Don’t assume you’ve got ALCO right

It must fit your bank. Now is critical time to truly understand your risks

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Joe Kennerson, managing director, Darling Consulting Group

Last winter’s FDIC’s Supervisory Insights set the tone for interest rate risk analysis and regulatory expectations for the near future. Examiners are concerned with the persistent low rate environment—79 months and counting—and are expecting more analysis and deeper dives in account-level data to ensure a more accurate ALCO process.

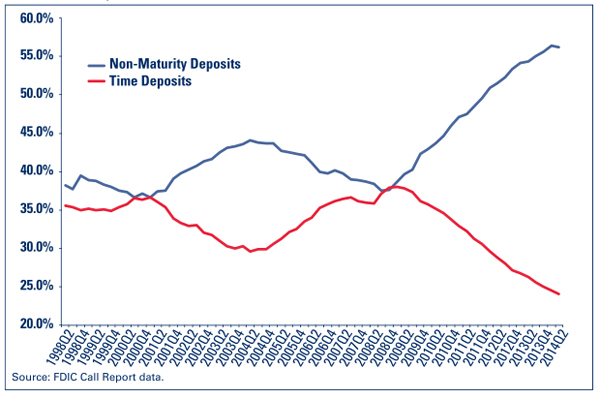

The industry shares the same concerns. The last time the Federal Reserve actually raised rates was over nine years ago. Much has changed since the 2004-2006 rising rate cycle. Banks have experienced a considerable change in deposit mix (see chart below). And many customers have never banked with them through a rising rate environment.

There has never been a more important time in history to truly understand your risk profile given these structural changes and heightened regulatory awareness.

Deposit Composition As A Percentage Of Total Assets For Banks Less Than $10 Billion

As FDIC states in its Insights article, “the use of unsupported or stale assumptions is one of the most common IRR [interest rate risk] issues identified by FDIC examiners.” Falling victim to a stale IRR process can cause headaches during your next exam or even worse—give a false understanding of the bank’s true risk position, which could have a negative impact on future earnings.

Let’s delve deeper.

Assumptions: Think outside the box

Reinvesting all cash flow into like product and utilizing industry standard non-maturity deposit (NMD) sensitivity assumptions is no longer sufficient.

For example, let’s say your bank has decided not to hold fixed-rate mortgages in the current rate environment. Does it make sense to reinvest existing mortgage cash flow back into 30-year fixed-rate mortgage loans?

Assumptions need to be bank-specific and reflective of recent activity and future expectations. Incorporate multiple business lines into the assumptions process (e.g. lending, retail, and treasury), and focus on what is material. For most community banks, a few select categories on each side of the balance sheet have the biggest effect on IRR sensitivity.

The most difficult assumption bankers must deal with today is rate betas on non-maturity deposits. It may not seem suitable to base assumptions on rate movements from ten years ago—but it is a starting point. Risk managers must then take a more qualitative stance in determining expected sensitivities when rates rise.

Examiners expect this: “Banks should consider qualitative adjustments to deposit betas to reflect the possibility that surge deposits will be strongly rate-sensitive once interest rates start increasing.” (from FDIC’s Supervisory Insights)

Diving deeper into the data can help with the qualitative analysis and provide some insight into “stickiness” factors. Ask questions such as:

• How many of my non-maturity deposit customers utilize automatic bill pay? How many have multiple relationships with the bank?

• What’s been the average balance trend of my top depositors over the past five years?

• What’s the average age of my top 25 depositors?

A “big data” analytics approach will give you more confidence in your risk analysis, but can also provide strategic direction. By identifying “at risk” deposit segments, retail departments can devise marketing initiatives to generate more business from your existing deposit base.

The next rate cycle is going to be about deposit retention—now is the time to be proactive.

A loan prepayment analysis can be more complicated, particularly with commercial loans. The good news is that there are more recent rate scenarios on which to base an analysis. Think back to late 2011-2012 when long-term rates were at historically low levels. What type of prepayment activity did your various loan portfolios experience? Thereafter, how much did it slow subsequent to the “taper tantrum” of 2013?

Segment term structures and credit levels when analyzing the mortgage portfolio. Most institutions will find that jumbo mortgages prepay at a faster pace than conforming loans. This data can defend portfolio strategies to hold more 30-year mortgages (if they have a shorter life than initially assumed) and can also drive pricing initiatives.

Scenario analysis: Out with old, in with the new

Analyzing the results can be cumbersome given the amount of scenarios required to be run quarterly.

It can be easy to get caught up with running a multitude of IRR scenarios (ramps vs. shocks, static vs. growth, parallel vs. non-parallel yield curve shifts).

Avoid analysis paralysis—focus on the key three or four rate scenarios needed to manage your IRR position.

It’s out with the old and in with the new when it comes to shocks versus ramps. Instantaneous rate shocks are just not plausible given historical rate trends or future rate expectations.

Does it make sense to shock rates up 300 basis points instantaneously when the Fed funds futures rate in December of 2016 is 1.04% (as of 7/14/15)? Focus more on gradual interest rate ramps in your analysis.

And don’t be blindsided: Don’t overlook a falling rate environment. With all the talk in the industry around rising rates, it can be easy to have a one-sided focus in your IRR process. Don’t discount the impact to earnings if the long end of the curve were to fall.

You don’t have to look back very far for a relevant lesson. In the beginning of 2014, when the yield curve was very steep, the industry was focused on rates moving higher, with little concern over falling rates. The ensuing bond market rally flattened the yield curve—that shrank margins.

The downside risks may be too dire to avoid, even if you don’t think it is a probable scenario.

Finally, remember that rates do not move in unison, so incorporate non-parallel yield curve scenarios. Examine the impact to rates if the yield curve were to flatten or steepen and have the flexibility to alter rate scenarios as the rate environment changes.

Avoid future stress by stress testing

Stress testing is a part of everyday life for community banks.

According to FDIC Insights, “Another issue that examiners observe is that some institutions do not attempt to evaluate how the results of their IRR measurements would change in response to a change in assumptions (i.e. sensitivity testing).”

Assumptions are almost always wrong. As discussed above, we must take the assumptions process very seriously to establish what the bank thinks is most accurate for the model.

A prudent risk management process would then run stress tests on the most material assumptions: non-maturity deposit sensitivity, prepayments, and asset pricing.

Historical analysis on actual trends can provide a starting point to run stress tests. For example, if MMDAs moved 50% with 3-month LIBOR in the last rising rate cycle, it may be prudent to increase the beta to 75% in a stress test. Stress testing will help identify which assumptions have the most impact on your sensitivity and on earnings if you are wrong.

Future of IRR

We are at a most crucial point in the time of IRR reporting. Non-maturity deposit balances are very high and model sensitivity depends on bank-defined assumptions. Additionally, examiners are reviewing the assumptions and how they are developed very closely. Failure to take this process seriously can lead to headaches during your next exam, or—even worse—have a negative effect on your future earnings potential.

About the author

Joe Kennerson is a managing director at Darling Consulting Group. He works directly with financial institutions by providing solutions for their asset-liability management process in the areas of interest rate risk, liquidity risk management, ALM modeling, regulatory compliance, and executive-level education. Kennerson has been with DCG since 2005, where he began his career as a financial analyst and worked as product manager for DCG’s contingency liquidity model, Liquidity360°.

Tagged under ALCO, Management, Financial Trends, Risk Management, Rate Risk, ALCO Beat, Feature, Feature3,