REG Burden Hits Small Hardest

Study finds economies of scale in compliance, and little match between spending and exam ratings

- |

- Written by Website Staff

How much does your bank spend on regulatory compliance? A recent Fed district bank study found that community bank compliance costs averaged 7.2% of non-interest expense. While significant by itself, that average hides a trend with significant implications—but let’s not get ahead of the story.

When S. 2155, the Economic Growth, Regulatory Relief, and Consumer Protection Act was signed into law, the industry breathed a big sigh of relief. But getting rid of some of the Dodd-Frank Act rules, or easing them, won’t solve the totality of the regulatory burden banks face—not by a long shot. There was plenty to do before Dodd-Frank came about, and most previous relief laws merely nibbled around the edges of compliance duties.

In fact, it has been pointed out by some in the compliance fraternity that, in the wake of S. 2155, banks initially will face additional costs in unwinding systems and procedures built at a significant cost to handle the rules that have been eliminated or amended.

Indeed, in an analysis of S. 2155 on BankingExchange.com by Zach Fox of S&P Global Market Intelligence, the writer states: “For smaller banks, the relief appears more modest. Some of the law’s provisions meant to ease regulatory burden will have little impact for a simple reason: Small banks were already exempt. Provisions, such as qualified mortgage status for loans held in portfolio, higher leverage at bank holding companies, a lengthier exam cycle, and a shorter call report, were already available to banks with less than $1 billion of assets.”

The hopes for further relief through Senate consideration of other financial legislation sent over by the House remain just that—hopes. Political promises from Senate leadership to House Financial Services Commission Chairman Jeb Hensarling have been made in a midterm election year that may exert unusual gravitational pull on legislation.

And that makes the findings of a Federal Reserve Bank of St. Louis study about community banks’ regulatory costs especially interesting. For those who predict that compliance costs will continue to encourage consolidation at the small end of the industry spectrum, the study provides more evidence.

Indeed, the study reports that 85% of bankers in the most-recent sampling in its database indicated that regulatory costs were important in considering acquisition offers.

The project makes it clear that regulatory burden hits smaller community banks harder than larger community banks, and that the impetus to merge for compliance efficiency will not go away, even though the recent regulatory reforms may help some institutions.

Even relief from S. 2155 appears more modest for small banks, which were already exempt from some provisions

Major findings

The Fed study, entitled Compliance Costs, Economies Of Scale, And Compliance Performance, was published in April. The project was based on survey data compiled from among nearly 1,100 community banks by the Conference of State Bank Supervisors in 2015, 2016, and 2017. (All institutions in the sample were under $10 billion in assets.) Interestingly, the researchers also referenced multiple studies of banking compliance costs that have been performed in recent years by agencies, academics, and associations to give a full picture around their own findings and arguments.

The survey looked at regulatory costs in multiple ways and at multiple levels. Among the findings:

• Economies of scale exist in compliance. Many forms of compliance have incremental costs—suspicious activity reporting, mortgage transactions, etc., cost more with increasing volume—but the ongoing fundamental systems costs and the costs of keeping current apply to all institutions.

“Banks with assets of less than $100 million reported compliance costs that averaged almost 10% of non-interest expense,” the study reports, “while the largest banks in the study reported compliance costs that averaged 5%. In other words, the compliance cost burden for the smallest community banks is double that of the largest community banks.” [Emphasis added.] The largest banks referred to were those with between $1 billion and $10 billion in assets.

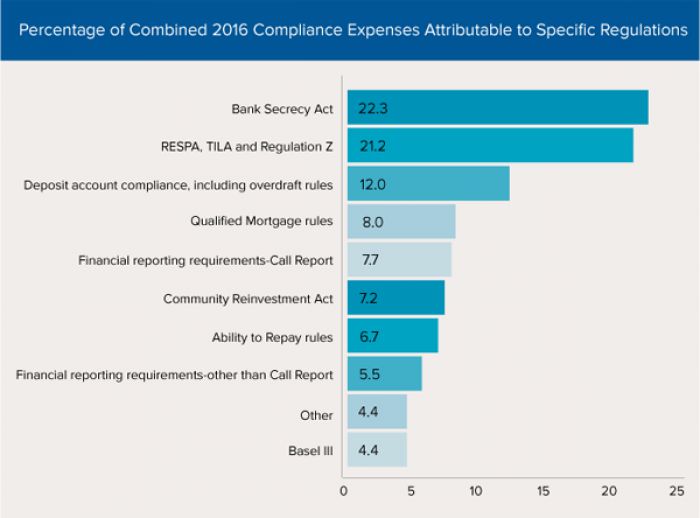

• Bank Secrecy Act compliance costs lead the way among expenses tied to specific regulations. In the 2017 survey results, based on 2016 numbers, BSA expenses dwarfed all other compliance costs, with the exception of those related to RESPA, TILA, and Regulation Z. This is interesting because Comptroller of the Currency Joseph Otting, a former banker, identified BSA costs early on as a priority. While banking agencies can’t directly change the rules, Otting has spearheaded efforts to discuss these issues with the agency that does, the Financial Crimes Enforcement Network, or FinCEN. As Exhibit 1 indicates on the opening page, mortgage-related rules would supplant BSA as the leading categories if the RESPA, TILA, and Regulation Z, Qualified Mortgage, and Ability to Repay rule bar were combined into one, totaling almost 36%.

• Personnel expenses account for the majority of community bank compliance costs. The study found that this was followed, in order, by data processing, accounting, consulting, and legal expenses. The report states that personnel costs—coming to 5.1% of average non-interest expense—represent almost seven times more than the other four categories combined.

“Compliance expenses for personnel appear to be more subjective than expenses in the other categories,” the report says. “For example, it may be difficult to estimate just how much time a loan officer spends filling out compliance forms versus drumming up new business. Respondents may account differently for the time and attention devoted to compliance by chief executive officers or boards of directors.”

• Compliance spending and compliance ratings bear little relationship to each other. For this analysis, the researchers looked at both compliance ratings and the M—for management—component of the CAMELS ratings, which includes consideration of the management and board oversight of the compliance function.

The analysis found that “within a given size category, compliance expenses as percentages of non-interest expense do not appear to vary systematically for banks with different performance ratings. For banks with assets of less than $100 million, for example, relative compliance expenses at the highest-rated banks were lower than for other banks, while for banks with assets between $500 million and $1 billion, relative compliance expenses were higher for the highest-rated banks than for other banks. This suggests that compliance performance is based on factors other than what is spent on it.”

Read the study in its entirety, tinyurl.com/SaintLouisFedBank

Read the S&P Global Market Intelligence post, tinyurl.com/regrelief

Tagged under Compliance, Compliance Management, Feature, Feature3,