Stronger Basel III showing by megas

SNL Report: Most banks see improved capital ratios under “advanced approaches” framework

- |

- Written by SNL Financial

By Salman Aleem Khan, SNL Financial staff writer

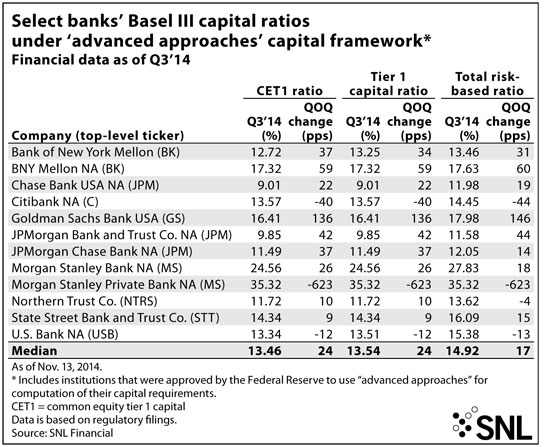

The largest U.S. banks reported higher Basel III capital levels in the third quarter. On a median basis, the 12 banks reporting Basel III capital levels under the advanced approaches framework in 2014 saw improvement in all three capital ratios—CET1 ratio, Tier 1 capital ratio, and total risk-based ratio—as of Sept. 30.

Nine of 12 institutions computing capital ratios under the "advanced approaches" saw an improved CET1 ratio and Tier 1 capital ratio compared to the past quarter, while eight saw an improved total risk-based ratio. The pack of 12 institutions saw a median increase of 24, 24, and 17 basis points in the three capital ratios—CET1 ratio, Tier 1 capital ratio and total risk-based ratio—compared to the previous quarter.

These banks reported capital levels under the "advanced approaches" for only the second time in third-quarter regulatory filings. While most of the banks saw improvements in capital ratios, Citibank NA, Morgan Stanley Private Bank NA, and U.S. Bank NA saw a decline in all three capital ratios. Although Morgan Stanley Private Bank NA's capital ratios were well above the minimum requirements, all three of the institution's capital ratios declined by over 600 basis points in the third quarter, representing the largest decline across the group of 12.

The chart below compares the capital ratios of the 12 Fed-approved "advanced approaches" institutions under the "advanced approaches" guidelines. The "advanced approaches" framework makes adjustments to both the numerator and denominator of the computed capital ratios while the general Basel III guidelines only adjust the numerator of the capital ratios based on Basel III rules.

Details of revised capital reporting

Starting this year, the regulatory capital schedule within call reports was broken out into parts I.A and I.B. Part I.A is reported under general risk-based rules, while the new part, I.B, is filled out using Basel III guidelines by "advanced approaches" institutions and any other institution that elects to use the "advanced approaches" for capital computations.

An entity is defined as an "advanced approaches" institution under federal regulatory capital rules if it has consolidated total assets of $250 billion or more, has on-balance sheet foreign exposure of $10 billion or more, or is a subsidiary of a depository institution that uses or elects to use the "advanced approaches" to calculate total risk-weighted assets.

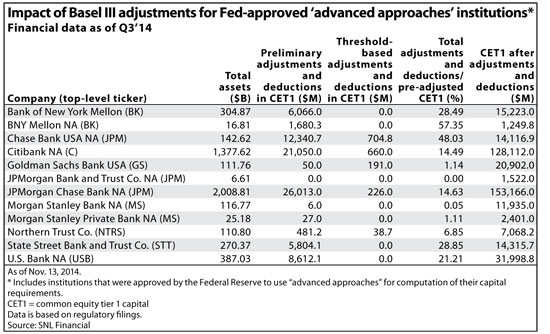

Under the recent changes to the call report's regulatory capital schedule, "advanced approaches" institutions filing the new portion of the schedule are required to compute CET1 capital after making some preliminary and threshold-based adjustments and deductions.

Under the preliminary adjustments and deductions, these banks make amendments to goodwill, intangible assets, significant investments in the capital of unconsolidated financial institutions in the form of common stock and other items.

These institutions are then required to make further adjustments depending on whether the mortgage servicing assets, certain deferred tax assets or significant investments in the capital of unconsolidated financial institutions exceed 10% of the Tier 1 deduction threshold. Those items subject to the 10% threshold also cannot collectively exceed 15% of CET1 capital at the institution, net of the preliminary adjustments and deductions.

Putting the third-quarter results into perspective, these adjustments and deductions had the largest impact on BNY Mellon NA among the Fed-approved "advanced approaches" institutions; the bank's pre-adjusted CET1 capital of $1.68 billion was reduced by 57.35%. However, this percentage has dropped by 1.13% percentage points compared to the first quarter, when the bank reported these figures for the first time under the new reporting requirements. Chase Bank USA NA was next in line, its CET1 capital falling by 48.03% thanks to Basel III adjustments and deductions. The bank also had its CET1 capital reduced by $704.8 million under the threshold-based adjustments and deductions, the largest such hit among the 12 companies.

JPMorgan Chase Bank NA and Citibank NA were the only institutions to have CET1 capital adjusted downwards by over $20 billion in total preliminary and threshold-based adjustments and deductions. The two institutions had $26.24 billion and $21.71 billion in total adjustments and deductions, which amounted to 14.63% and 14.49% of the companies' pre-adjusted CET1 capital, respectively.

How “general” Basel III crowd is doing

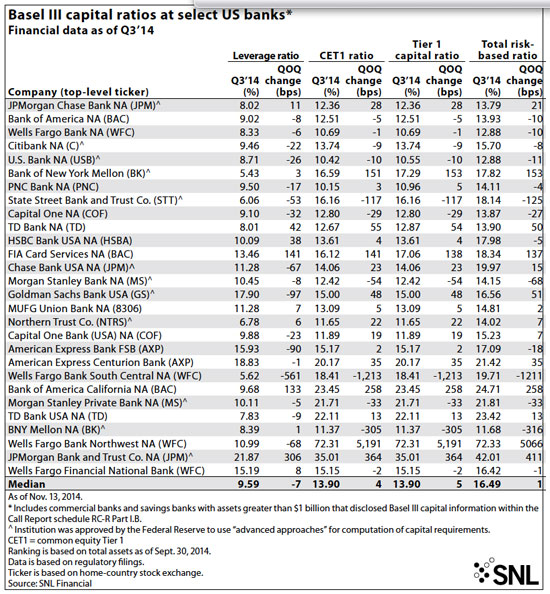

SNL also analyzed institutions with assets greater than $1 billion which started reporting the new regulatory capital schedule under the general Basel III guidelines in 2014. While the "advanced approaches" framework makes adjustments to both the numerator and denominator of the computed capital ratios, the general Basel III guidelines only adjust the numerator of the capital ratios based on Basel III rules.

For the 28 institutions with assets greater than $1 billion, including the 12 Fed-approved institutions, the median improvement in the three capital ratios—CET1, Tier 1 and total risk-based capital—was of 4, 5, and 1 basis point(s). On the flipside, the median leverage ratio for the group of 28 saw a decline of seven basis points under the general Basel III rules. Seventeen institutions saw improvements in their CET1 and Tier 1 capital ratios, while 14 saw an improvement in their total risk-based ratio. Only 11 institutions reported a healthier leverage at the end of the third quarter.

The below chart displays the capital ratios of all banks and thrifts with assets greater than $1 billion, that were either approved by the Fed to report capital ratios under the Basel III rules starting in the first quarter of 2014, or elected to do so. Capital ratios shown are under the general Basel III guidelines and not under the "advanced approaches" framework.

For a larger version, click on the image.

For a larger version, click on the image.