Fintech and banks shaking hands

SNL Report: Digital lenders ditch disrupting traditional players to partner with them

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Zach Fox, SNL Financial staff writer

Marketplace lenders enjoyed explosive loan growth in 2015, but instead of cementing the industry as a disruptive threat to banking, the online companies turned toward partnering with retail banks, with more joint ventures expected in 2016.

Despite origination volumes that started to rival midsized banks, marketplace lenders in 2015 seemed to temper talk of taking over the banking industry. SNL spoke with senior management from five leading marketplace lenders and found widespread agreement that retail bank partnerships would become more common in 2016.

"When I went to marketplace lending conferences at the beginning of the year, there was a lot of talk about disrupting the banks. … More recently at conferences, there was a lot more talk about partnering with the existing players," said Julianna Balicka, an analyst with Keefe Bruyette & Woods. Balicka attributed the shift primarily to a need to reduce the cost of acquiring new consumers.

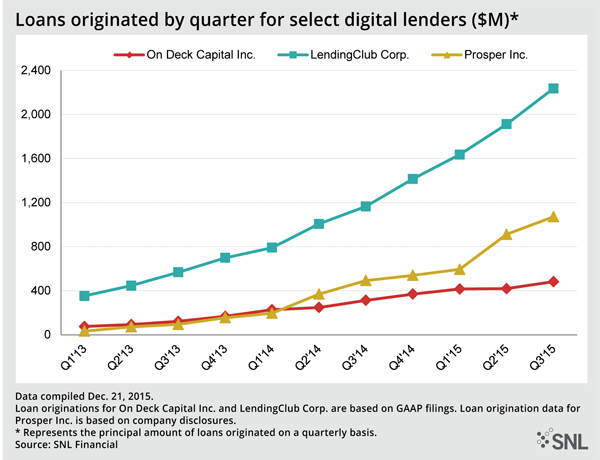

Looking at marketplace lenders’ numbers

LendingClub Corp. reported 92% year-over-year growth in loan originations in the third quarter while On Deck Capital Inc. posted a 54% growth rate. And the sheer volume of originations at the largest digital lenders started to rival some of their more traditional competitors. In the third quarter, OnDeck originated $483 million of loans, Prosper originated $1.07 billion and LendingClub did $2.24 billion. By comparison, Investors Bancorp Inc., a $20 billion thrift, originated $1.71 billion in the third quarter.

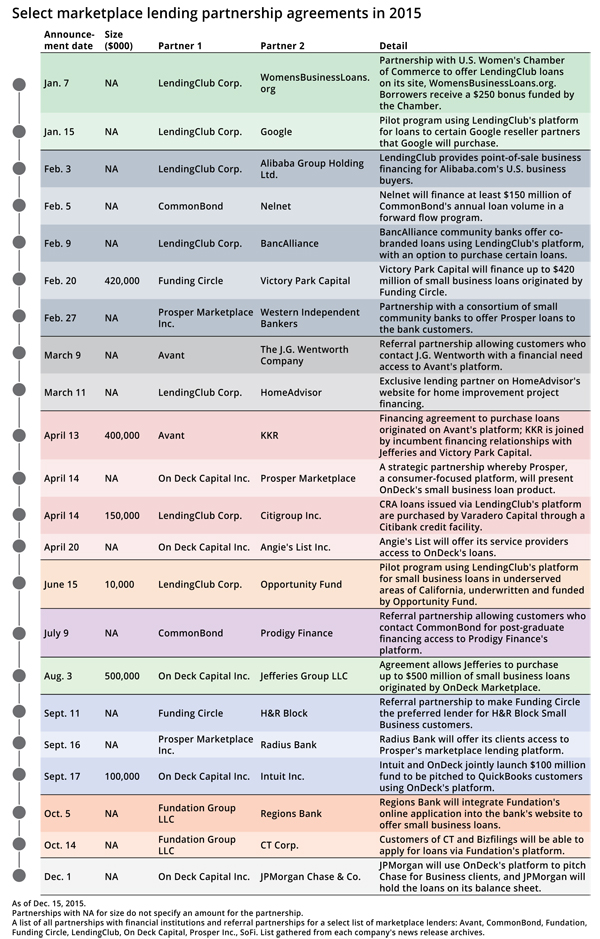

High loan growth rates are nothing new for marketplace lenders. What really caught Wall Street's eye was OnDeck's partnership with JPMorgan Chase & Co. The company's stock shot up 30% on the news as investors and analysts alike viewed the agreement as proof of concept.

Other top marketplace lenders, such as LendingClub, Fundation Group LLC and Prosper Marketplace Inc., also announced retail bank partnerships in 2015, and senior management at all of the lenders said they expect more to come next year.

"[The pipeline] is very robust. If anything, the Chase announcement has created a sense of urgency with some other banks," said Howard Katzenberg, CFO of OnDeck.

Banks have a variety of choices when choosing a marketplace partner. Companies such as LendingClub, Prosper, and Funding Circle deploy a business model often referred to as "pure marketplace," meaning the company does not hold any of the loans it originates. Companies such as OnDeck and Fundation use a hybrid model, holding some loans on balance sheet and sourcing the rest to investors like a pure marketplace lender would.

Unsurprisingly, each company believes its business model offers a competitive advantage.

LendingClub

The largest U.S. marketplace lender, LendingClub originated $5.78 billion of loans through three quarters in 2015, up 95% from the prior-year period. The company announced in February that it joined forces with BancAlliance, a consortium of 200 community banks, to offer co-branded loans. And in April, LendingClub announced a venture that would use a Citibank NA credit facility to finance loans that qualify under the Community Reinvestment Act, to be purchased by Varadero Capital LP.

Andrew Deringer, head of financial institutions for LendingClub, told SNL that the BancAlliance partnership will allow community banks to provide small-dollar loans that they would not have otherwise been able to offer due to high costs. The banks will also have an option to purchase the loans via LendingClub's platform.

While the BancAlliance consortium consists of 200 banks, each bank decides on its own whether to partner with LendingClub.

"We are growing the number of banks that we're working with every month," Deringer told SNL. "It's hard for me to gauge what the take-up is just because we have a pretty big pipeline. We're working with more than a dozen banks today just within that network."

LendingClub is also looking to partner with banks of greater size, including superregionals and larger, and expects to complete "a lot" of partnerships next year.

"You can safely assume that we're talking to a very large percentage of the banks that are over $50 billion, and so that will obviously include some of the money-center banks. It's too early to say anything," Deringer said.

He said LendingClub's pure marketplace model allows the company to achieve greater growth since it is not constrained by a balance sheet. Regarding the near-100% year-over-year growth rate in loan originations, Deringer said he thinks the company can sustain that level of growth into 2016, especially considering upcoming partnerships.

OnDeck

OnDeck's business model differs drastically from LendingClub, beyond the distinction between the pure marketplace and hybrid models. Where LendingClub has a broad product offering—from financing elective medical treatments to consumer loans to small business loans—OnDeck is singularly focused on small business loans.

CFO Katzenberg told SNL that the pipeline for bank partnerships is "very attractive" and that the JPMorgan deal puts OnDeck in a strong position since it serves as validation of the company's processes. The JPMorgan deal is different from a partnership OnDeck has with BBVA Compass Bancshares Inc., which co-brands the product, with OnDeck holding loans on its balance sheet.

Katzenberg said an important distinction is that JPMorgan defines the risk tolerance and relies on OnDeck for credit scoring and underwriting. "It takes a lot of resource[s] and time to build out a credit platform and a credit model, and I think that's a large part of why they're looking to partner with us, because we have the most mature and sophisticated credit capabilities in the space."

He said OnDeck wants to offer a product or a platform that aligns with the partner institution's goals. "With Chase, they wanted to be the lender and put their own capital at risk and be branded as a Chase solution, versus BBVA saw more opportunity by co-branding it and saying it's powered by OnDeck. In that situation, we're the originator and we own the loans, but that doesn't mean over time those relationships don't evolve."

Katzenberg said OnDeck's "maniacal" focus on small business loans is a differentiating factor and helps the company present itself as a market leader. With 28 million small businesses across the United States, OnDeck has plenty of room to grow considering it has only served roughly 45,000 small businesses so far, he said.

"We're very confident that we're still in the early innings of this game," Katzenberg said.

Fundation Group

Fundation Group LLC deploys a business model similar to OnDeck's, focusing only on small business loans and offering bank partners the option to either buy the loans or allow Fundation to hold the loans.

CEO Sam Graziano told SNL that the lender's partnership with Regions Bank, announced in October, involves a custom-built product that caters to the bank's client base. The joint venture includes a "highly negotiated agreement around asset sharing and revenue sharing" in which both Regions and Fundation will hold originated loans. Fundation is also developing a turnkey software platform for smaller community banks without the same level of customization, provided at a lower cost.

"We are perfectly happy to let the community banks hold loans, and we will be doing that. But we're also happy to own all of them," Graziano said.

He said the company relies on "a partnership-driven strategy" and expects another deal with a superregional bank by the end of next year. However, he said the marketplace lender is not in talks with money-center banks because that sort of partnership would consume significant resources.

"I'm more interested at the moment in developing a few, very meaningful, very intimate relationships as opposed to putting myself in a situation where I may only have one," Graziano said.

Prosper

Prosper Marketplace employs a pure marketplace model but, unlike LendingClub, offers only consumer loans. Prosper has posted significant loan growth and has publicly reported the figures, as opposed to other private marketplace lenders, such as Fundation, that have declined to disclose origination volumes.

Through the third quarter, Prosper originated $2.58 billion of loans in 2015, up 143.5% from first three quarters of 2014. President Ron Suber told SNL that he expects to again post 100% loan growth in 2016. The company expects to remain entirely focused on consumer loans; however, he added that consumers will often use the loans to fund their small businesses, expanding Prosper's reach beyond debt consolidation.

Suber said Prosper has developed processes to satisfy banks' compliance demands, adding that the company expects to announce "groundbreaking" announcements with retail banks in the first half of 2016.

"I think you'll see some big announcements from the, call it, No. 40 to No. 20 banks with marketplace lenders about real integrated ways to work together in partnerships. I think what you saw with JPMorgan and OnDeck is just a sign of what's to come," Suber said.

With significant loan origination volume, there has been some speculation that Prosper might join OnDeck and LendingClub with an initial public offering. While Suber said Prosper is larger than LendingClub was when it went public, there are no plans currently on the table to pursue an IPO.

"We have plenty of capital to run the business, and we'll see what happens in the year ahead. But we're very excited about what happened in 2015 and very, very excited about 2016," he said.

Funding Circle

Another marketplace lender expecting to make a splash in 2016 is Funding Circle, a pure marketplace lender that has so far focused its efforts in the United Kingdom. In September, the company made inroads into the U.S. market with a referral partnership with H&R Block Inc., winning the title of "preferred lender" for the tax giant's small business arm.

Albert Periu, Funding Circle's global co-head of capital markets, told SNL that the company expects to announce a "handful" of partnerships in the first quarter.

"Two years ago, there was a perception that we were trying to be competitive. It's not like that at all; it's very much a collaborative relationship," said Periu.

Similar to OnDeck and Fundation, Funding Circle is singularly focused on small business loans. In the United Kingdom, the bank already has partnerships with Santander UK Plc and Royal Bank of Scotland Group Plc.

Troubled waters ahead

Periu and the other executives repeatedly mentioned strong compliance being central to winning bank partnerships.

It seems likely that some marketplace lenders will hit rough patches. The list of major players to jump into the market can seem dizzying; other major companies in the space include SoFi, Zopa, Avant, CommonBond, LendKey, Lenda, Sindeo, Roostify, Lendvious, Orchard Platform, Foundation Capital, Dealstruck, Kabbage, LiftForward, and Kreditech.

Todd Baker, managing principal for Broadmoor Consulting LLC, has been a vocal critic of the burgeoning marketplace lending industry, pointing to the often fragile funding sources. He said the bank-digital lender partnerships appear positive for the banks but could relegate marketplace lenders by stripping their technological advantages.

"As these things develop, it'll be a very interesting question whether it pushes these companies toward becoming service providers for the banks as opposed to free-standing competitors," Baker told SNL.

For marketplace lenders with ambitions of becoming lenders of the future, navigating the credit cycle will be a top priority. Fundation's Graziano said competition for the loans has become fierce, and he has seen fellow marketplace lenders bid on loans with extreme aggression.

"For a given credit," he said, "some of these competitors will go many hundreds of basis points lower than we will."

Zuhaib Gull contributed to this article.

This article originally appeared on SNL Financial’s website under the title, "Digital lenders ditch disrupting banks to partner with them"

Download PDF reprint of SNL article

For additional viewpoints on fintech and banking partnerships:

• “Stock analysts size up fintech”

• “Shake hands—and come out cooperating”

• “Community banks, alternative lenders can coexist”

Tagged under Mergers Acquisitions; Financial Trends;