As Fed hike looms, LCR impact weighed

LCR leaves questions about deposits when rates rise

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Nathan Stovall and Tahir Ali, SNL Financial staff writers

The liquidity coverage ratio has already transformed some banks' deposit bases and could have significant impacts on the market when interest rates rise.

Banks' efforts to comply with the regulatory provision have changed the composition of their investment portfolios, increasing the concentration of lower-yielding securities on their balance sheets.

The liquidity coverage ratio, or LCR, has also significantly increased the value of retail deposits for the nation's largest banks that are subject to the rule and is already causing some to change their deposit bases. Just how much it will increase the competition for deposits when rates rise, though, remains unclear.

About the LCR

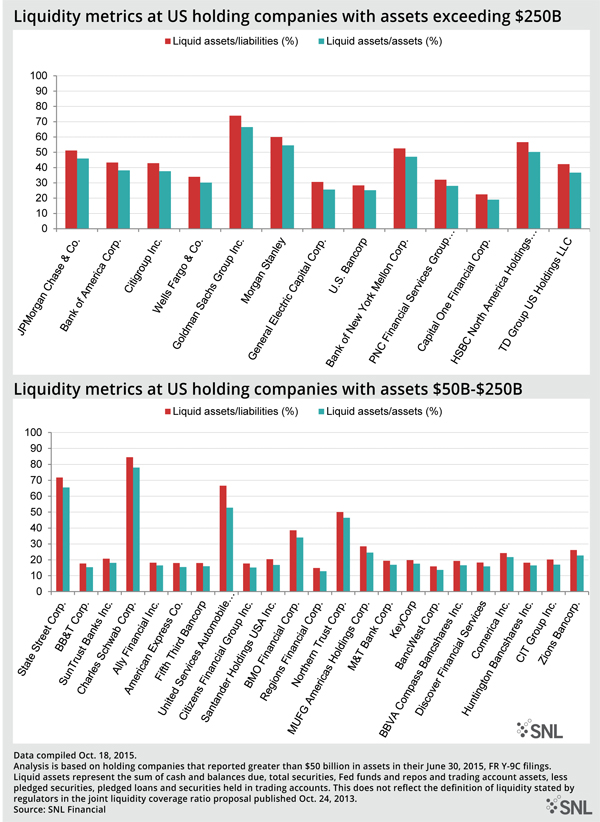

The LCR requires covered institutions to hold "high quality liquid assets" greater than, or equal to, their projected cash outflows minus their inflows during a 30-calendar-day stressed scenario.

The LCR applies to banks with more than $250 billion in assets or those with at least $10 billion in foreign banking assets and subsidiaries of those large banks with at least $10 billion in assets. Those institutions began complying with the LCR at the beginning of this year and have to reach full compliance by Jan. 1, 2017.

Banks with assets between $50 billion and $250 billion are subject to a less-stringent LCR and will not have to begin complying with the rule until Jan. 1, 2016, but most institutions falling in that asset group have already taken steps to meet the requirement.

Many institutions subject to the rule have already built the adequate amount of high-quality liquid assets, or HQLAs, on their balance sheets. However, there remains some debate over the potential inclusion of municipal bonds as HQLAs under the LCR. Some critics have argued that munis should be considered HQLA because they are low risk, have fairly strong liquidity and proved to less susceptible to a systemwide shock during the last downturn.

Regulators have also taken different stances on the issue. Ethan Heisler, a managing director at Citigroup, wrote in a recent newsletter for bank treasury clients that there still is not clarity from U.S. regulators on the treatment of munis. He said the Fed recognizes some of the securities as level 2B HQLA, while the FDIC and OCC do not. Efforts in Congress to force regulators to recognize munis as level 2A HQLA have also proved unsuccessful to date, he said.

LCR impact on deposit market

How the LCR will change the deposit market has been the subject of even more debate. At banks with more than $250 billion in assets, FDIC-insured deposits are assigned a 3% outflow rate under the LCR, while noninsured deposits, including corporate deposits, receive outflow rates of 10% to 40%. Those two categories of deposits will receive outflow rates of 2.1% and between 7% and 28%, respectively, at banks subject to the less stringent LCR.

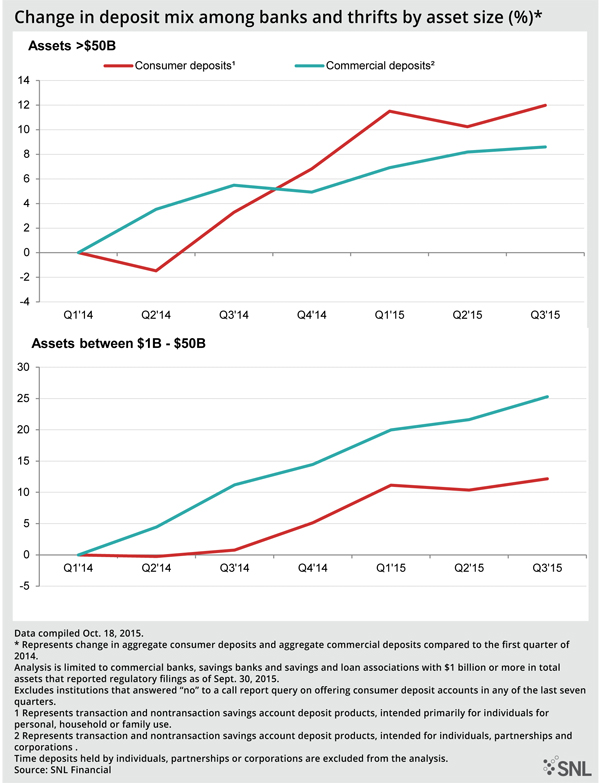

Banks, particularly those already subject to the LCR, have worked to reduce non-LCR friendly commercial deposits. Those efforts are evident, with the nation's largest banks growing commercial deposits at slower rates than their smaller counterparts. SNL data show that banks with more than $50 billion in assets have grown corporate deposits more slowly than smaller institutions, increasing those balances by 8.6% since the first quarter of 2014, when corporate and consumer data was first made available. Comparatively, banks with assets between $1 billion and $50 billion have increased those balances by 25.3% during the same period.

Meanwhile, banks with more than $50 billion in assets have grown their consumer deposits by 12.0% since the first quarter of 2014. Banks with assets between $1 billion and $50 billion have grown those balances by nearly 12.2% during the same period.

JPMorgan Chase & Co. has actively transformed its deposit base perhaps more than any other large bank. JPMorgan executives said at an investor conference in mid-November that it reduced non-operational deposits across the company by more than $150 billion. The company, however, believes that there is no historical reference for how the deposit market might behave when interest rates do move higher given changes in regulation.

"Given … the new regulatory framework, the battle for core operating deposits is much different. So what we're doing is just trying to be prepared as possible, making sure we're talking to our clients, watching our competitors, making sure we have the right mix of products," Doug Petno, CEO of JPMorgan's commercial banking division, said at the BancAnalysts Association of Boston conference earlier this month, according to the transcript.

Capital One Financial Corp. CFO Stephen Crawford expressed a similar viewpoint at the same event. He said that everyone should admit some humility to predicting changes in the deposit business when rates rise due to many changes in the financial system. For instance, he said the money market business has changed, the size of the Federal Reserve's balance sheet has grown and noted that regulators are now stressing liquidity much more through provisions such as the LCR.

"I mean there is a whole bunch of reasons why anybody should be cautious … about what they think is going to happen to deposits," Crawford said at the event, according to the transcript.

Downloand PDF of SNL article.

Tagged under ALCO, Management, Financial Trends,