Checking out regulatory math

How close do regulators come on compliance time burden?

- |

- Written by Nancy Derr-Castiglione

- |

- Comments: DISQUS_COMMENTS

Regulators periodically publish their estimates of how long it takes to comply with information collection requirements. Nancy Derr-Castiglione does a bit of math, for the "fun" of it.

Regulators periodically publish their estimates of how long it takes to comply with information collection requirements. Nancy Derr-Castiglione does a bit of math, for the "fun" of it.

If you’re an avid reader of the daily Federal Register as I am, you probably notice, but quickly pass over, the numerous Agency Information Collection Activities Notices that propose for comment renewal of existing information collections.

These are accompanied by “burden estimates.” The burden estimates are the total number of hours the affected regulated entity spends on the information collection or recordkeeping requirement—that is, according to the agency.

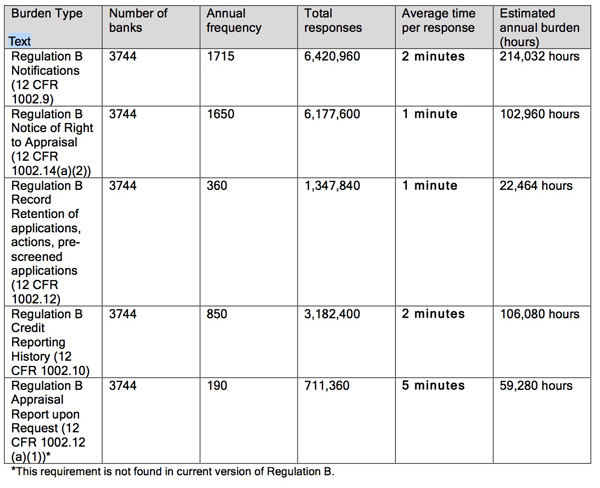

Recently, one such notice of agency information collection caught my eye. It was published by FDIC in July in the Federal Register relating to Regulation B recordkeeping. It contained a more detailed breakdown of estimated burden hours for Regulation B recordkeeping for state nonmember banks than is usual.

There were also burden hour estimates for the optional self-test provisions of Regulation B that do not automatically apply to all banks that are not included above.

Crunching the numbers

The total burden hours for the reporting and recordkeeping elements of Regulation B for state nonmember banks—according to FDIC’s estimate—is 504,816 hours per year. On a per bank basis, that comes out to 134.83 hours per year. (However, the 59,280 hours attributed to the “Appraisal Report Upon Request” requirement may be an historic requirement rather than a current regulatory collection.)

My unscientific analysis of this information identifies a couple of problems with the FDIC estimate of burden.

First, the number of minutes attributed to each average response time for each activity appears to be significantly understated.

For example, the requirement to provide notifications under Regulation B encompass adverse action notices to declined applicants, both consumer and most businesses, as well as existing accounts that are terminated. It includes notifying applicants of incomplete applications and the information required to complete an application.

Assuming someone else has made the credit decision and provided the reason(s) for the decision (who is not counted in this burden estimate), someone has to prepare the notification with the correct customer contact information and place it in the mail or delivery system and retain it in the customer’s file.

I believe that would take more than 2 minutes.

Let’s say, it only takes 5 minutes to do all that.

The burden estimate for Regulation B Notifications would really be 535,080 hours (instead of 214,032 hours).

Second, the burden estimates don’t really reflect the whole picture.

Looking specifically at the customer notifications requirement of Regulation B. The regulatory burden relating to notifications is not just the 2 or 5 minutes it takes to send out the adverse action letter to the customer as required under 12 CFR 1002.9.

There is periodic compliance training that has to take place. There has to be a compliance monitoring program in place where the process is reviewed periodically. There is generally a second review that takes place in which a second person is looking at that customer letter before it goes out to be sure it is in compliance with Regulation B (which will double the number of minutes right there).

The estimate of 1 minute per response to provide an appraisal notice as required by 12 CFR 1002.14(a)(2) of Regulation B is probably not a bad estimate. That notice is generally combined with other disclosures that are provided at the same time and are also being sent to the customer.

However, the burden estimate for this regulation does not consider the next step after the notice, which is the requirement to provide the borrower with a copy of the appraisal. The appraisal has to be copied and mailed or delivered to the borrower within prescribed time frames.

You could easily double each of these burden estimates for Regulation B that FDIC has provided, plus add a considerable number of minutes or hours for Regulation B compliance.