Banks borrowing to save and grow

SNL Report: Debt force awakens for small banks

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By John Lachica and Nathan Stovall, SNL Financial staff writers

More small banks are opportunistically tapping the debt markets to refinance higher-cost capital and help support growth.

Banks under $1 billion in assets have issued more debt and relied less on common equity when raising capital in 2015, with many institutions taking advantage of the expansion of the small bank holding company policy statement to raise the asset threshold to $1 billion from $500 million.

Institutions falling under the $1 billion asset threshold now are able to hold greater leverage at their holding companies and downstream funds to their bank subsidiaries and effectively lower their cost of capital.

Making up ground after lull

Thomas Killian, principal at Sandler O'Neill & Partners LP, said that if a bank does not expect to grow above the $1 billion asset mark within its planning horizon, it is prudent to consider issuing debt at current rates. While the change in the small bank holding company policy statement occurred in spring of this year, Killian said it probably took a month or two or more for banks to fully get their arms around the issue and speak with their boards. Banks also needed to see that there was investor appetite for their debt, he said.

"As more debt deals have gotten done and the market has absorbed them, there's more positive reinforcement that banks should consider it," Killian said.

Kroll Bond Rating Agency's launch of bank ratings in 2012 helped community banks more readily issue debt, but many of the issuances in recent years have come from banks with assets above $1 billion. The adjustment to the small bank holding company policy statement and the re-emergence of pooled bank credit offerings have allowed a far greater number of banks to issue debt.

Regulators have been clear that banks can harness leverage to finance growth as long as they communicate with their regulators early and often through the process, and offer a clear plan on how they intend to manage their debt service.

That regulatory support helped pooled bank credit offerings surface once again. Recent and ongoing transactions facilitated by the likes of StoneCastle Partners LLC and EJF Capital LLC could help scores of community banks raise three-quarters of a billion dollars in capital. Some of the banks participating in the pooled offerings are as small as $75 million in assets and likely would struggle to issue debt on their own. Single-name debt issuances by small banks have picked up as well.

Ins and outs of community bank debt

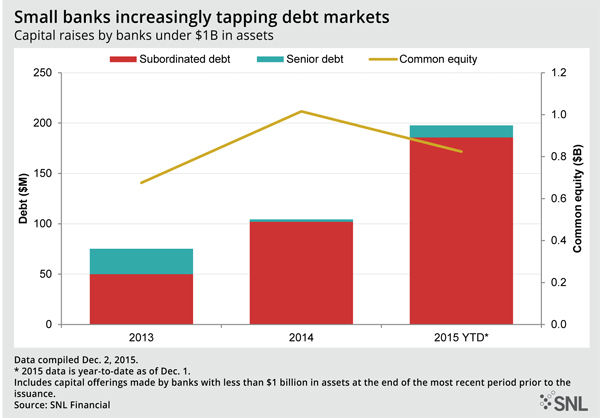

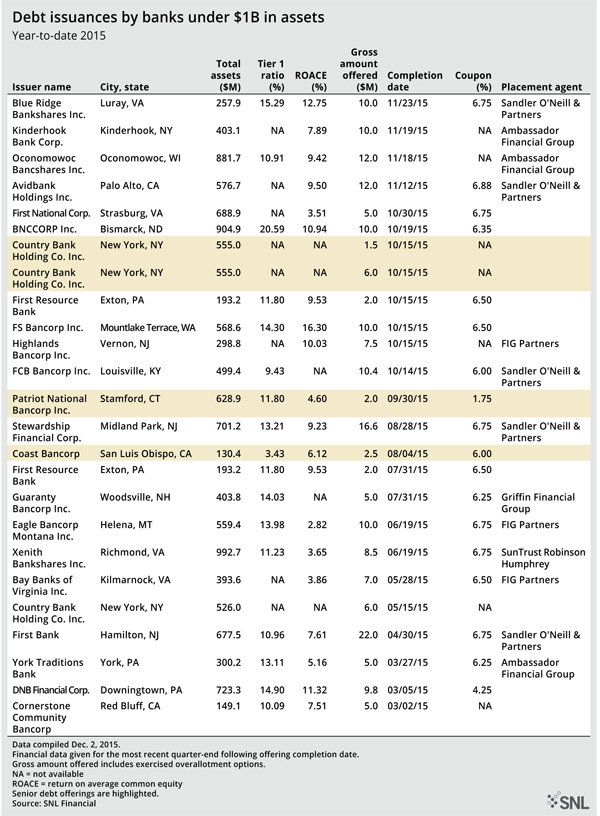

SNL found that at least $197.8 million of debt has been issued by banks with less than $1 billion in assets in 2015 through Dec. 1, compared to $104.4 million in all of 2014 and $75.2 million in 2013. Those institutions are on track to issue less common equity this year, coming to market with $823.9 million in common equity in 2015 year-to-date, compared to $1.02 billion in 2014.

Matthew Resch, co-founder and managing principal at Ambassador Financial Group Inc., said issuing debt represents a far cheaper way for banks to raise capital. For instance, he noted that many small banks are issuing debt around 6.5% to 7%, or at an after-tax cost of 4.3% to 4.6%. That is much less expensive than issuing common equity.

Resch said "the big catalyst" for recent small bank debt issuance has come from a number of institutions looking to refinance outstanding funds raised through the Small Business Lending Fund. The cost of SBLF capital could be as low as 1% for banks that grew their small business portfolios considerably, but the coupon on any outstanding SBLF funds will reset to 9% early in 2016, which equates to roughly 13% on a pretax basis.

Resch said a number of banks are also issuing debt purely to support growth. He said there could be a scenario in which a publicly traded small bank is trading at or even below book value and raising common equity would not be economically feasible. That same institution could potentially raise capital by issuing much more cost-effective debt.

"It's much, much less dilutive than common and lowers their overall weighted-average cost of capital," Resch said.

Banks issuing debt have found an array of willing buyers. Advisers say that buyers of bank debt can vary from local investors and mutual funds to insurance companies and even commercial banks.

Killian said the buyers in each transaction ultimately depend on the size and ratings of the bank issuing debt. He said the buyers can range from high-net-worth and local investors involved in small, unrated transactions to institutional investors and insurance companies buying the paper in publicly registered and rated deals.

Resch said there is now broad interest in the asset class in the investment community. While issuing debt represents a cheap source of capital for banks, the yields on the instruments are relatively attractive in the current low interest rate environment.

"When they compare the ability to invest into a plain vanilla community bank who is a solid performer where they can capture 400, 500 basis points over the 10-year Treasury, it's a tremendously attractive asset class," Resch said.

Resch believes that will hold true as comfort with the asset class grows among banks and the investment community. He expects banks will continue to issue debt; they see the transactions as shareholder-friendly since they lower the cost of capital.

"Barring anything unforeseen, we think the asset class is here to stay and the instrument as a source of capital for the banking sector is here to stay for some time," Resch said.

This article originally appeared on SNL Financial’s website under the title, "The debt force awakens for small banks"

Tagged under Management, Financial Trends, CSuite, Community Banking,