M&A speeding up by volume

SNL Report: Industry-level consolidation rises in '15, expected to continue

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Mohsin Azam and Nathan Stovall, SNL staff writers

A larger percentage of the banking industry consolidated in 2015, and observers expect M&A activity to continue at a healthy pace in 2016 as persistently low interest rates and higher regulatory and compliance costs encourage banks to sell.

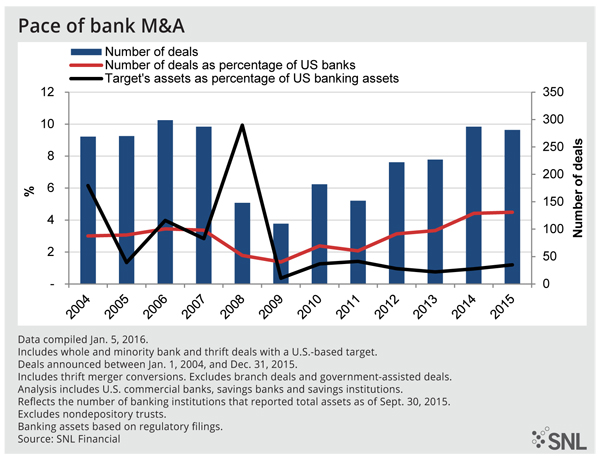

The number of announced bank deals in 2015 actually declined from year-ago levels, dipping to 281 transactions from 287 deals a year earlier. While fewer deals surfaced in 2015, a greater percentage of the industry consolidated during the period.

In 2015, announced bank deals equated to nearly 4.6% of banks in the industry, the highest percentage of consolidation since 2004. In 2014, announced bank deals equated to nearly 4.4% of banks in the industry. From 2004 to 2013, the measure ranged from 1.4% to 3.4%, according to SNL data.

Bank observers believe the drivers of M&A remain intact as the industry faces continued profitability pressures from prolonged low interest rates, necessary technology investments, and costly compliance with regulation. Banks are also not expected to receive the same boost from reserve releases as they have in years past.

"Even as interest rates rise, the slow and incremental increase will not be enough to boost profitability for banks in a meaningful way in the short term," Christopher Wolfe, a managing director in financial institutions at Fitch Ratings, said in report providing the firm's outlook for 2016. "Bank earnings growth is expected to be somewhat muted given the expectation of rising provision expenses, limited improvement to margins over the next 12 months, and continual compliance and regulatory-related investments."

Size and coming deals

Fitch and members of the analyst community believe the majority of deal activity will come from smaller institutions agreeing to sell, but there is some hope that larger transactions will become more common in 2016.

2015 produced five bank deals with values over $1 billion, a notable pickup from prior years. In each of 2014, 2013 and 2012, just two bank deals with values over $1 billion surfaced, while three deals apiece with values over $1 billion were announced in 2011 and 2010, according to SNL data.

The median size of targets, at least relative to the size of buyers, also increased last year, rising to 17.53% of the buyers' assets from 13.58% in 2014 and 15.19% in 2013.

The sell-side community believes larger deals could pick up as more regional banks become confident with M&A under the framework of the Comprehensive Capital Analysis and Review, or CCAR. That exercise subjects banks to annual stress testing, limiting how much capital they can leverage and return to shareholders.

Not every large regional bank is interested in pursuing acquisitions either. The Evercore ISI bank analyst team noted in a Jan. 4 report that BB&T Corp., M&T Bank Corp., Regions Financial Corp., Synovus Financial Corp., and First Horizon National Corp. have expressed an interest in eventually expanding their markets through acquisitions, but the analysts said M&T's existing regulatory agreement, and the recent CRA rating downgrade at Regions could "temper" possible expansion plans. The analysts further noted that BB&T is taking a self-imposed 6- to 12-month break from deals to focus on integrating its planned acquisition of Allentown, Pa.-based National Penn Bancshares Inc. as well as its recently closed purchase of Lititz, Pa.-based Susquehanna Bancshares Inc.

Not that many other sizable regional banks have publicly discussed their M&A appetite. There simply are not that many publicly-traded banks with assets between $10 billion and $50 billion, and banks above that asset threshold must face the constraints of the CCAR process. SNL data show that there are 48 publicly-traded banks with assets between $10 billion and $50 billion that are not merger targets, possibly limiting just how many large bank acquisitions could occur.

Given such constraints, smaller institutions are still expected to make up the bulk M&A activity. Analysts believe that banks are beginning to recognize that scale is necessary to earn their independence, which could encourage further deal activity.

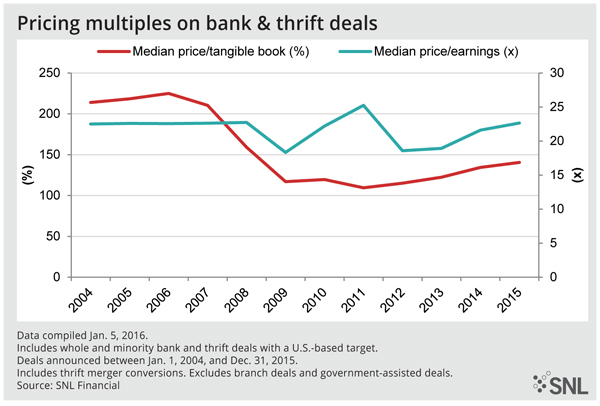

The prices that sellers have received in 2015 rose modestly. Bank deal prices rose to a median of 140.5% of tangible book value and 22.7x earnings in 2015, up from 134.4% of tangible book and 21.6x earnings in 2014, and 122.5% of tangible book and 18.9x earnings in 2013.

The small increase in median deal values came as bank stock multiples actually declined in 2015. Volatility grew in the markets last year and the SNL Bank & Thrift Index closed the year trading at nearly 165% tangible book value, down slightly from 175% at the close of 2014. However, buyers gained greater comfort with sellers' balance sheets, helping narrow the disconnect between buyer and seller expectations, Raymond James bank analysts wrote in a Jan. 8 report.

Acquirers also showed a willingness to pay up for larger transactions in 2015, with the median price on deals over $500 million in value rising to 219.4% of tangible book value and 22.9x earnings, up significantly from 147.9% of tangible book value and 15.4x earnings in 2014, according to SNL data.

Those deals have been far from the norm, leaving investors with few opportunities to select target franchises that could sell for a big payday.

Which M&A horses will investors bet on?

Picking the right potential targets with hopes of cashing out on a sale is easier said than done, and the holding period for a protracted M&A cycle may prove longer than initially expected, Raymond James bank analysts said in the recent report. The analyst team accordingly, once again, recommended selecting well-positioned acquirers that have the appetite, capital, and integration skills to execute deals that make financial and strategic sense.

"While pricing certainly comes into play and those incurring meaningful tangible book value dilution (or extended earn-back periods) could prove detrimental, we believe prudent deployment of capital via acquisitions will continue to prove fruitful for acquirers' stocks over time," the analysts wrote in the report.

Chris Vanderpool contributed to this article.

This article originally appeared on SNL Financial’s website under the title, "Industry consolidation rises in '15, expected to continue"

Tagged under Management, M&A, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story