The New Killer KPI for Personal Digital Banking: Moment-of-Need to Resolution

Few realize it, but a new era of community banking is here

- |

- Written by Lee Wetherington, Director of Strategic Insight: Jack Henry & Associates, Inc.

Banks once defined by their personal service inside branches can now (for the first time) translate their personal service meaningfully into digital channels thanks to new technology that enables immediate, authenticated, actionable conversations inside digital banking.

Since the introduction of the ATM, technology in banking has been applied generally to replace people with automation in the name of self-service, but a new approach among community financial institutions finally employs technology to give consumers what they want at the moment of need: a live, local person who can resolve their questions and concerns at the first point of contact without being forced to dial into a call center, re-authenticate identity, remember the account number in question, and verbally describe the details of the problem from scratch.

For community financial institutions, this new approach restores their relationship-based banking model and extends it into digital channels. A big deal.

Better still, by eliminating the need to re-authenticate in separate channels, this new approach can reduce call volumes by 20% without adding support staff.

The Financial “Moment of Need”

Roughly 75% of Americans say they live “paycheck-to-paycheck.” For them, there is no such thing as a “small money problem.” One unfamiliar transaction or one unexpectedly low balance can feel like a disaster in the making. In this context, consumers don’t want to navigate the convoluted menus of an Interactive Voice Response (IVR) system or, heaven forbid, spar with a soulless chatbot that can’t understand, much less intuit, what the consumer needs.

In a financial moment of need, consumers prefer personal service. And this is true across all ages and incomes.

In the golden era of analog banking, high-quality, in-person branch service was always preceded by the inconvenience of the time required to get to the branch—since all moments of need happen outside the branch.

Today, however, waiting in line at a branch, cursing at chatbots, and screaming “RE-PRE-SEN-TA-TIVE!” at IVRs are no longer necessary pre-requisites to proper service and resolution. Instead, customers can get what they want (access to real people) when they need it most while perusing balances and transaction details inside digital banking, where most moments of need arise.

Even better, for most community financial institutions, these new digital conversations are being fielded on-demand by the very same people staffing the branches.

To this end, branch strategy and digital strategy are no longer mutually exclusive; they’re directly linked in one fluid customer experience.

The Mundane vs. the Meaningful

There is a distinct difference between personal and “personalization.” “Personal” happens when a real person connects with another real person. “Personalization,” however, refers to automated, data-analytics applications that provide customized information to customers serving themselves inside digital channels (e.g., real-time alerts, offers and spending-pattern advice).

Though personalization is helpful for mundane interactions, it cannot substitute for the personal connection required to deliver meaningful service and support at the moment of need.

Mega banks prioritize automation and self-service by default. They often provide personal support only as a last resort after customers have been forced to exhaust the gauntlet of all other self-service options.

In a recent Forbes article on the ethics of fintech, Ron Shevlin posed several sobering questions about the price of automation in banking. Does too much automation ultimately disable ethics and cut against the best interests of customers? Perhaps the bigger question is, what kind of opportunity does the over-automation of banking present to small banks and credit unions?

Unlike mega banks, community financial institutions prioritize the personal. Delivering personal service at the moment of need in digital channels may prove to be smaller institutions’ most important and strategic differentiator going forward.

Digital Banking KPIs

Digital key performance indicators (KPIs) have been around for a while. Today, they include time-based benchmarks that measure the speed of:

- App-launch to app-usable (time required);

- App-launch to balance view (time required); and

- App-launch to transaction view (time required).

Surprisingly, these table-stakes KPIs remain sluggish in digital banking. Some of the most widely used mobile banking apps still clock shockingly slow launches of 7-11 seconds. The fastest mobile banking apps open in 1-2 seconds.

In a moment of need, the difference between 1 second and 10 seconds is an eternity. For fun, check your mobile banking app’s launch-to-usable speed right now.

The New Killer KPI: Moment-of-Need to Resolution (MON2RES)

The new era of truly personal digital banking brings with it a new killer KPI that rules and subsumes all others: the time that elapses between the moment of need and the moment of resolution (MON2RES).

Think about it. What was the best MON2RES in the golden age of branch banking – 30 minutes, 1 hour? It really depends on how close you were (are) to the branch and whether/when you can free up your schedule to go. It might also depend on when you call, who’s available, and how long you must remain on hold or await a call back.

What is the best MON2RES today for mega banks that force customers to exhaust the limits of self-service systems, like IVRs and chatbots, before reluctantly revealing options for personal service – 5 minutes, 15 minutes? Let’s table the customer rage and gnashing of teeth that result from the bad UX for now.

The bottom line is that community financial institutions can now deliver MON2RES on-demand. This is not only historic, but it’s also strategically critical. And for serving small business relationships, it’s a gamechanger.

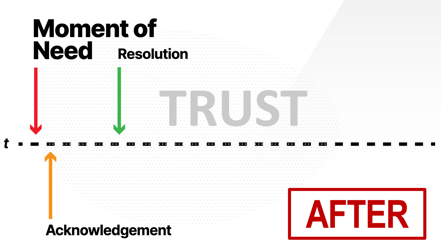

How Trust Turbo-Charges the Speed of MON2RES

Community financial institutions have always had a secret weapon: trust. It’s the bedrock of relationship banking, and it’s an advantage that community financial institutions can now lever digitally in a measurable and powerful way.

After the customer has alerted the bank to a moment of need—and before that need is resolved—there must be an acknowledgment of the need.

For trusted institutions, acknowledgment is a de facto resolution psychologically speaking. This means that in addition to the new technology that dramatically shortens MON2RES technically, the presence of trust creates a digital UX that effectively delivers resolution in real-time.

This is the way forward for community financial institutions in the era of mega banks, big techs, and fintechs. This is the answer to automation for the sake of automation. And this is how community financial institutions safeguard themselves and the communities they anchor.

Tagged under Community Banking, Technology, Retail Banking, Tech Management, Branch Technology/ATMs, Feature3, Feature,