Robust ALM modeling is banker’s compass

Keeping your bank headed in right direction demands a steady guide

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Zach Zoia, senior consultant, Darling Consulting Group

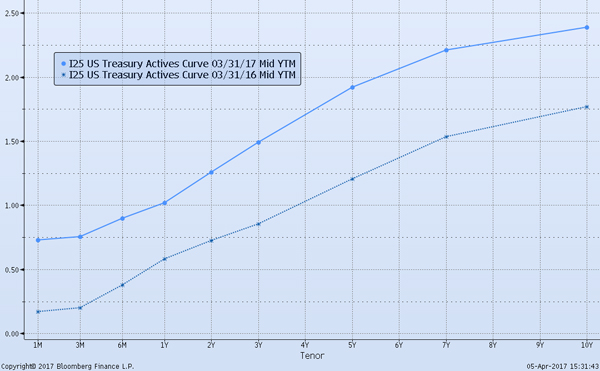

“What is the 10-year Treasury yield today? What about the latest Fed Dot Plot? What can these two data points tell us about the future trajectory of interest rates?”

These questions are constantly being asked at nearly every ALCO meeting. And that’s not surprising. Think back to a year ago, when over $13 trillion of global debt was at negative yields, the 10-year Treasury was trending towards its lowest point, and the Federal Reserve was having trouble getting the markets ready for one additional hike in 2016—let alone four.

It was during this time that discussions were materializing at ALCO meetings about the potential for lower, perhaps even negative, rates in the U.S. They revolved around such issues as:

• What would we do with deposit rates and fees?

• Do we have floors on our loans?

• Can our core systems even handle negative market rates?

Given today’s yield curve, such conversations are a distant memory.

Markets have experienced two rate hikes since then, and the intermediate and longer points of the yield curve sold off considerably during the fall. Now, rising rates have returned to the forefront of almost every discussion, with speculation concerning the pace and magnitude of future rate changes.

However, the more important issue is that every institution needs to have a strong asset-liability management (ALM) process to help navigate the prevailing winds of the markets, no matter which way they are currently blowing.

Rate projections and environments can change rather quickly, as we have seen with the volatility just over the past year, but robust ALM modeling can be the compass to help more clearly direct decisions made at ALCO.

A central component of the ALM modeling process is stress testing.

What is your modeling game plan?

Establishing a set of benchmark scenarios that are performed each quarter is an important aspect of your modeling outputs. This allows your institution to establish a consistent baseline to assess risk. The +/- 200bp ramps over 12 months are fairly common “core” scenarios to utilize.

Furthermore, guidance from the Joint-Agency Advisory on Interest Rate Risk Management in 2010, in conjunction with the subsequent Frequently Asked Questions in 2012, made it clear that more needs to be done.

In fact, the Joint Guidance stated that:

“In many cases, static interest rate shocks consisting of parallel shifts in the yield curve of plus and minus 200 basis points may not be sufficient to adequately assess an institution’s IRR [Interest Rate Risk] exposure. As a result, institutions should regularly assess IRR exposures beyond typical industry conventions, including changes in rates of greater magnitude (e.g., up and down 300 and 400 basis points) across different tenors to reflect changing slopes and twists of the yield curve.”

And we, at DCG, wholeheartedly agree.

Now, this is where “stress-testing” comes into play. Under the umbrella of stress testing are two important categories: scenario analysis and sensitivity analysis.

What is scenario analysis?

Using the aforementioned publications as our guide, scenario analysis should “assess a range of alternative future interest rate scenarios” that “should be sufficiently meaningful to identify basis risk, yield curve risk, and the risks of embedded options.”

While there are countless permutations of interest rate scenarios that could be modeled, a best-practice ALM model typically includes some combination of the following in addition to benchmark scenarios:

• Rate ramps of greater magnitude.

• Rate ramps over a longer period of time.

• Rate shocks.

• Changes in yield curve slope.

• Changes in relationships between key market rates.

Running a portfolio of simulations that include these types of market moves will help provide a clearer picture of your institution’s earnings at risk. However, it is critical that the scenarios modeled are plausible and tailored to the present rate environment.

In other words, running a down 300 basis points simulation, given present day rates, does not fit.

The scenarios should be crafted to add value in helping to triangulate your risk position, and not viewed in the spirit of “more-is-better.” That will just lead to an exercise of “analysis-paralysis.”

Where sensitivity testing comes into play?

Assuming your models are firing on all cylinders given the breadth of scenarios mentioned, it is pivotal to sensitivity test in order to help identify which assumptions have the greatest influence on the modeling results.

But interest rate risk (IRR) models include thousands of assumptions, so where do we begin?

There has been an emphasis on including “institution-specific” assumptions with IRR models for some time now. The 2010 guidance even states, “financial institutions should perform historical and forward-looking analyses to develop supportable assumptions.”

These types of assumptions typically revolve around the following:

• Replacement of cash flow/maturities (rates and products).

• Asset prepayments.

• Non-maturity deposit price sensitivity and decay rates

So it is only practical to make sure your modeling includes sensitivity testing that addresses these key assumptions.

Yet, even if you performed an intense “study” of your prepayments or deposit betas and lives, the past is not always a predictor of the future.

The best way to frame how to conduct and analyze sensitivity tests is to ask the question, “What is the impact if we are wrong about x, y, or z assumption?”

For example:

• What is the impact to our IRR profile if pricing spreads are narrowed within our loan portfolio?

• What if investment and loan prepayments accelerate even more as rates fall—or slow more considerably as rates rise?

• What if we have to pay more on deposits to maintain our current customers?

• What if we do not pay as much as we assumed in the model, but we see deposit migration/disintermediation?

• What if our deposits are not as “core” as we calculated?

These key assumptions center on customer behavior patterns—difficult to predict. Quantitative support is a great starting point, but there are qualitative aspects that need to be considered to formulate and refine model assumptions. Better said, assumption development is as much an art form as a science.

Accordingly, institutions that run these types of sensitivity tests gain more knowledge about the levers that influence the models most. Thus they can better assess the spectrum of potential impact in case these assumptions are proven wrong by actual experience.

Stress testing is an essential part of your ALM modeling.

The goal of IRR modeling should be to produce models that enable members of ALCO to make well-informed decisions regarding balance sheet strategy.

No matter which way the current rate forecast winds are blowing, stress tests that include a combination of scenario and sensitivity analyses can help to triangulate the risks inherent in your balance sheet, and are an integral component of a decision-oriented, robust ALM modeling process.

About the author

Zach Zoia is a Senior Consultant at Darling Consulting Group. He works directly with financial institutions throughout the country and across the ALM spectrum, with focus on interest rate risk modeling, liquidity management, capital planning, strategy development, and regulatory compliance. He also leads new client model implementations and assists with executive education. In addition, he serves as Product Manager of Prepayments360°, DCG’s proprietary loan analytics tool.

Tagged under Management, Financial Trends, Risk Management, Rate Risk, Feature, Feature3,