N.J. bank keeps turning out new approaches

Cross River Bank envisions shaking up payments as it did digital lending

- |

- Written by S&P Global Market Intelligence

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

By Zach Fox, S&P Global Market Intelligence staff writer

After enabling a shake-up of the lending landscape, a small bank in New Jersey has set its sights on payments.

Cross River Bank has about $543 million in assets and just one branch, a small storefront in Teaneck, N.J., that shares a retail center with a mom-and-pop clothing store.

But the real action happens four miles away at corporate headquarters in Fort Lee, just across the river from Manhattan.

The space oozes tech startup: Guests sign in on a tablet, every wall doubles as a whiteboard and all the doors are glass, even for the CEO's corner office.

Far beyond the wrapper

Cross River has started to turn heads. In September, it sponsored a policy summit in Washington, D.C., that included a keynote from top banking regulator Thomas Curry. In November, the company secured $28 million in funding from some big Silicon Valley investors, one of whom told The Wall Street Journal that Cross River could be the next Bank of America.

"I don't think the regulators want to hear the fact that we want to be as big as Bank of America," said Chairman, President and CEO Gilles Gade. "I think we want to grow very moderately. Asset growth is not something I want to focus on—transaction growth is."

A B2B compliance provider

Cross River is essentially a business-to-business bank. It handles the messy, boring parts of banking so its fintech partners can improve customer experience with easy-to-use platforms.

Financial regulation is notoriously onerous, and many of the rules apply to nonbanks. The Bank Secrecy Act and anti-money laundering rules, for example, apply to all lending institutions and money transmitters; the examination manual runs 442 pages long.

Digital lenders can avoid burdensome state licensing requirements and achieve regulatory compliance more easily by partnering with a bank such as Cross River.

In the minutes it takes an online borrower to secure financing, Cross River's automated engine ensures compliance in real-time.

"That's our specialty," Gade said. "[We] bring legacy regulatory compliance to the fintech industry."

First, Cross River vets the lender's credit policy, including the algorithm that evaluates creditworthiness, for fair-lending concerns and general compliance.

Cross River's automated engine will then re-underwrite each loan and test it for proper compliance, re-calculating all relevant ratios such as annualized percentage rates as required by the Truth In Lending Act.

Newer Cross River clients, such as Quicken Loans Inc.'s Rocket Loans product, already use this automated engine while others have legacy platforms. All 17 digital lenders partnered with Cross River will be on the automated engine by the 2017 second quarter, Gade said.

Digital lenders might benefit even more from Cross River's preemption from state laws.

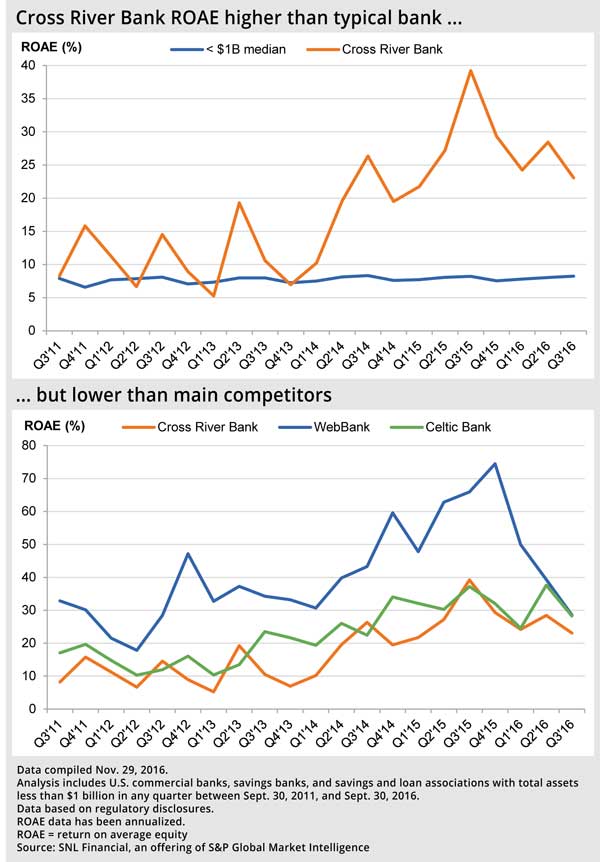

The use of issuing bank partnerships is nearly ubiquitous in digital lending. WebBank is arguably the biggest player by virtue of servicing the largest marketplace lenders: LendingClub Corp., Prosper Marketplace Inc. and Avant. But Cross River is not far behind, acting as the issuing bank for Marlette Funding's Best Egg platform, Upstart and Affirm. The bank also won the right to issue consumer loans for mortgage giants Quicken and loanDepot.com LLC. Utah-based Celtic Bank is big in the small business space as the issuing bank for On Deck Capital Inc., Kabbage, and Square Capital.

So far, issuing bank partnerships have been extremely profitable. Cross River's return on average equity exceeds 20%, less than that of its issuing bank competitors but well above the sub-10% ROAE for banks with less than $1 billion in assets.

"Big nut to crack"

Cross River acts as fintech's gateway to banking, earning fee income for the service as well as booking interest income on the loans it retains.

But the bank gets its own gateway, too, into the fintech business.

It seems Gade wants to be the behind-the-scenes banking provider for anything and everything fintech. Gade said the bank's digital lending partners have "naturally" moved to Cross River's payments system.

"As in the Quicken example, we're getting a shot at the rest of their business, which is the $80 billion of mortgages they originate on a yearly basis and the couple trillion dollars of loans that they service on an annual basis," Gade said. "This is a big nut to crack, but we're part of the conversation."

Gade believes Cross River's payments activity could double next year, and the bank already has relationships with Stripe and Google Wallet to provide access to the Mastercard Send product.

For example, when Google Wallet users send money to each other with a debit card, Google uses Cross River as an "acquiring bank" to access Mastercard's platform. With increasing competition, pricing is tightening, but Gade said there is still plenty of money in the business.

"When you pay $25 to [JPMorgan] Chase for a wire, that wire doesn't cost $1. It doesn't cost 50 cents, it doesn't even cost a quarter. So the margins are huge. We don't need to make a 95% margin on that kind of transaction. If we make a 50% margin, we're happy," Gade said.

Cross River currently handles roughly 2 million transactions per month, and there are "a lot of market shares for the taking," Gade said. He highlighted insurance companies paying out claims, commercial landlords looking to accept payments from tenants and auto companies collecting lease and loan payments as examples.

Gade said the bank has taken advantage of working with money services businesses, which have been shunned by traditional banks as part of fallout from the Justice Department's Operation Choke Point, which investigated financial institutions' relationships with payment processors and payday lenders.

But the bank is still risk-averse. It refuses to deal with cannabis companies due to legal uncertainty. And Cross River does not service payday lenders.

"There are many bad agents that have tarnished the payday lending business and until this is sorted out, I don't want to play cop," Gade said.

Todd Baker, managing principal of Broadmoor Consulting, said Cross River might be uniquely positioned to take advantage of the payments space because many larger banks have conflicts that preclude them from partnering with payment startups. "[Cross River is] willing to take a little bit of money to do it because they're not competing against themselves," Baker said.

Issuing bank partnerships currently account for roughly 40% of the bank's business. Traditional community banking activities, such as commercial real estate and small business lending, account for 40% to 50% of its activity, and the remainder is related to payments. Gade said payments activity could stabilize at roughly 30% of activity, with issuing bank partnerships staying around 40%. The traditional community banking share will shrink but still constitute 20% to 30% of business.

There is speculation that Cross River could be working on something more in the realm of traditional banking, although with a fintech twist.

Cross River has quietly built a brand known as Almond Bank that has attracted significant attention from fintech followers. Ben Weiss, a former "entrepreneur-in-residence" for Two Sigma Ventures, joined Cross River more than a year ago and lists his job on LinkedIn as "building stealth-mode consumer bank."

"I don't see them becoming Bank of America just on the backs of marketplace lenders, so that's where I think Almond Bank comes in," said Peter Renton, co-founder of Lend Academy. Renton does not know what Cross River is building in Almond Bank, but he speculates it will be an online banking platform to gather deposits.

"While it is too early to go into details, Almond is the bank's research-and-development lab," Gade said, unwilling to expand.

Potential hurdles

Silicon Valley wants to disrupt banking, and Cross River is well-positioned to be the bank that makes it happen. But competitors abound, and larger banks have a cost-of-funding advantage. There could also be legal challenges.

Digital lending partnerships have been heavily scrutinized due to recent court rulings that raise questions about the model's legality. The issuing bank typically holds the loan for a few days before selling it to a hedge fund, bank or other investor. Courts have held that preemption from state laws requires that the bank be the "true lender."

Cross River has this problem solved, Gade said, with risk retention: The bank retains 5% to 10% of the loans issued by its partners and holds them for an average of about one year, Gade said. The bank either holds a loan selected at random by a computer or retains a vertical slice of all loans issued.

Another threat to the issuing bank partnership model emerged recently when the Office of the Comptroller of the Currency unveiled a framework for a fintech special purpose charter that would offer preemption without a bank partner.

That eliminates the raison d'être for many of Cross River's lucrative partnerships. Still, analysts and consultants think the special purpose charter's effect on issuing bank partnerships will be marginal.

"Compliance is a big hurdle to innovation in finance," said Jo Ann Barefoot, a former deputy comptroller for the OCC who now heads a consulting firm. "When a bank like Cross River can get some economies of scale and get that automated, it helps these innovators focus on what they do best."

Cross River plans to spend its $28 million in venture capital on improving its compliance engine, other regulatory technology investment and increased retention of loans originated by its digital lending partners. Greater loan retention helps Cross River's fintech partners with a significant challenge: stable funding sources.

"We're looking at the marketplace lending industry very holistically," Gade said. "As an end-to-end solution, from origination to funding and even post-funding with liquidity channels, we want to own that part of the equation."

This article originally appeared on S&P Global Market Intelligence’s website under the title, "Cross River Bank envisions shaking up payments as it did digital lending"

Tagged under Bank Performance, Compliance, Compliance Management, Community Banking, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story