Overdraft shift could cost smaller banks most

SNL Report: Expected CFPB changes could chew beyond community bank revenues

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Kiah Lau Haslett and Zuhaib Gull, SNL Financial staff writers

Potential changes to overdraft procedures and disclosures could erode fee income at the nation's banks and disproportionately impact smaller institutions where fees make up a greater percentage of revenue.

Banks and thrifts with less than $5 billion in assets showed the greatest reliance on overdraft fee income and could be hardest hit by any rule or guidance the Consumer Financial Protection Bureau publishes on the practice. The rules, slated for release later this year, are now expected to focus on disclosures or transaction ordering, as opposed to potentially harsher rules that would limit the amount of a charge or the number of times it could be incurred.

Putting some numbers on the issue

Beginning in the first quarter, banks with more than $1 billion in assets were required to report overdraft fees charged to consumers on transaction and nontransaction deposit products intended primarily for individuals. The 600-some banks that fit in that group collected $2.51 billion in overdraft fees.

Click to enlarge image

Click to enlarge image

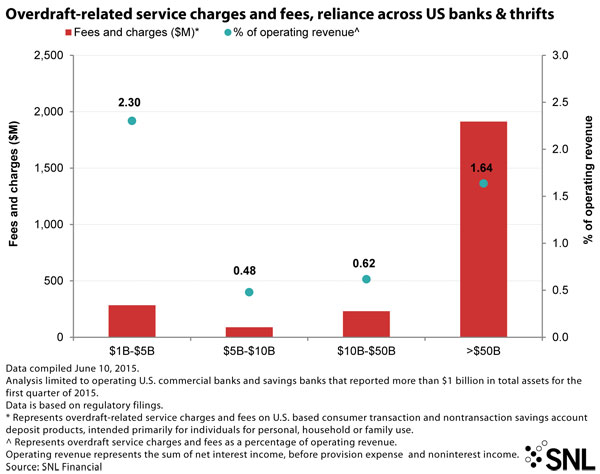

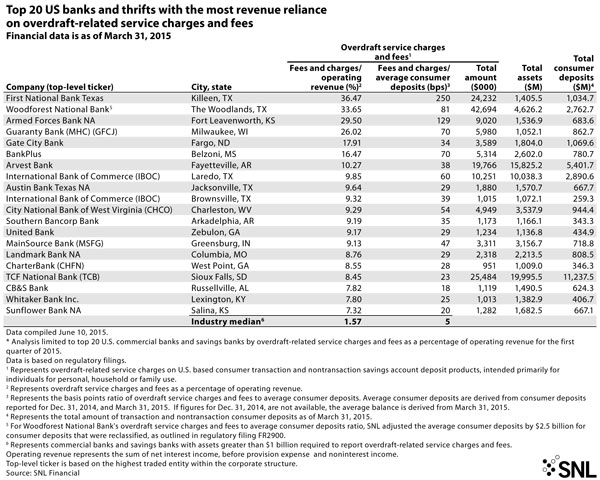

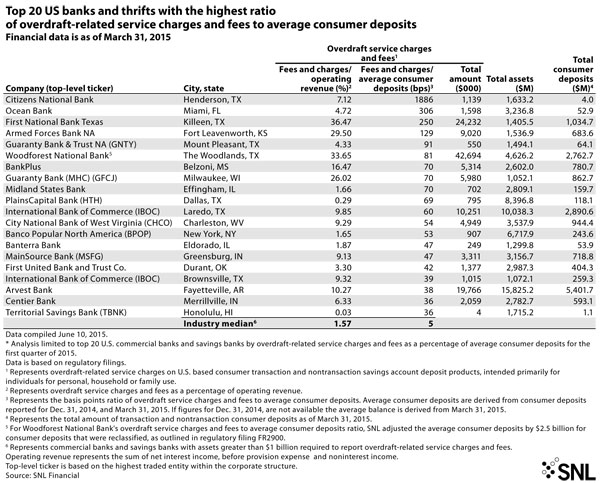

Overdraft service charges and fees comprised more than 2% of operating revenue at banks with less than $5 billion in assets, compared to 1.64% at $50 billion banks. Banks with less than $5 billion in assets also dominated SNL's analysis of institutions most reliant on overdraft fees: 17 of the top 20 banks had less than $5 billion in assets.

At Woodforest National Bank, a unit of The Woodlands, Texas-based Woodforest Financial Group Inc., overdraft service charges and fees were 81 basis points of average deposits, comprising 33.65% of operating revenue—the second-highest in SNL's analysis.

Julie Mayrant, president of retail operations, said the bank has four different overdraft products for most of its demand deposit accounts, including traditional overdraft protection that consumers must opt into and costs $29 per overdraft charge; a sweep product that links accounts and automatically transfers funds for a $2 fee; and two credit products. She said 50% of the bank's customers chose to opt into the overdraft program, a rate that fell as the industry changed from requiring customers to opt out of default overdraft protection to electing it.

Click to enlarge image

Click to enlarge image

She said Woodforest has been transparent with its customers when it comes to overdraft disclosures. The bank has used a terms and conditions form for new customer accounts that has been modeled after the Pew Charitable Trusts' form for several years because it is "simple, concise and very thorough," and has a separate disclosure specific to overdraft options, she said. But, she added, the ability for consumers to more easily access account information has actually had a more significant impact on overdraft behavior.

"From an industry standpoint, I don't think the disclosures necessarily changed customer behavior," she said. "I think the fact customers can access information easier today than ever before affects consumer behavior. I think the mobile channel has affected it, the adoption of smartphone technology — all of those things kind of work together in this space."

Where the bureau’s thinking may be headed

CFPB may be sensitive to the fact that small banks like Woodforest National Bank, which had $4.63 billion in assets at the end of the first quarter, would bear the brunt of any changes to overdraft fees or disclosures, and could propose changes that are softer than expected.

The agency is leaning toward opposing rules that would cap the fee size or frequency that they can be imposed, Bloomberg Businessweek reported June 5, citing two individuals briefed with the agency's process. Possible rules would instead be focused on prohibiting transaction reordering that maximizes potential overdrafts and better disclosures to help consumers avoid fees. The CFPB referred SNL to the FDIC's Financial Institutions Report issued Jan. 22 that discussed the call report changes.

Regulators want to make sure customers understand the services they receive, but the new data from call reports could influence rulemaking by quantifying the reliance that community banks have on overdraft fees, said Oliver Ireland, a regulatory attorney at Morrison Foerster. He said potential rules and regulations regarding posting order and enhancing disclosures seems like "a reasonable approach"

"I think [regulators are] concerned about the health of community banks," he said. "I think [community banks] may be—I'm going to qualify this—viewed as more customer-friendly than some of the larger banks. I think this will be a concern of the bureau."

Consumers have multiple roles in debate

Another concern the CFPB must weigh when it comes to potential changes to overdraft rules is that the product is popular with consumers who would rather pay a fee than bounce a check.

Regulators must balance the concern they have that a product harms consumers with the fact that some consumers have requested the product, said David Bizar, chair of Seyfarth Shaw LLP's Consumer Financial Services Litigation group.

Those concerns could be one reason behind the agency's narrow focus toward disclosures and reordering. Bizar said he "wouldn't be surprised" if the bureau banned the reordering of transactions or batch processing.

Larger institutions would also miss fee income

Small banks are not the only institutions where overdraft rule changes could eat away at revenue.

In an analysis of first-quarter call report data, Compass Point found that overdraft fees accounted for an elevated amount of EPS at TCF Financial Corp., International Bancshares Corp., Regions Financial Corp., Citizens Financial Group Inc., and SunTrust Banks Inc., according to a May 28 report.

The analysts said overdraft fees at TCF Financial accounted for more than 30% of EPS, or about 40 cents, when measured against his full-year 2016 estimates. If its overdraft revenue dropped to peer average, EPS would decline by 28 cents, the report said.

TCF unit TCF National Bank was also the largest bank on SNL's list of the 20 banks and thrifts that are most reliant on overdraft-related service charges and fees, with 8.45% of its operating revenue coming from overdraft fees. TCF management said they changed sort-order practices in 2013 but the bank has a high number of retail customers, which translates into more fees, according to comments made during the bank's third-quarter 2014 earnings call. TCF has more than a million checking accounts, an amount that Chairman and CEO William Cooper said was more common at a bank with $80 billion in assets as opposed to a $20 billion bank.

The large number in checking accounts persist even as management diversified revenues stream away from a reliance on consumer fees to national lending programs after the financial crisis, said R. Scott Siefers, an analyst at Sandler O'Neill.

"They have transformed and the first iterations of this began several years ago. But where are we?" he said. "They're still affected and depending on what and when the CFPB might come up with in terms of an industry mandate, there could be further changes down the road. … [I]t's an old issue but it's still relevant today, unfortunately."

Click to enlarge image

Click to enlarge image

Tagged under Mergers Acquisitions; Compliance; Revenue; CFPB; Big Data; Feature; Feature3;