Turn Big Data into Smart Data

Analysis can assist in branch management

- |

- Written by W. Michael Scott

The amount of data being created by businesses, individuals and even computers themselves grows at a staggering rate.

According to a survey by Computer Sciences Corporation, by 2020 the global pool of data will be 35 zetabytes (1,000 million gigabytes)--44 times greater than it was in 2009.

The technology industry has invented the term "Big Data" for this collection of data sets that are so large, complex, and/or unwieldy that they become difficult for companies to capture, process, and use in a fruitful manner.

Unstructured data--information that does not have pre-defined properties and relationships and is not already integrated into databases--is the most elusive element of Big Data. Comprising 80%-90% of all data, unstructured data is also growing at the fastest rate.

Due to the tsunami of Big Data--especially unstructured data--the media have written many articles about the implications for businesses that don't get their Big Data under control. Fortunately for banks, unstructured data is also one of the largest pools of information for creating actionable business intelligence and, in many cases, systems are already available that can gather this data, harness it, and turn it into Smart Data with little to no effort. Leveraging this powerful data can result in sizeable efficiency and productivity gains, customer service enhancements, and overall cost reductions for banks and their branches.

Hidden weapon: data you already have

Banks have access to data covering a wide range of account-holder habits, including when they visit the branch, the frequency of their credit card usage, and even specific purchases.

Never before has real-time data had so much potential to be practically used.

On the other hand, many banks are still using legacy systems that are inefficient and limited in their ability to perform modern data harvesting. Also, these older systems are often inflexible regarding user interfaces and do not provide an easy means of creating custom reports and other data-modeling instruments. Compounding the problem, much of the data available to banks resides in different silos, and is difficult to aggregate for analysis on a bank-wide basis.

Some of the most meaningful Big Data that a bank can use is teller transaction data stored by the core processor and HR Department (especially transaction time, transaction type, and associated employee). This information can be extracted and analyzed to prepare teller performance business intelligence "Smart Data" reports.

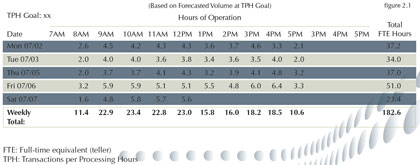

An example of teller performance "smart data": It displays staff needed based on forecasted volume at transaction per hour goal. For a larger view, click on the image or click here.

Another way an institution can leverage Smart Data is through optimally scheduling branch staff to align with account-holder traffic patterns. This systematic staffing approach ensures the FI schedules the precise number of staff for both peak transaction times and idle periods--resulting in better service and a material reduction in labor cost.

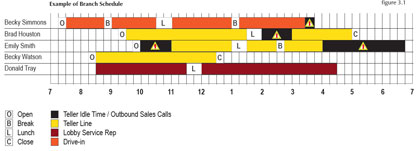

An example of branch scheduling based on account-holder traffic patterns. For a larger view, click on the image or click here.

Boosting lobby performance with Smart Data

The lobby is possibly the most common area of the branch that lacks solid performance information. In many cases, ineffective, manual tracking systems prevent banks from collecting meaningful sales and service information from the platform side of the branch. Even when banks collect lobby data, they may not know how to leverage it as Smart Data.

Implementing a lobby management system, which collects and analyzes account-holder data at sign in and then tracks the customer through wait and assist periods (with all associated details being stored for processing) can create an enormous pool of powerful, actionable information. When properly analyzed by a dedicated business intelligence solution, lobby data can identify service breakdowns, help associates engage in more successful cross-selling, and pinpoint missed opportunities that management can seize in the future by putting new training programs in place.

Using Big Data to improve direct marketing

Another opportunity for banks to make smart use of Big Data is to mine account holder data, such as credit card usage, current service profile, online banking habits and bank website activities, and incorporate it into their marketing messages. In this category, as well, there are technology solutions, including powerful CRM (customer relationship management) products, that facilitate this effort.

For example, banks can segregate the data by product, demographic attributes, or profitability. Once this is done, they will have access to appropriately categorized and segmented, high-level account-holder details they can use to publish targeted marketing communications that will be more relevant to the recipient.

The advent of such technologies as digital printing is making this approach increasingly popular, as it is now affordable to print short runs of postcards, brochures and other print communications, enabling banks to create "target zones" of 50 or fewer customers. All that is needed is the data and a means of making it smart. Thus, instead of promoting consumer loans generically, specific types of loans could be promoted to targeted customers groups.

Data-driven thinking

Big Data in even its most unstructured format has incredible potential to provide powerful insight and actionable analysis. Realistically, however, many banks have yet to invest the proper amount of resources to build a framework that can make the best use of their unstructured data assets. Others are uncertain exactly which resources are most beneficial.

A good place to start: Leveraging the transaction data stored by core processors and HR departments drives substantial benefits across the board--from better service to increased sales and a material reduction in labor cost--and therefore is an excellent candidate as the first Smart Data project.

Tagged under Technology, Core Systems,