Street gives thumbs up to RBC/City National deal

SNL Report: RBC's return to US largely welcomed, sparks big-bank M&A questions

- |

- Written by SNL Financial

By Nathan Stovall, SNL Financial staff writer

City National Corp. is not the old RBC Bank (USA).

The investment community seemed to recognize this much and believed that Royal Bank of Canada's $5.4 billion plans to return to the U.S. banking market through the purchase of City National made strategic sense. The Street said that City National offers an attractive private banking and wealth management platform focused on metro markets, and importantly, diversifies RBC's earnings away from the slowing Canadian economy.

Peter Routledge, an analyst at National Bank Financial, said he has argued for two to three years that RBC's biggest risk was that it receives far too great a share of earnings from Canadian personal and commercial banking and said he was not surprised that the company took action to address it.

"RBC's biggest risk remains an overreliance on Canadian personal, commercial banking for earnings. This transaction is a direct and unmistakable response to that risk," Routledge told SNL.

The risk of that exposure was somewhat validated this week, with the Bank of Canada cutting interest rates in response to the recent, dramatic decline in oil prices. Analysts noted that the move signaled that the Canadian central bank believed the plunge in oil prices would have a meaningful impact on the economy and slow growth. Canaccord Genuity analyst Gabriel Dechaine had already reduced his earnings forecast for Canadian banks the day before the rate cut, citing reduced net interest margins due to lower five-year bond yields and a slightly more conservative level of loan losses against the backdrop of potential job weakness in Canada.

RBC gains from City National deal

Routledge said that the acquisition of City National, however, will provide RBC with geographic diversification away from Canada and offer exposure to areas where the company wants to focus—high-net-worth clients in the U.S.

"It's a great time to be jumping into the U.S.," Routledge said. "It's one of the few developed-world economies where the growth outlook is reasonably optimistic."

RBC is paying 2.6x tangible book value per share and a market premium of roughly 26% to acquire City National. The deal is relatively small when measured against RBC's enormous balance sheet, but likely will bring additional regulatory scrutiny as the combined U.S. operations would have more than $50 billion in assets. RBC said that it included the potential regulatory hurdles, including being designated as a systemically important financial institution, in its deal assumptions.

Brian Klock, an analyst at Keefe Bruyette & Woods who covers both RBC and City National, said that the transaction shows that RBC felt comfortable coming back into the personal and commercial banking sector in the U.S., even if it means bringing additional regulatory burdens, because they are acquiring a high-quality franchise, with a strong management team.

"They feel comfortable enough buying this bank, this franchise, this management team despite all the regulatory burden that comes with being a SIFI bank. This wasn't a bank that was for sale, so they paid a premium for it, but that premium reflects the fact that they got a bank that they feel like they're not going to have all these regulatory issues with," Klock told SNL.

RBC's executives also touted the growth prospects that the City National franchise can offer in the future, predicting loan, deposit, revenue, and earnings growth to be, on average, greater than 10% through 2020.

"We haven't had revenue synergies talked about in a bank M&A deal in years. We haven't seen a 21x forward earnings multiple in a while either, but City National is different. If you've got this very asset-sensitive bank that is under-earning, the real earnings power of City National comes further out," Klock said.

Not only would City National's earnings increase if interest rates move higher, but Klock noted that RBC could shrink the company's large securities portfolio and deploy excess liquidity into higher-yielding commercial credits through its existing U.S. business. For instance, he noted that the RBC Capital Markets might book loans at an attractive rate of 4%, but it is currently financing those credits with wholesale funding because it lacks a U.S. deposit base. That will change with the City National deal.

"If I can get a 4% spread and I can take that out of the 20 basis points I was getting in the securities portfolio, that's meaningful," Klock said.

How this deal differs from old RBC in U.S.

The purchase of City National will bring RBC back to the U.S. market less than four years after selling its previous American franchise to PNC Financial Services Group Inc. That sale came after RBC had acquired a series of banks in the Southeast during the most recent peak of the bank M&A market and required the company to book a $1 billion-plus write-down on the venture.

Analysts noted that City National is a different franchise, though, and focused on metro markets and high-net-worth clients opposed to operating in many rural markets with sizable exposure to local real estate.

Royal Bank President and CEO David McKay had also publicly stated as early as January 2013 that he wanted to go back to the U.S.

McKay, then RBC's group head of personal and commercial banking, said the bank was considering payment system partnerships and acquisitions, and expansion of its Internet bank in the U.S.

McKay said on a call to discuss the City National deal that he first approached the seller's chairman and CEO, Russell Goldsmith, about a transaction in 2013. McKay said that Goldsmith first told him that City National was not a seller, but ultimately that changed.

Analysts who cover City National were surprised by the timing of its sale, with many highlighting that the highly asset-sensitive company is selling before interest rates rise. BMO Capital Markets analyst Lana Chan was among the analysts in that camp, noting that City National is selling at below-normalized earnings given the low rate environment. However, she noted that the premium City National will receive in the deal "accounts for some of the earnings upside, in our view."

"CYN's sale price is well above acquisition multiples post-crisis, although there have not been many of this size; but, it is more in line with pre-crisis acquisition multiples. In 2014, the average deal price to TBV was 1.4x and the average core deposit premium was 5%; in 2006, the average multiples were 2.5x and 19%, respectively," Chan wrote in a Jan. 22 note to clients.

Big bank bigger picture

The deal represents the second-largest U.S. bank transaction since 2009, trailing only Capital One Financial Corp.'s $9.0 billion purchase of ING Bank, according to SNL data. The RBC/City National transaction is just the 13th U.S. bank deal with a value greater than $1.0 billion since 2009, but comes a few months after BB&T Corp. announced plans to acquire Susquehanna Bancshares Inc. for $2.5 billion. That deal prompted a number of observers to predict that big-bank M&A could return once again, and some analysts think the more recent RBC/City National transaction could serve as further proof that large deals can be done.

The Sterne Agee & Leach bank analyst team, for instance, noted that the $5.4 billion acquisition bodes well for midcap bank stocks in general, but specifically institutions with larger wealth management platforms and higher inside ownership.

The vast majority of bank stocks did rally higher Jan. 22.

The Sterne team also thinks that the City National is an encouraging sign for larger bank deal activity.

"With the news of the CYN sale we now have greater confidence in the prospects of larger size deals in the banking space," the analyst team wrote in a Jan. 22 report.

Print an SNL Financial reprint of this article

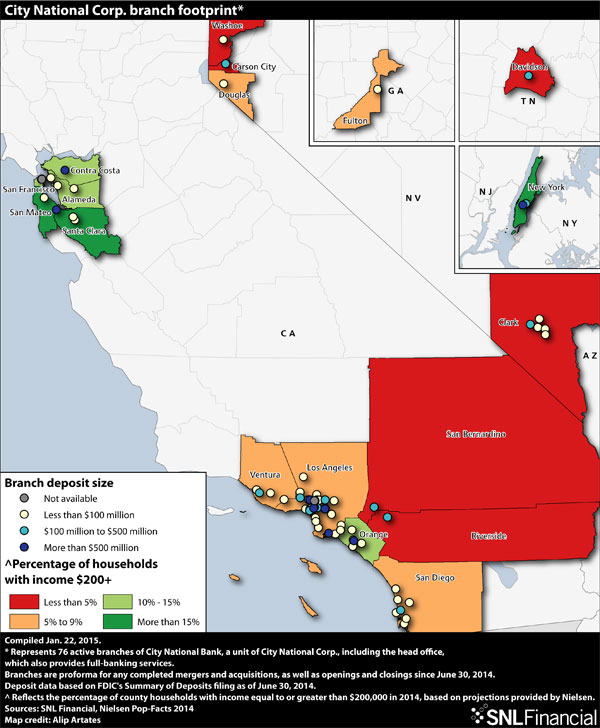

For a larger version of this map, click on the image

Tagged under Management, Financial Trends, Feature, Feature3, M&A,