Portfolios meet “Trump effect”

Higher rates after Trump win mean good things for bank loan yields

- |

- Written by S&P Global Market Intelligence

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

By Nathan Stovall and Chris Vanderpool, S&P Global Market Intelligence staff writers

Loan yields at U.S. banks appear to be stabilizing, and the election of Donald Trump as the country's next president could help send them higher.

Since the U.S. election last week, long-term rates have risen considerably. Investors have sold long-term Treasurys on the belief that Trump will increase the deficit by boosting infrastructure spending while cutting taxes. [S&P Global posted this article originally on Nov. 16.]

The yield on the 10-year Treasury jumped 35 basis points in the aftermath of the election, rising to 2.23% at one point, the highest level since January. The move up in the benchmark 10-year follows increases in key short-term rates like the three-month LIBOR, which hit new 52-week highs early in the third quarter ahead of money market reforms in mid-October.

Both moves should alleviate pressure on banks' security and loan portfolios, particularly with the yield curve steepening. The spread between the 2-year and 10-year Treasury yield expanded to as wide as 123 basis points with the recent moves, well above the low point of 76 basis points during the summer and the average spread of 96 basis points seen throughout 2016.

Higher long-term rates will reduce reinvestment risk in banks' bond portfolios, and the expansion should offer a lift to prices on new loans. That relief would be welcome since loan yields have been under pressure at banks of all sizes since the financial crisis.

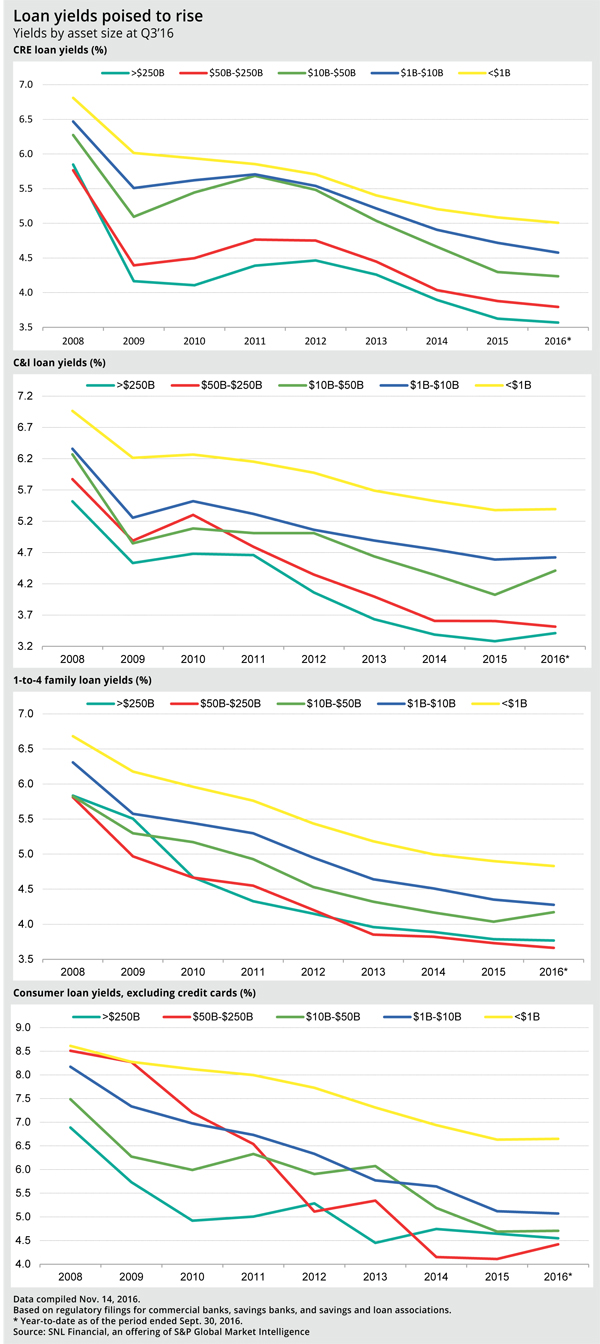

CRE loans likely to post greatest gain

Commercial real estate yields should benefit the most from the recent changes in rates and the competitive environment. Through the first nine months of 2016, CRE loan yields remained under pressure at banks across various asset groups, falling in the range of six to 14 basis points from 2015 levels. Since the financial crisis, the most significant CRE yield compression has occurred at the nation's largest institutions, those with assets over $250 billion.

There is hope that pressure will abate as regulatory scrutiny over elevated CRE exposures has prompted some institutions to leave their respective markets. While bankers had not seen much of a change in CRE pricing during the summer, when rates remained near historical lows, they told a different story during third-quarter earnings season, noting that pricing is beginning to inch up.

Some bankers suggested that regulators have been wise to blow the whistle on CRE and encouraged others to proceed with caution. Banks reported in the Federal Reserve's latest senior loan officer survey that standards had tightened on all types of CRE loans. Banks also reported strong demand for CRE loans, suggesting they could continue to attract borrowers even at higher rates.

Higher rates in the residential mortgage market could deter some borrowers and at the very least serve as a headwind to strong refinancing activity that occurred during the sustained period of lower long-term rates in the summer. Mortgage rates have already moved higher since the election and could offer support for waning yields on 1- to 4-family loans.

Taking a reading on C&I loans

Meanwhile, short-term rates such as the three-month LIBOR increased months before the election and appear to have already offered a lift to commercial and industrial loan yields. Through the first nine months of 2016, the banking industry's aggregate C&I loan yield rose seven basis points from 2015 levels. The yield expanded at banks in every asset group, save for institutions with assets between $50 billion and $250 billion.

Bankers indicated in the recent senior loan officer survey that C&I loan demand could be weak, but a number of institutions said during third-quarter earnings season that the uncertainty over the election negatively impacted growth. A net 9% of banks, however, noted in the loan officer survey that they decreased spreads on C&I loan rates over their funding costs to large and medium-sized firms, compared to 6% in the prior survey. Just a net 6% decreased spreads to small firms, down from 13% in the prior survey. The net percentage is the difference between the percentages of bank loan officers reporting spread easing versus tightening.

Some greater clarity in the aftermath of the election coupled with continued increases in the three-month LIBOR, which hit another 52-week high Nov. 14, could offer a boost for C&I loan yields and other credits tied to floating rates.

Some market observers expect rates to move even higher. Fed futures continue to suggest the central bank will increase the fed funds rate by 25 basis points in December, while investor and bond expert Jeffrey Gundlach argued last week that the 10-year yield could rise to 6% in the next five years due to Trump's policies.

No matter when changes come to pass, signs suggest that pressure on banks' loan yields could soon be a thing of the past.

This article originally appeared on S&P Global Market Intelligence’s website under the title, "Higher rates after Trump win mean good things for bank loan yields"

Tagged under Bank Performance, Risk Management, Rate Risk, Community Banking, ALCO,