Testing is your essential TRID armor

Catch inevitable mistakes before examiners do

- |

- Written by Lyn Farrell

TRID compliance has high-risk issues that can cost your bank plenty, so testing must be rigorous.

TRID compliance has high-risk issues that can cost your bank plenty, so testing must be rigorous.

The blood, sweat, and tears that went into the initial implementation of TRID last fall will, fortunately, not be needed to implement a TRID compliance testing program. However, establishing such a testing program will not be without headaches and thorny issues to resolve. The sooner a round of testing is complete, the better.

Some regulatory agencies have indicated that they plan to start testing for TRID within the next few months, so it is important that your bank knows where it stands.

Regardless of the time and trouble necessary to set it up, a TRID testing program is an essential element of the required TRID CMS (compliance management system). TRID compliance has too many high-risk issues that can cause real monetary loss to your institution. So it is imperative to have a rigorous testing system in place.

10 testing essentials

There are multiple crucial elements to an effective TRID testing program. The most important factors follow.

1. Make sure the testing samples include all products and channels.

Institutions often have different channels through which TRID-covered loans are made. Often, the channels use different loan origination systems (LOS). Include every channel in the testing sample.

Include every product as well. Different types of products carry some unique disclosure requirements. For example, construction loans are complicated. They require care to ensure that the disclosures are correct. Include these in your samples if your institution makes them.

2. Test for disclosure deadlines.

A key motivation behind TRID rules is providing disclosures to consumers in a timely manner, thus allowing them to shop for loans. (Remember, these rules combine Truth in Lending and Real Estate Settlement Procedures Act provisions—TILA RESPA Integrated Disclosures.)

Therefore, providing loan estimates and closing disclosures within the required deadlines is extremely important. Generally, loan estimates must be provided within three business days of receiving the application (i.e., when the six application elements are received by the bank) and within three business days of a change of circumstances.

Always make sure that your institution has verifiable methods to prove disclosure delivery within the required time period.

• If you use the “mailbox rule,” make sure the mailing date is documented.

• If you rely on alternative methods to confirm receipt, be sure that the bank’s records demonstrate clear confirmation of the receipt. And be sure that the confirmation is applied consistently.

Also, keep in mind this rule (which can be easy to forget): When a loan is rescindable, all parties with the right to rescind must receive their own loan estimate and closing disclosure documents. The institution should be sure to show that all parties were sent their own copies of the required disclosures in this case.

3. Make sure fees on the loan estimate are correct and complete.

Fee disclosures will certainly be the focal point of regulatory exams. First, the fees must be in the proper categories: no-tolerance fees, 10% tolerance fees, and unlimited tolerance fees.

The following are some examples of these fees:

• No-tolerance fee category: Fees must be exactly correct and cannot change later—except in the case of a valid change of circumstances.

Fees charged by the lender, such as points or loan origination charges, are in this category.

• Fee changes in the 10% tolerance bucket are limited to 10% of the total of this category.

The 10% category includes fees for services that the lender requires, but for which the borrower is allowed to shop. If the borrower does not shop for the service, but instead uses the service provider disclosed by the lender, the fees are in the 10% tolerance category.

• The unlimited tolerance category includes fees for services required by the lender for which the borrower can shop for the service provider and for which the borrower did shop for the service provider.

In other words, if the lender allows the borrower to shop for a title company and discloses ABC Title Company on the service provider list, but the borrower shops for and selects XYZ Title Company, then the fee will fall into the unlimited tolerance category.

• Another factor that is important to test is the naming convention for the fees on all loan estimate and closing disclosure documents.

Each of the fee names should clearly and conspicuously describe the charge that is being imposed on the consumer. The fee names also should be consistent from document to document, to avoid confusing the consumer.

4. Test that all subsequent loan estimates were issued for valid changes in circumstances.

Loan estimates can be revised when fees have changed due to valid changes in circumstances. However, if the institution claims that a change in circumstances occurred, the lender must include documentation in the file to support both the change in circumstances as well as when the institution became aware of the information.

To review: There are four main fee-related categories of valid changes of circumstances. Here are some examples:

• Changes involving settlement fees. Example: The property has more buildings on it than originally represented by the consumer, and the appraiser charges are increased as a result.

• Changes involving the borrower’s eligibility for the loan. Example: The consumer overstated income, and when income is verified, the consumer is not eligible for some or all charges that were initially estimated.

• Changes requested by the borrower. Example: The consumer decides to waive escrows, which comes at an additional cost to the consumer.

• Changes related to interest rates. Example: The consumer decides to lock the interest rate after the initial loan estimate is provided, and the discount points associated with that rate are different from what was initially disclosed at application.

• Other changes of circumstances include changes to the estimate of charges when the borrower does not provide an intent to proceed within ten days of receiving the original loan estimate, or if the loan is a construction loan that is not expected to close within 60 days of the date of the original loan estimate.

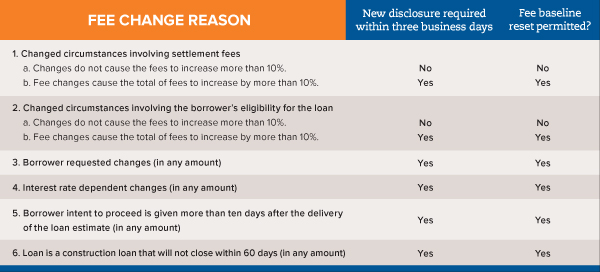

5. Test the fee baseline for the closing disclosure to determine that the tolerances were met.

Even under valid changes of circumstances, a new loan estimate does not have to be provided unless there is a reason to reset the fee baseline. The chart below indicates when a new loan estimate is required and when it is not required because the baseline was not reset. Even if the baseline is not reset, the provision of a new loan estimate is not a violation of the TRID rules.

However, remember that the Consumer Financial Protection Bureau does not encourage providing new loan estimates when not required. The bureau believes that too many loan estimates will confuse the borrower. The correct fee baseline is crucial to determining that the closing disclosure is correct or whether amounts need to be credited or reimbursed to the borrower.

6. For accuracy, recalculate a sample of loan estimate calculations.

Testing the calculations, such as the lender credits, cash to close, and total interest percentage can be challenging tasks unless the inputs for each calculation are apparent in the loan file.

Lenders should document the calculations so that auditors and examiners can easily find their components. In checking these calculations, remember that once lender credits are disclosed, they cannot be reduced without a valid change of circumstances, such as a change in points due to a rate lock.

However, the bureau has stated that a reduction in fee amounts is not a valid reason to reduce a lender credit. The total interest percentage should include prepaid interest, and the in-five-year calculations should include all borrower-paid loan costs and prepaid interest as well as mortgage insurance costs.

Checking the accuracy of the calculations is important because these amounts are crucial to the consumer’s understanding of the loan costs. Their accuracy will help demonstrate to a regulator that the bank is complying with one of the key points of the regulation; that is, allowing the consumer to properly compare loan terms between multiple lenders.

7. Compare the closing disclosure to the last accurate loan estimate.

Loan estimates that are not provided within the three-day deadline will be considered to be null.

So it is critical that the last loan estimate that was timely provided be compared to the closing disclosure to determine if the fees are within the applicable tolerances. The lender credits must match the loan estimate, and the total of payments should include consumer-paid loan costs and prepaid interest.

8. Establish a TRID cure process.

Mistakes will inevitably happen. So the lender should have a robust TRID curative process established to credit borrowers at closing or refund fees within 60 days after closing.

Making sure that there are controls in place to determine the accuracy and completeness of the closing disclosure as well as to refund the correct amounts when necessary are critical to the TRID compliance program.

A tester should select a sample of cured loans and recalculate the amounts to be refunded or credited. A tester must determine if the correct amounts were provided to the consumer within the 60-day time period after the loan closed.

9. Provide proper documentation of your testing efforts.

A TRID testing program is only as robust as the documentation that goes with it. It is critical to provide a regulator or examiner with ample demonstration of your testing program—and its results—in order to support your good-faith efforts at TRID compliance.

In addition, you should make sure you have properly documented the corrective actions taken both in reimbursing individual consumers and to your TRID compliance program to remedy and help prevent these errors from occurring in the future.

Be aware: CFPB has set a precedent of imposing more severe penalties when it discovers an institution did not act in a timely manner upon discovery of errors.

10. Ongoing analysis is not optional.

The final point about all compliance testing programs: They are not static, but fluid, and improve as they mature. An institution should be constantly analyzing the results of its TRID testing, and looking for opportunities to update its processes, procedures, and preventative controls commensurate with the data from the testing.

This article appears in magazine form in the April-May 2016 Banking Exchange.

Tagged under Mortgage Credit, Compliance, Mortgage, Mortgage Compliance, Mortgage/CRE, Residential, Feature, Feature3,