will doom the entire project.

Q. Assuming all that you've advised is done, is that it?

A. No, and my advice to owners is to be in no hurry to settle the claim.

There's a natural inclination to want to settle with the insurer quickly. "Fight the urge!" I advise.

As repairs are made the owner or the contractors may find additional damage. The contractor may discover that the original repair plan isn't appropriate. The cost of materials may suddenly increase dramatically. A cautious, businesslike approach is almost always a winning strategy.

Stay focused and businesslike

A large loss is an emotional rollercoaster.

Even smaller claims can be trying.

Owners will need to work with adjusters and insurance agents throughout the process.

My advice to victims:

"Losing your temper and blowing up may be what you want to do. It will not help. Your behavior and attitude will dictate the tone of the entire process.

"If you stay calm and focused you are well within your rights to demand that the adjuster do the same. If you have behaved appropriately and the adjuster comes at you with an attitude you have grounds to call him on his lack of professionalism.

"Firmly demand what is due you in this process. Stand up for yourself in a businesslike manner. You will end up way ahead in the end."

About Scott Simmonds

Scott Simmonds is an unbiased insurance consultant with a specialty in bank insurance issues. He can be reached at [email protected]. His website is www.BankInsuranceConsultant.com