What to expect when expecting regulators

Tougher exams can be met with better prep

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Patrick Ward, managing director, Darling Consulting Group

As the fourth quarter looms on the horizon, we have a pretty good sampling of what the examiners are asking (demanding?) of their banks during exams in 2014. And if the trends continue, we can expect to see an even greater emphasis on asset liability management in 2015. Regulators are concerned about banks’ potential exposure to rising rates and are focusing their exams on mitigating that exposure as much as possible.

It is not just the exposure they are concerned about, but also the causes and effects of that exposure.

Three areas of particular focus that stand out in talking with hundreds of banks are:

• Interest rate risk sensitivity to rising rates

• Development and support of bank-specific deposit assumptions

• Realization of unrealized losses in the AFS investment portfolio

While the intensity of the exams has continued to rise, there is a silver lining (or two) for those banks that choose to spend the time to prepare.

Sensitivity to rising rates

This can often be a matter of perspective. By perspective, I’m referring to the tools used to measure the sensitivity—net interest income (NII) simulations vs. economic value of equity (EVE).

We have found that the most effective measurement of interest rate risk sensitivity is the utilization of NII simulations, as they factor in variables such as reinvestment of cashflows as well as ramps and non-parallel movements to the yield-curve.

In order for these simulations to be truly effective decision making tools, there are caveats.

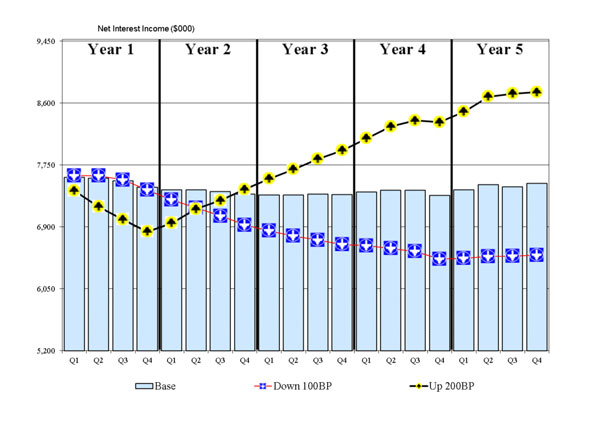

The simulation horizon is important to consider, as those that make decisions based strictly on the near term (i.e. 1-2 years) risk missing the “big picture” of their true interest rate risk profile. There is often a near-term exposure that “self corrects” over time as non-maturity deposit rate increases subside and longer-term assets continue to reprice or be replaced in a higher rate environment.

A longer-term simulation (particularly when viewed graphically by months/quarters versus columnar in total dollars) allows ALCO to gain a better understanding of the degree of exposure, the impact of rate caps or floors as rates rise and how rate risk projections change as compared to the “base” simulation.

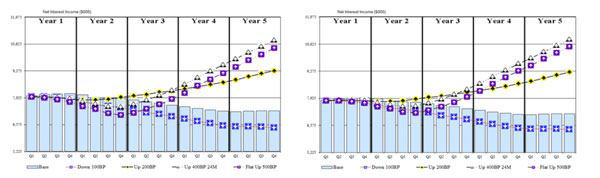

For a larger version, click on the image.

For a larger version, click on the image.

The other benefit of longer-term simulations with a ramping of interest rate movements (versus instantaneous and permanent shocks) is that they provide ALCO the opportunity to identify exposure to a variety of rate scenarios. These include the impact of non-parallel movements (i.e. flattening, twists, etc.), assumption support, and strategy development. This provides significantly more value to the user than limiting analysis to +300/400 basis point shocks.

While the NII simulation provides the most useful information to ALCO from an interest rate risk perspective, regulators also rely on the EVE analysis. However, that tool has significant limitations in its ability to accurately reflect the risk profile of the bank. It is, at its most basic, a theoretical liquidation calculation of the bank and does not account for replacement assumptions in results, a key factor in determining risk exposure.

An EVE analysis may show that there are structural mismatches embedded within the balance sheet, yet it does not provide an indication as to the timing and degree of that exposure, which the NII simulations can do very effectively. Also, the assumptions utilized for non-maturity deposits (NMD) have a significant impact on the results.

Longer life assumptions for the NMD accounts results in higher value than shorter lives. Yet the examiners are concerned about placing too much value on these accounts, thus “masking” the true risk inherent in the balance sheet. Enter deposit studies. . .

Bank-specific deposit assumptions

The regulatory trend toward “bank-specific” deposit assumptions has led many a bank to migrate down the deposit study path, whether that study is prepared internally or by seeking third-party advice.

However, the study findings depend on certain factors—which can vary depending upon who prepared the study—such as:

• The type of historical data (detailed or call report).

• The degree of qualitative analysis incorporated into the study (factoring in of market conditions, bank practices, and customer behavior expectations).

• Terminal life assumptions (providing a “maturity” to a non-maturity account).

Deposit studies are only useful if ALCO understands the methodologies of the study and can explain the results.

And, then, the results are only a starting point.

Deposit studies can provide reliable support for assumptions related to sensitivity betas, average lives, and core balances that can be included in rate-risk and liquidity risk analyses. But in order to truly comprehend the impact these assumptions have on potential rate and liquidity exposure, banks must run alternative simulations or stress-tests to quantify the impact of “being wrong”—these are, after all, assumptions. In addition, the bank must determine which assumptions have the most significant impact on sensitivity.

For most community banks the deposit base is the largest funding source on the balance sheet. The more ALCO understands about the deposit base, the better equipped committee members are to proactively manage customer behaviors and liquidity needs, as well as gain a better understanding of the key drivers of rate sensitivity.

Gone are the days of default or “canned” assumptions. ALCO should take advantage of this opportunity to not only get better assumptions in their risk models but also gain a better understanding of the source of those funds—their customers.

What we have found to be commonplace in the multitude of deposit studies we have performed is that they generally support a longer average life assumption on the NMD base than may have been previously considered. In addition to providing the added “value” to these accounts from an EVE perspective, the greater benefit to banks is that a longer (more stable) funding base may allow more opportunity to support longer assets, which in turn provides much needed income to banks that are seeing margins continue to compress.

As we move closer to the next rate cycle, bankers are cautious about extending assets. The reasons varies. It may be for fear of foregoing “opportunity” when rates rise with shorter assets. Or it may be regulatory pressures about potential exposures to rising rates (NII or EVE).

What a deposit study offers is a way to support the decision to extend assets for additional income opportunities until rates rise. This is to see how the value increase of longer NMDs offsets the “loss in value” in the EVE analysis of longer-term loans and securities. The impact of longer-term securities is also at the top of regulatory exams this year.

Unrealized losses on available for sale

Banks have been in the current rate environment for years. And bankers tend to go in for longer-term securities. As a result, many portfolios currently have unrealized losses in their AFS portfolio, or they will with any appreciable rise in rates.

The potential realization of those unrealized losses is of concern to the regulators when they walk into your bank for your next exam. As a banker who has been struggling to maintain earnings, what are your choices? Sell off those securities and keep the cash short in anticipation for the Fed increasing rates? Get ready to experience even more earnings compression:

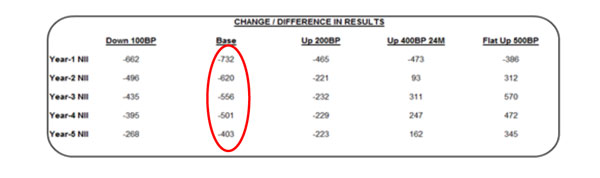

For a larger version, click on the image.

For a larger version, click on the image.

For a larger version, click on the image.

For a larger version, click on the image.

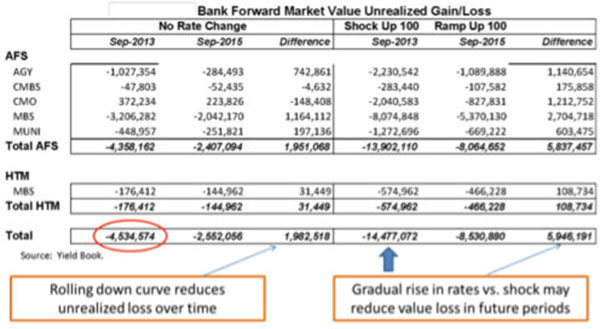

Should you have the funding base to support these assets, it can often make more sense to maintain the status quo, let time “heal all wounds,” and allow for the cashflows to roll down the curve, or allow for the rising interest rates to negate some of the potential loss exposure:

For a larger version, click on the image.

For a larger version, click on the image.

Before being reactive to unrealized losses, ALCO must truly understand the impact actions have on earnings, IRR sensitivity, liquidity, and capital ratios.

The new capital rules for banks that will take effect beginning Jan. 1, 2015, will allow banks an “opt-out” of the unrealized AFS losses running through regulatory capital. It is assumed that the majority of banks will select to opt-out, thus preventing potentially significant swings in regulatory capital ratios due to unrealized losses or gains.

Please note, however, even when you elect to “opt-out” from the regulatory capital ratios, the changes in the value associated with the AFS portfolio will still continue to flow through accumulated other comprehensive income (AOCI) and impact tangible common equity. On the other hand, securities in the held to maturity (HTM) accounts do not flow through AOCI and do not impact tangible common equity.

As a result, many banks are currently in the process of reviewing their allocations within the AFS and HTM accounts and how they relate to the overall level of tangible common equity. Nevertheless, managing potential losses within the investment portfolio remains a fact of life for bankers who must decide the best way to manage regulatory concerns in conjunction with ongoing earnings requirements.

Expect the unexpected

It is a challenge to try to forecast what your next exam will entail. If you plan on being able to address these three aspects of a sound risk management process, you should be in a good position with your examiners. Following these steps, ALCO will be able to best position itself to benefit from the next rate cycle. Committee members will better understand the makeup of the deposit base, how it will behave when rates begin to rise, and what impact that will have on rate risk and liquidity.

And don’t let your investment portfolio dictate how you manage your balance sheet. Be proactive. Understand the impact on earnings, liquidity and capital. Defend your position to your examiners.

The road to effective decision making is a challenging one. But for those who take the time to put a process in place that turns data into information and information into action, you will gain the respect of the regulators and position your bank for success in the years to come.

About the author

Patrick Ward is a Managing Director at Darling Consulting Group. His primary focus is providing balance sheet management to financial institutions. He utilizes his 30 years in banking to provide advice in the areas of pricing, fixed income, asset liability management and capital. Prior to joining DCG, he was a senior vice-president of a large publicly traded regional bank in New York where he developed, executed, and evaluated all of the bank’s ALM strategies and tactics. In addition, he directed the bank’s fixed income portfolio ($1.4 billion) and participated in several M&A due diligence reviews.

Tagged under ALCO, Management, Financial Trends, Risk Management, Rate Risk, Compliance/Regulatory, ALCO Beat, Feature,