Revamped tools could boost commercial business

Effective strategies for using a business process model approach to overcome challenges in corporate lending

- |

- Written by Shobhit Mathur & Amit Mishra

Special to Banking Exchange Tech Topics By Shobhit Mathur, program director, Banking and Financial Services and Amit Mishra, senior consultant, Banking and Financial Services at MindTree Limited.

For the last decade, information technology investments in banks have focused on bringing about automation in the high-volume retail banking portfolio. Corporate banking, specifically lending, has been assumed to be too subjective and relationship-driven to support centralization and automation. Consequently, corporate lending groups in most banks have disparate islands aligned to different customer segments or product lines.

With regulators introducing a slew of legislation like the Durbin Amendment/Reg E that adversely affect margins in retail banking, banks are compelled to look at other lending opportunities with renewed vigor. As the focus shifts back on corporate lending (SMB and large business) it is almost certain that the current way of doing things will not last. Various factors that point to this threat are:

Regulatory pressure. Post financial crisis, there has been added pressure from regulators to capture and refurbish all kinds of data; spanning across proposal evaluations to portfolio of exposures and assets.

Growth implications. Today, banks can still accommodate inefficiencies in corporate banking as the number of deals are fewer. Going forward, with banks ramping up volumes, the key considerations are to control credit quality and operational costs.

Customer expectations. Lending needs of corporate customers are increasingly more sophisticated. Coupled with intense competition among banks for a share of this business and availability of new age technology, customers have started expecting better service standards, that include demand for better rates and transparent and predictable service.

Corporate Lending—The way it works today

There are four key stakeholders in corporate credit processing:

• Sales (Relationship Manager and the admin/assistant staff)

• Product Specialists

• Credit Department

• Credit Operations

Figure 1: Existing Credit Approval Process

The credit approval process revolves around the Credit Proposal/Credit Appraisal Memo created by the relationship manager, which is passed back and forth between these stakeholders. Due to a lack of centralized systems, the sales unit spends a significant amount of time in nonsales activities; i.e. data collation and follow-ups. Some key deficiencies in the existing process are as follows (Note: TAT stands for turn around time):

The credit approval process revolves around the Credit Proposal/Credit Appraisal Memo created by the relationship manager, which is passed back and forth between these stakeholders. Due to a lack of centralized systems, the sales unit spends a significant amount of time in nonsales activities; i.e. data collation and follow-ups. Some key deficiencies in the existing process are as follows (Note: TAT stands for turn around time):

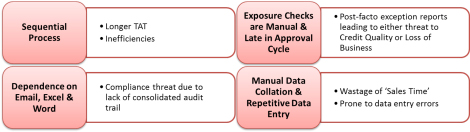

Figure 2: Issues with Typical Credit Approval Process

A. Sequential process with lack of transparency and predictability

Currently, in the loan lifecycle, it is difficult for the previous stakeholder to know exactly what or who is working on the loan proposal. This leaves the relationship manager left in the lurch trying to provide an updated status to the customer, since the relationship manager would not be aware of the proposal status. The RM may also not be aware of the reasons for rejection of a proposal which could, for instance, lead to the same type of credit being sourced again and getting rejected, leading to a waste of precious resources

Currently, in the loan lifecycle, it is difficult for the previous stakeholder to know exactly what or who is working on the loan proposal. This leaves the relationship manager left in the lurch trying to provide an updated status to the customer, since the relationship manager would not be aware of the proposal status. The RM may also not be aware of the reasons for rejection of a proposal which could, for instance, lead to the same type of credit being sourced again and getting rejected, leading to a waste of precious resources

B. Manual data collation and repetitive data entry

Corporate loans are quite complex, hence the associated documentation needed for comprehensive analysis is also varied and expansive. Currently, either the relationship manager or his or her team collect and collate this information for inclusion in the loan proposal. In some cases, it is entirely possible that the person might not know the reason why certain information is needed or where it fits which could lead to the customer having to provide the same information more than once.

C. Dependence on email, Excel and Word

Bank-wide mid-year policy changes are typically circulated to all stakeholders through emails. The biggest challenge in this approach is the risk of someone having missed seeing the email or skipped reading the same or even having forgotten the contents of the email. Moreover, this is an area that the regulators want to fix as there is no consolidated proposal evaluation summary and that makes it difficult to fix responsibilities, for audit purposes.

D. Exposure checks are manual and late in approval cycle

Today, neither sales nor the credit desk is armed with real-time data on budgets and limits, and the bank’s current standing against them. More often than not, exposure related checks are done only when a proposal reaches the credit desk. Precious resources get wasted in sourcing and processing a loan proposal that might get rejected at a later stage in the loan life cycle. This might have ramifications on customer relationships also, as it could disrupt the business plans of the customer.

Solution Considerations

Finding an ideal solution that can address all the above challenges is quite tricky as:

• Banks want automation without compromising on decision making. There is tremendous scope for bringing automation, thereby minimizing user involvement to only where it is absolutely necessary—i.e. decision making. The solution should provide an effective platform for collating and disseminating relevant data to decision makers.

• Banks need early warning triggers at a portfolio level. Today, banks work with end-of-day reports that can make risk management reactive. Changes in account behavior, utilization patterns, and impending breach of covenants are some of the areas that banks want to track proactively.

• Banks want to avoid undertaking a large scale transformation program. While it is inevitable that introduction of a new solution would bring about some change in the way the bank works, the key here is to limit the change. An ideal solution would enable the bank to conduct its business processes without spending too much time and money in either customizing the solution or redoing the business processes. Additionally, if the bank wants to change a process at a later point in time, it should be able to do so, relatively easily.

Business Processing Modeling Tools as possible alternatives

The inherent advantage of BPM tools is that they allow an easy-to-use interface for orchestrating business process which can be optimized over time. This coupled with a data collation and an aggregation engine can provide an effective solution that can address the four key issues with current procedures.

The inherent advantage of BPM tools is that they allow an easy-to-use interface for orchestrating business process which can be optimized over time. This coupled with a data collation and an aggregation engine can provide an effective solution that can address the four key issues with current procedures.

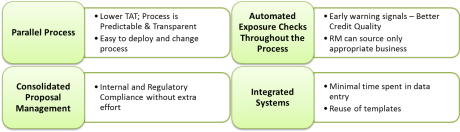

Figure 3: Key Facets and Benefits of the BPM approach

Some inherent features of BPM tools which directly address the needs are:

• Process modeling instead of coding—Unlike retail lending, corporate lending processes vary significantly across banks. This makes customization and implementation of traditional applications both costly and time consuming. Since the underlying activities remain the same across banks, BPM tools provide an effective platform to model the relevant process without undertaking large technology projects.

• Optimized process—Banks can configure the process to enable execution of steps as and when relevant data is captured. This approach will not only improve operational efficiencies, but also provide early warning signals for any non-compliance with lending policies and exposure budgets. Here’s a sample optimized process flow:

Figure 4: Optimized Credit Approval Process (Representative Sample Only)

• Leverage existing tools and templates—Banks can decide to retain some of the existing tools/templates/applications because they want to retain it in long term or because they are too difficult to replace in short term. Thus banks can focus on implementing an optimized process, rather than spending time and money on changing the existing applications.

Conclusion

While there are a lot of options on which a solution can be modeled, there is no denying the fact that such a solution is the need of the hour. By improving the efficiency and effectiveness of business processes along with an automated workflow management process, BPM technology can greatly reduce cycle times, improving a bank’s responsiveness and profitability. More important, a better decision can be made, since all the related information is provided at a single place. The ultimate benefit of a BPM-based solution is its ability to help a bank orchestrate the loan appraisal process with its own time-tested processes.

While there are a lot of options on which a solution can be modeled, there is no denying the fact that such a solution is the need of the hour. By improving the efficiency and effectiveness of business processes along with an automated workflow management process, BPM technology can greatly reduce cycle times, improving a bank’s responsiveness and profitability. More important, a better decision can be made, since all the related information is provided at a single place. The ultimate benefit of a BPM-based solution is its ability to help a bank orchestrate the loan appraisal process with its own time-tested processes.