M&A breeze picks up in Windy City

Wintrust triple-play could start open-bank M&A tempest in Chicago

- |

- Written by SNL Financial

By Kiah Lau Haslett and Robert Downey III, SNL Financial staff writers

Wintrust Financial Corp. opened 2015 with a bang, announcing three deals in five weeks, but the wave of open-bank deals for the Windy City may just be starting to gather steam.

Wintrust announced it would acquire nearly $1 billion in assets through three bank deals announced within a little more than a month. But this may just be the beginning of Chicago's M&A wave. As failures have receded, more sellers may come to the market looking for a buyer and create more opportunities for acquisitive institutions like Wintrust, according to the investment banker who advised two of the sellers.

Making of Wintrust’s deals

Wintrust was "very, very" active in M&A discussions with potential sellers throughout 2014, executives said during the bank's third-quarter earnings call, and management previously said they are partial to smaller acquisitions because they tend to be less disruptive to the company and offer a cultural fit.

Courting smaller banks can also mean less competition from other community banks, and the preference has differentiated the company as it cobbles deals together in order to make a more meaningful impact to the bank, said FIG Partners analyst John Rodis.

The latest deals go along with that playbook.

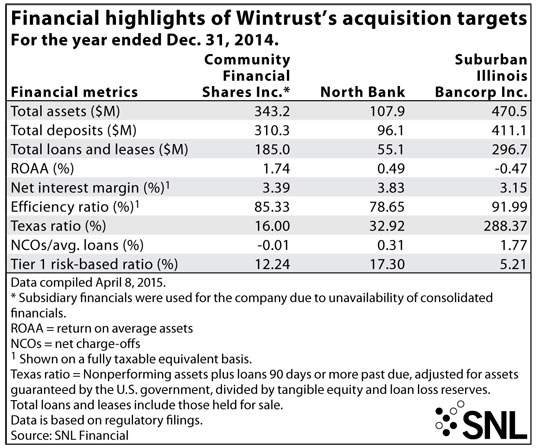

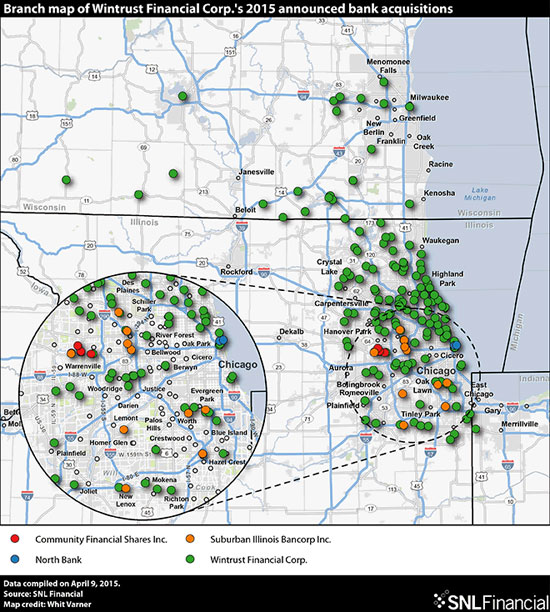

• Wintrust announced March 2 that it had agreed to acquire Glen Ellyn, Ill.-based Community Financial Shares Inc., which had $343.0 million in assets as of yearend 2014, for a reported deal value of $42.4 million.

• Wintrust followed with another announcement March 30 that it had agreed to acquire Chicago-based North Bank for a reported deal value of $17.0 million. North Bank had $107.9 million in assets as of year-end 2014.

• Wintrust then announced April 2 that it had agreed to acquire Elmhurst, Ill.-based Suburban Illinois Bancorp Inc. for a reported deal value of $12.5 million.

The three deals would bring total acquired assets of $921 million, total acquired loans of $537 million, and total acquired deposits of $817 million, Sandler O'Neill analyst Brad Milsaps wrote in an April 6 report following the Suburban Illinois deal.

Wintrust paid about $72 million in total, which Milsaps said "seems reasonable relative to what a $1 billion Chicago franchise would fetch." The three deals will improve profitability and provide "ample" cost saves from branch consolidation. He estimated that they could add between 8 cents and 12 cents to 2016's EPS if Wintrust could generate 80 to 90 basis points on the acquired assets.

More M&A may be on the way—with a twist

There could be more deals coming for the Windy City. Chicago is in the "opening innings" of its own consolidation wave after lagging many markets across the United States, said Eugene Katz, an investment banker at D.A. Davidson. Katz worked with the management teams at North Bank and Community Financial in their mergers with Wintrust and his comments to SNL were limited to the general marketplace.

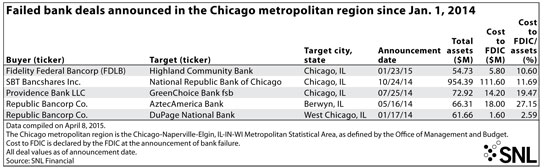

He said banks in Chicago mulling open-bank deals had to consider the opportunity cost of FDIC-assisted transactions in the past. The number of troubled banks in the state meant buyers may have focused more on failed-bank deals, with would-be sellers waiting on the sidelines for the wave of failed banks to peter out. Now that the tide of failures has receded, Katz said to watch for the rise of open-bank acquisitions.

"In Chicago, we're finally at the end of that rope. There's really nothing left of any size that is problematic and so folks started looking at open-bank transactions, which is something that's been going on across the across the country for two to three years now. We just haven't had as much of it here in Chicago," he said. "I think that's one of the reasons why you're seeing this pent-up demand to sell come to the surface. Potential sellers have figured out that banks are not failing and even the problem banks [are] salvageable."

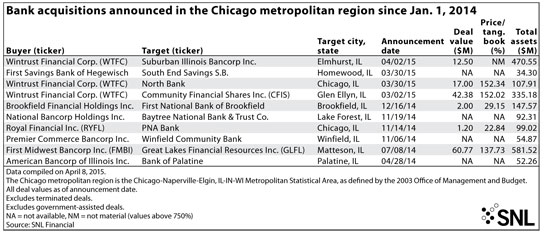

Including Wintrust's three announced deals, there have been five bank deals announced in the Chicago metropolitan area year-to-date, according to SNL data; only one was for a failed bank. There were 10 deals in the Chicago area for all of 2014, including four that were FDIC-assisted.

The pent-up demand could even create more sellers than buyers, Katz said. The types of banks apt to sell now are those that are troubled but not expected to fail, as well as clean banks that may be grappling with succession and growth concerns. He also said deal prices are beginning to "firm up" but remain below historical levels, creating an opportune environment for sellers and buyers. At the time of Wintrust announcement, Community Financial had a deal value to tangible common equity of 152.0%; North Bank had an announced deal value to tangible common equity of 152.3%, according to SNL.

Wintrust, the juggler

This is not the first time that Wintrust has juggled multiple deals from announcement to close. It acquired failed banks Lincoln Park Savings Bank and Wheatland Bank on the same day in April 2010. It announced a deal for HPK Financial Corp. and a failed-bank deal for First United Bank within 11 days of each other in 2012. It also announced two branch deals within days of each other in April 2014.

Rodis said management has maintained and defended its regulatory "gold standard," which has allowed it the flexibility to do several deals at the same time. The comparatively small size of the deals and Wintrust's multiple bank charters may make the deal more palatable for regulators and integration easier.

The pro forma company will have about $21 billion in assets, but Rodis believes the bank will remain disciplined when it comes to deal-making. He said today's regulatory environment discourages banks from approaching $50 billion in assets. He does not see Wintrust combining with a larger regional in Chicago at this time to get larger.

"I think maybe $25 billion to $30 billion [in assets] is certainly realistic. I think beyond that is harder to say," he said.

Read an SNL Financial reprint of this article

Tagged under Management, Financial Trends, CSuite, Community Banking, Feature, Feature3, M&A,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story