Mergermakers target smaller banks

SNL Report: Bank M&A hums along in Q2'15, but average deal size shrinks

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Kevin Dobbs, SNL Financial staff writer

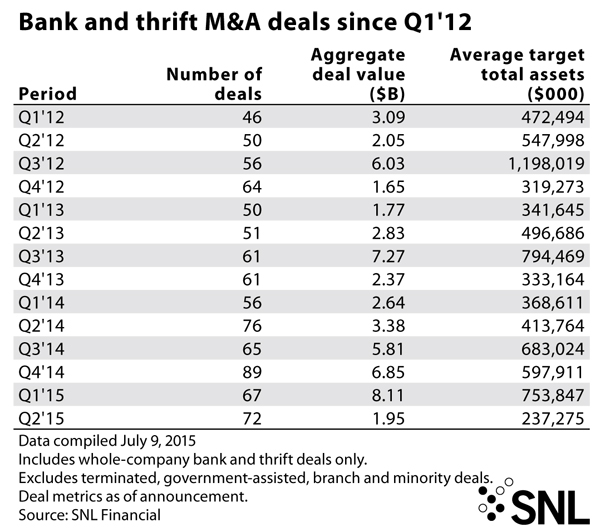

Bank M&A activity continued at a steady pace during the second quarter, but the average size of targets dropped substantially from previous periods.

Observers attributed the shift to multiple factors, including an anticipation of rising interest rates among some sellers and regulatory distractions among larger would-be buyers.

An SNL Financial analysis found that there were 72 whole-bank deals announced during the second quarter, comparable to the 67 deals announced during the first quarter and in the same ballpark as each of the final two quarters of 2014.

Aggregate deal values, however, were notably lower as the typical target was much smaller. The average asset size of sellers in the second quarter was a little more than $237 million, down notably from each of the three previous quarters, the analysis shows. The second-quarter figure marked the lowest average target size in a given quarter in more than three years.

What’s driving size shift

Keefe Bruyette & Woods analyst Michael Perito told SNL that there were key contributors to this development.

On the seller side, he said, some banks that had considered selling amid fierce competition for loans and net interest margin pressure started to look ahead to a rising interest rate environment. Many observers, including Perito, are anticipating that Federal Reserve policymakers will start to boost short-term rates after their September meeting.

"There is some hesitancy to sell ahead of it," Perito said of the anticipated rate hike, noting that many asset-sensitive banks, particularly those large enough to compete for bigger loans, are positioned to benefit from higher rates. Sellers' core deposit bases could also become more valuable.

Therefore, he said, some potential sellers could see their valuations improve when rates do go up and that could help them attract higher offers from buyers. "They want to see how the market perceives them when rates rise," Perito said.

On the buyer said, Perito said the Dodd-Frank Act stress testing that many banks in the range of $10 billion to $50 billion in assets were wrapping up in the second quarter likely distracted some would-be buyers. "I think that definitely caused some pause," he said.

He also noted that some larger buyers—those more likely to go after bigger targets—in recent months probably have taken a wait-and-see stance, hoping to see previously announced large deals earn regulators' nod and get closed before they pull the trigger themselves.

Perito noted that regulators have closely scrutinized large-scale deals, and he pointed to M&T Bank Corp.'s long-delayed plan to buy Hudson City Bancorp Inc. as a case in point. Regulators have delayed that deal several times since it was announced in August 2012 because of Bank Secrecy Act and anti-money laundering compliance concerns.

Simple mechanics influences deal pace

Matthew Veneri, co-head of investment banking at FIG Partners LLC, told SNL that another likely reason average targets were smaller in the second quarter is that there simply was a healthy number of larger community banks active on the deal front in the second half of 2014 and early this year.

These banks needed time to close and integrate those deals, he said, meaning several acquisitive banks were temporarily on the sidelines during the second quarter.

"They needed time to digest what they already had on their plates," he said. "That's caused a lull."

Veneri cited Moultrie, Ga.-based Ameris Bancorp as an example. It closed a deal in June 2014 and then another in May of this year. The targets were both well over $400 million in assets and they followed another acquisition that Ameris closed in 2013; that one involved a target with assets of more than $700 million.

Veneri anticipates that Ameris will get back on the deal path in the second half of this year, as will others like it, and that could drive up the average size of targets.

Perito agreed and said that even larger regionals could soon rejoin the M&A picture. He and other analysts are expecting word on the M&T-Hudson City deal this fall. And he noted that BB&T Corp. received regulatory approval this month to close its $2.5 billion acquisition of Susquehanna Bancshares Inc. That latter development could "encourage" bigger buyers to start looking anew at M&A, and they are likely to look at targets larger than the typical one that sold in the second quarter.

Smaller in size, but flow keeps going

In the meantime, the volume of deals did hold up in the second quarter, in large part because the smallest banks continued to struggle under the weight of heavy regulatory burden, and many of them do not see higher rates as the cure-all for their challenges, observers say.

These sellers have reasonable price expectations and are relatively easy to digest, and as such buyers have continued to actively gobble up these targets, Veneri said. "Expectations are realistic at the lower end of the spectrum," he said, "and that's allowing deals to continue to get done."

Recent examples from June include Canfield, Ohio-based Farmers National Banc Corp.'s plan to purchase East Liverpool, Ohio-based Tri-State 1st Banc Inc. ($139.5 million) for about $14.2 million, and Los Angeles-based PBB Bancorp's deal to acquire Big Bear Lake, Calif.-based First Mountain Bank ($145.6 million) for about $13.4 million.

SNL calculated the Farmers National-Tri-State 1st Banc deal value to be 130.0% of book value, on par with the pricing of bank and thrift deals in the Midwest over the preceding 12 months. SNL pegged the value of the PBB Bancorp-First Mountain deal at 104.0% of book, below the going rate in the West.

Perito said the combination of small deals continuing to accumulate and his expectation that larger buyers will get back into the mix leaves him optimistic that deal activity will be strong in 2016 and outpace this year.

"It feels like '16 is setting to be an active year," he said.

What's more, Perito added, the U.S. landscape remains heavily banked and ripe for consolidation. He noted that the top 10 biggest banks hold more than half of the nation's banking assets, leaving more than 6,000 other banks to wrestle each other for the rest of the pie.

"In general, it's still very much over-banked," he said.

About the author

Kevin Dobbs is a senior reporter and columnist for SNL Financial. The views and opinions expressed in this piece represent those of the author or his sources and not necessarily those of SNL. Share your thoughts at [email protected]. Follow on Twitter @Kevin1Dobbs. Jack Chen contributed to this article.

This article originally appeared on SNL Financial's website as "Bank M&A hums along in Q2'15, but average deal size shrinks."

Tagged under Management, Financial Trends, CSuite, Community Banking, Feature, Feature3, M&A,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story