Valley of consumer gripes

Looking for Wells Fargo-like risks in CFPB's complaint database

- |

- Written by S&P Global Market Intelligence

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

By Zach Fox and Zuhaib Gull, S&P Global Market Intelligence staff writers

Recently blogger Lucy Griffin wrote in “‘Wells Problem’: How could you stop it in your bank?” of the need for an individual bank to sift their complaints for a problem like the Wells Fargo affair. This S&P Global Market Intelligence article takes a wide span view of the matter.

It is easy to find plenty of consumer complaints about unauthorized accounts at numerous financial institutions. Whether those complaints will translate to regulatory action is another matter.

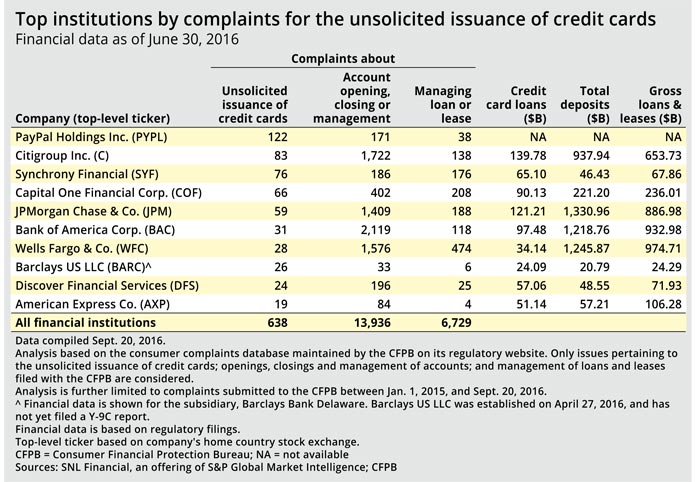

As Wells Fargo & Co. continues to deal with fallout from $185 million in fines after employees opened more than 2 million deposit and credit card accounts that may not have been authorized by consumers, cross-selling practices have become a focus for regulators. Since Jan. 1, 2015, consumers have filed 638 complaints with the Consumer Financial Protection Bureau regarding unsolicited issuance of credit cards.

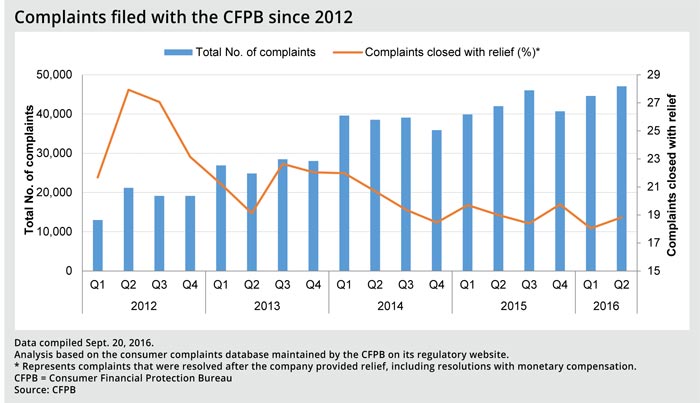

Financial institutions have criticized the CFPB's complaint database as faulty. The regulator will make some effort to confirm the customer has a relationship with the named institution, but the CFPB does not verify other details. Nonetheless, it seems clear that the CFPB uses the database as a jumping-off point for investigations.

"Consumer complaints are the CFPB's compass and play a central role in everything we do. They help us identify and prioritize problems for potential action," said CFPB Director Richard Cordray in July 2015.

Among the 638 complaints for unsolicited credit card issuance, Wells Fargo accounted for 28 complaints, the seventh-highest total. Although nominally small, the figure appears worse when accounting for the size of Wells Fargo's credit card business. Bank of America Corp.'s credit card business is more than twice as large, but the bank only had three more complaints.

One company stands out when looking at unsolicited issuance complaints: PayPal Holdings Inc. The company was the subject of 122 complaints, nearly 50% more than the next company, Citigroup Inc., which has the largest credit card portfolio among U.S. banks. PayPal does not disclose the size of its credit card business.

PayPal offers a line of credit option previously known as Bill Me Later, rebranded as PayPal Credit and backed by Comenity Capital Bank. PayPal also has a PayPal Extras Mastercard product, which is issued by Synchrony Bank.

PayPal did not respond to requests for comment.

PayPal has already been hit over its Bill Me Later product. In May 2015, the CFPB fined the company $10 million and ordered $15 million in consumer redress. While consumer complaints are always concerning, there is reason to believe the CFPB is comfortable with PayPal's approach, said Sanjay Sakhrani, an analyst with Keefe Bruyette & Woods who covers the company.

"I feel like this is something that the CFPB has definitely vetted, and I think PayPal has been working with them to improve their disclosures," Sakhrani said in an interview.

The CFPB's consent order against PayPal required that the company stop using PayPal Credit as the default option for payment, among other things. The rate of unsolicited issuance complaints against PayPal has not changed significantly since the CFPB action. From January 2015 through May 2015, the company was the subject of 29 such complaints, or roughly 5.8 per month. From June 2015 through September 2016, the rate was almost exactly the same, 5.8 per month.

In a Sept. 21 note, Piper Jaffray analysts examined the CFPB complaint database for risks among banks. They believe Citizens Financial Group Inc. faces significant risk considering an elevated number of complaints and a focus on cross-selling practices. Still, the analysts like the company based on valuation and expected earnings growth.

Wells Fargo was the subject of a significant number of complaints regarding bank account opening, closing or management and regarding managing a loan or lease. But those complaint figures appear to be in line with other money-center banks like Bank of America, JPMorgan Chase & Co. and Citigroup. To an extent, significant complaint volume is unavoidable for banks that large, said Rick Fischer, a senior partner with Morrison Foerster.

"It's the nature of servicing literally tens of millions of consumers," he said.

Fischer said the complaint database can provide valuable insight into areas of focus for the CFPB. For example, Fischer said his firm started work on debt collection practices before the CFPB released its study as the volume of complaints made it clear the industry would become a focus.

Tristram Wolf, an associate with law firm Ballard Spahr and a former investigator for the CFPB, said companies should pay close attention to the database to monitor reputation risk and prepare for exams. But Wolf said the CFPB will rarely start an enforcement action based on a complaint, which is handled by the regulator's consumer response division. Rather, the agency's supervisory division will use the database to determine the scope of an exam and the questions to ask. And he said the enforcement division will consult complaints for additional support.

"Enforcement pretty regularly reaches out to consumer response for consumer complaints that can support ideas that they have or enforcement actions they might be interested in," Wolf said in an interview. "As a general matter, the flow between the consumer complaint unit and enforcement is generally driven by enforcement."

For more about CFPB procedure, read, “Q&A: Understanding CFPB’s mindset”

This article originally appeared on S&P Global Market Intelligence’s website under the title, “Looking for Wells Fargo-like risks in CFPB's complaint database”

Tagged under Retail Banking, Compliance, Customers, CFPB, Feature, Feature3,