SNL Report: Worst reg orders fell in 2012

SNL Report: Severe enforcement actions down to lowest annual total since '08

- |

- Written by SNL Financial

By David Hayes, SNL Financial staff writer

Severe enforcement actions, like bank failures and credit quality, continue to give evidence of an industry on the mend.

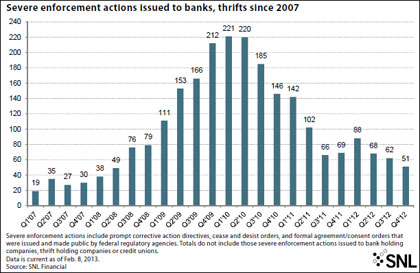

Federal regulators handed out 16 severe enforcement actions in December, bringing 2012 to a close with 269 total severe enforcement actions handed out to banks and thrifts. This was the lowest annual total since 2008's 242 severe actions. The 51 actions handed out in the fourth quarter of 2012 were the lowest amount issued since the second quarter of 2008, when 49 actions were placed.

Severe enforcement actions include prompt corrective action directives, cease and desist orders, and formal agreements/consent orders.

For a larger version of the chart, click on the image or click here.

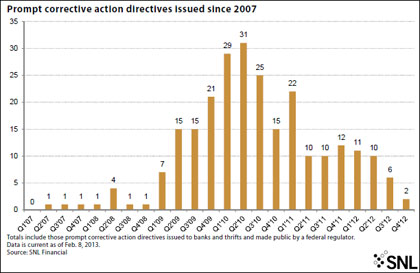

One prompt corrective action directive was handed out in December, the 29th such action issued in 2012. This was also the lowest annual total since 2008, when seven prompt corrective action directives were handed out.

For a larger version of the chart, click on the image or click here.

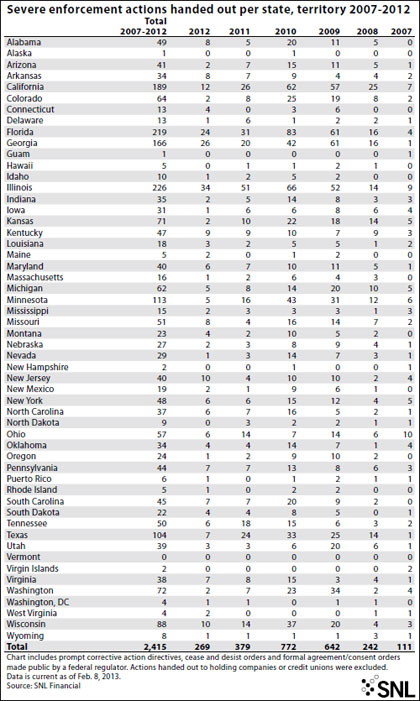

During 2012, 34 severe enforcement actions were handed to banks or thrifts headquartered in Illinois, the most in the nation, followed by Georgia with 26 and Florida with 24. Illinois' 51 actions in 2011 also led the nation that year, followed by Florida with 31 and California with 26.

For a larger version of the table, click on the image or click here.

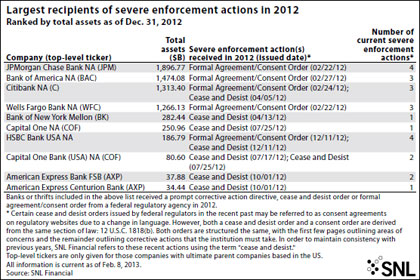

All four U.S. commercial banks with more than $1 trillion in assets, JPMorgan Chase Bank NA, Bank of America NA, Citibank NA and Wells Fargo Bank NA, entered into written agreements with the OCC in February 2012 tied to the companies' handling of foreclosure proceedings. Each of these banks is operating under multiple severe enforcement actions issued after the credit crisis broke. JPMorgan Chase, the U.S.'s largest bank by assets, picked up its fourth active severe enforcement actions after receiving a cease-and-desist order in January of this year tied to the bank's chief investment office and the trading of credit derivatives.

For a larger version of the table, click on the image or click here.

The portion of banks and thrifts under severe enforcement actions has also been declining. As of Feb. 13, 862 banks and thrifts were operating under a severe enforcement action issued after Jan. 1, 2007, equal to about 12.10% of the industry. At the time of SNL's last in-depth analysis of the industry in November 2012, 12.58% of the industry was operating under a severe enforcement action.

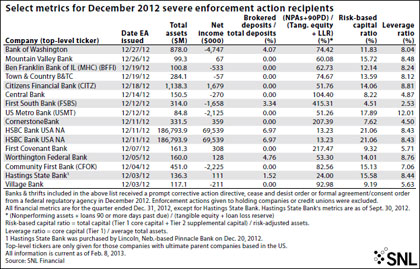

Many of the 16 severe enforcement actions handed out in December contained specific capital guidelines.

Certain cease-and-desist orders issued by federal regulators in the recent past may be referred to as consent agreements on regulatory websites due to a change in language. However, a cease-and-desist order and a consent order are derived from the same section of law: 12 U.S.C. 1818(b). Both orders are structured the same, outlining areas of concerns and the corrective actions the institution must take. To maintain consistency with previous years, SNL Financial refers to these recent actions as cease and desist orders.

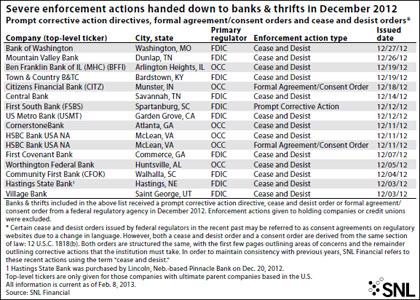

Washington, Mo.-based Bank of Washington received a cease-and-desist order from the FDIC on Dec. 27 requiring the bank to maintain a Tier 1 leverage capital ratio of 8% or more and a total risk-based capital ratio of at least 11% for the life of the order.

For a larger version of the table, click on the image or click here.

For a larger version of the chart, click on the image or click here.

McLean, Va.-based HSBC Bank USA NA received both a cease-and-desist order and entered into a written agreement with the OCC on Dec. 11 tied to findings of serious weaknesses in the bank's enterprise-wide compliance program. The OCC in combination with the U.S. Department of Justice, Board of Governors of the Federal Reserve, Financial Crimes Enforcement Network, Office of Foreign Assets Control, and New York County District Attorney's Office levied a total of $1.92 billion in penalties against HSBC Bank USA NA and its parent, HSBC Holdings Plc.

According to the U.S. Treasury Department's press release, the lapse in HSBC's anti-money laundering systems allowed "hundreds of millions of dollars" from Mexican drug traffickers to flow through U.S. accounts. HSBC's affiliates also processed transactions through U.S. institutions that involved countries or other entities subject to U.S. sanctions.

Commerce, Ga.-based First Covenant Bank received a cease-and-desist order from FDIC on Dec. 7, requiring the bank to maintain Tier 1 capital equal to at least 8.5% of total assets and total risk-based capital equal to 10% or more of total risk-weighted assets within 90 days from the issuance of the order.

Huntsville, Ala.-based Worthington Federal Bank received a cease-and-desist order from the OCC on Dec. 5, requiring the thrift to maintain Tier 1 capital equal to at least 9% of adjusted total assets and a total risk-based capital ratio of at least 13% by March 31.

Walhalla, S.C.-based Community First Bank received a cease-and-desist order from FDIC on Dec. 4, requiring the bank to have Tier 1 capital equal to at least 8% of total assets and total risk-based capital equal to at least 10% of total risk-weighted assets within 120 days from the issuance of the order.

Hastings, Neb.-based Hastings State Bank received a cease-and-desist order from the FDIC on Dec. 3, stating that the bank engaged in "a scheme to mislead regulators and customers regarding the issuer of credit life and disability insurance policies, and by diverting premiums for such policies to a related entity." The bank's merger with a fellow Nebraska-headquartered bank, Pinnacle Bank, was completed Dec. 20.

St. George, Utah-based Village Bank received a cease-and-desist order from FDIC on Dec. 3, requiring the bank to attain and maintain enough Tier 1 capital that the bank's leverage ratio is 9% or more within 120 days from the issuance of the order.

[This article was posted on March 8, 2013, on the website of Banking Exchange, www.bankingexchange.com, and is copyright 2013 by the American Bankers Association.]

Tagged under Management, Financial Trends,

Related items

- How Banks Can Unlock Their Full Potential

- JP Morgan Drops Almost 5% After Disappointing Wall Street

- Banks Compromise NetZero Goals with Livestock Financing

- OakNorth’s Pre-Tax Profits Increase by 23% While Expanding Its Offering to The US

- Unlocking Digital Excellence: Lessons for Banking from eCommerce Titans