New factors in fight for deposits

SNL Report: Prepping ahead of “giant sucking sound” of deposit shift

- |

- Written by SNL Financial

By Kiah Lau Haslett and Zuhaib Gull, SNL Financial staff writers

As the prospect of rising rates looms, banks are increasingly focused on building "sticky" consumer deposits.

In pursuit of sticky funding

Consumer deposits are prized among banks, because most bankers and regulators view them as a reliable funding source that may remain steady even as the eventual turn in the interest rate cycle changes the cost of deposits and possibly leads to deposit outflows. Experts say institutions must prepare to recapture funds that will be redistributed into higher-yielding accounts—which could be a challenge for some and a surprise for others.

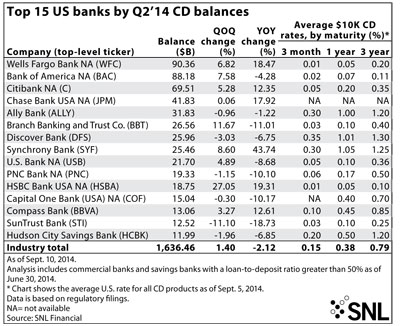

Consumer deposits make up 46.30% of deposits at banks with assets above $1 billion, according to an SNL analysis of regulatory data for the second quarter. The majority of that amount, 61.68%, was held in money market deposit accounts. This is the second quarter that banks have reported consumer deposit figures in regulatory filings, and the figures can differ from GAAP measures.

From a liquidity standpoint, consumer deposits are among the stickiest, most valuable deposits a bank can gather and are the least likely to run off in a crisis, said Sherief Meleis, managing director at bank analytics and advisory firm Novantas Inc. Institutions often grow retail consumers through the modest primary checking account, often called a demand deposit account or noninterest- or interest-checking account.

"All good things flow out of that primary checking," Meleis said. "It gives you the right to cross-sell, so banks are very focused on getting that primary checking account."

When rates rise, funds are liable to leave deposit accounts in search of higher yields; the risk for banks is that they would be transferred outside the institution into money market funds or other investment products. Banks should prepare for deposit runoff and a mix-shift in the distribution of funds, in order to minimize the former and capture and contain the latter. Meleis expressed concern about how banks plan to adjust if rates jump several hundred basis points.

"Banks need to be ready for the ‘giant sucking sound’ that happens when rates start rising and money starts coming out of savings and money market accounts and going to money market mutual funds and CDs," Meleis said. "They need to be ready to capture all of that in a rising rate environment. It's something banks are thinking a lot about—how do we make sure we keep the money that's going to shift out of liquid products into term?"

Impact of rate rise on deposit costs

A Novantas analysis suggests that deposit costs would increase 48 basis points if rates rose 100 basis points, and 96 basis points if rates rose 200 basis points, based on the rising rate environment in 2004. Meleis also noted that rates in the past have climbed quickly, as much as 50 basis points in a quarter.

"There are a lot of people right now in bank pricing who have never been through a rising rate environment and they're going to be learning on the fly," he said, later adding: "It's critical that banks are ready, and because it's been flat for so long, we think many banks are not ready."

Consumer deposits may give an edge to profitability, as many banks have already underwritten assets to be rate-sensitive. Institutions with the stickiest, lowest-cost deposit bases will prove to be the winners from a profitability standpoint, analysts say.

For a larger version, click on the image.

For a larger version, click on the image.

Deposit repricing will be a key factor "in differentiating between the levels of asset-sensitivity within the sector," wrote Keefe Bruyette & Woods analyst Christopher Mutascio in a Sept. 14 report. Institutions that can delay deposit repricing as short-term rates rise may be better positioned to expand their net interest margin.

Mutascio's analysis examined the change in interest-bearing deposit yields from the first quarter of 2004 to the third quarter of 2006, during which time the federal funds rate increased from 1.00% to 5.25%. He then compared the change in yield to that 425-basis-point increase in the fed funds rate, to arrive at a repricing factor. He found that the average cost on interest-bearing deposits increased 226 basis points for large-cap banks in his coverage universe during this time period, which represented 53% of the 425-basis-point increase in the fed funds rate, or an average deposit repricing factor of 53%.

Mutascio's analysis demonstrated that Wells Fargo & Co. had a deposit repricing factor of 60.5%—above the average and at the higher end of a group of 11 large-cap banks. Its cost on interest-bearing deposits in the first quarter of 2004 was 0.88%, the lowest in the group. But it was 3.44% by the end of the third quarter of 2006, only 3 basis points below the average. The increase was above most banks' average during the rising-rate environment.

For a larger version, click on the image.

For a larger version, click on the image.

"[T]he possibility that the flight to quality benefit may completely reverse itself when rates rise as customers will then seek yield over safety/quality/service was somewhat surprising to us," he wrote, later adding that it seems like a "logical explanation" for Wells Fargo's above-average deposit cost increase.

Insights on KeyCorp numbers

In contrast, KeyCorp's deposit repricing factor in Mutascio's analysis was one of the lowest in the group. The bank began the first quarter of 2004 with a 1.67% cost of deposits, 42 basis points higher than the average. Its cost of deposits increased more than 190 basis points by the third quarter of 2006, compared to Wells Fargo's increase of more than 250 basis points.

The narrowing of the spread between the two banks' costs of deposits over time was striking. In the first quarter of 2004, the spread was 79 basis points; by the third quarter of 2006, it was only 17 basis points.

"[I]f history repeats itself, then despite [Wells Fargo's] strong deposit franchise it could actually see its deposit costs rise more than the group average as the flight to quality wanes and customers search for higher yields," Mutascio wrote.

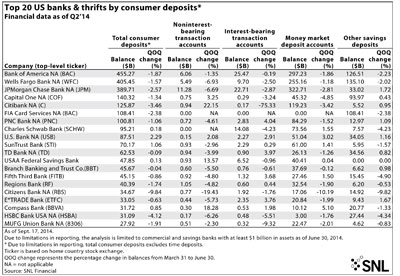

According to SNL's analysis of second-quarter data, consumer deposits at Wells Fargo Bank NA slipped 1.57% quarter over quarter to $405.45 billion. Consumer deposits at KeyBank NA fell 1.70% quarter over quarter to $25.58 billion.

Fresh sources of competition

While Wells, Key, and others could see the cost of their consumer deposits rise when rates increase, most of the competition for consumer deposits now stems from institutions that are less reliant on retail funding, Meleis said.

Commercial deposits are at "an all-time high," and regulators and bankers have expressed concern the money could evaporate as rates rise, he added. There is also competition for consumer deposits from brokers that offer attractive interest rates, low-cost accounts, and ATM reimbursements.

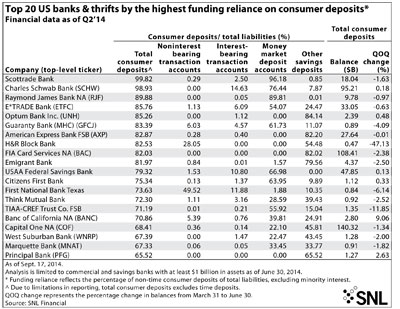

SNL data show that the bank units of several brokers currently hold large consumer deposit balances and in some cases, those deposits make up a large percentage of the bank's total liabilities. According to SNL regulatory data:

• Total consumer deposits at Charles Schwab Corp. unit of Charles Schwab Bank increased 0.18% quarter over quarter to $95.21 billion.

• However, they slipped 0.63% to $33.05 billion at E*TRADE Financial Corp. unit E*TRADE Bank.

• Consumer deposits made up 99.82% of total liabilities at Scottrade Financial Services Inc.'s Scottrade Bank, 98.93% of Charles Schwab Bank's liabilities, and 85.76% at E*Trade Bank.

Just as banks are using deposits as a way to take share of investment, wealth management and retirement accounts, brokers are attempting to capture deposits and interchange income of the clients that already have trading or investment accounts, or establish relationships with new customers, said Ron Shevlin, senior analyst at the Aite Group who specializes in retail banking issues.

Companies like Charles Schwab, E*Trade, and others had historically been challenged by having no physical bank locations, but have leveraged technology as customers become increasingly comfortable conducting financial transactions outside the branch.

"Their business isn't lending so much, so they're not worried about utilizing the deposits," Shevlin said. "They're just looking at it as a way to add additional revenue. In the scheme of things they're not picking up that many consumers out of the mainstream business."

For a larger version, click on the image.

For a larger version, click on the image.

Tagged under ALCO, Management, Financial Trends, Retail Banking,