Report of BHC insurance brokerage fee income

A few stumbled, but most holding companies grew their insurance business in 2012

- |

- Written by Michael D. White

Six hundred sixty-five (665) large, top-tier bank holding companies (BHCs) earned $6.20 billion in insurance brokerage fee income in 2012,1 constituting a 19.5% decrease from $7.70 billion in 2011, according to the Michael White Bank Insurance Fee Income Report published by Michael White Associates (MWA).

Insurance brokerage income consists of commissions and fees earned by a BHC or its subsidiary from insurance product sales and referrals of credit, life, health, property, casualty, and title insurance. It does not include income derived from the sale of annuities or non-insurance products like debt cancellation or debt suspension agreements.

While several other big BHCs saw their insurance brokerage income decrease, this industry drop was attributable largely to two BHCs, whose declines in insurance brokerage income exceeded $1.54 billion. They were Bank of America Corporation (NC) and Citigroup, Inc. (NY).

B of A subsidiary FIA Card Services lost more than three-quarters of a billion dollars in insurance brokerage income, and net insurance brokerage losses tallied $637.5 million in 2012. The cause of this decline, which first occurred in 2010, was due to inappropriate sales of payment protection insurance (PPI) policies through its international card services business in the United Kingdom. The U.K. Financial Services Authority (FSA) established new standards for PPI sales and required companies to "remediate" customers for systematic breaches of the standards before, as well as after, they were set. B of A's PPI reserve was $510 million on December 31, 2012, and its recorded PPI expense last year was $692 million. From January 2011 through January 2013, total industry refunds and consumer compensation had reached $13.55 billion, according to the FSA.

BHCs with assets greater than $10 billion experienced a 24.0% decrease in insurance brokerage fee income from $6.96 billion in 2011 to $5.29 billion in 2012. Despite declines at several of the largest BHCs, the rest of the industry performed well overall.

BHCs with assets between $1 billion and $10 billion in assets did very well in 2012, earning $686.1 million in insurance brokerage fee income, up 13.4% from $606.6 million in 2011.

Insurance brokerage fee income produced by BHCs between $500 million and $1 billion in assets increased 65.9% from $133.7 million in 2011 to $221.9 million in 2012, largely due to new reporting by one thrift holding company. Without that one company, this class of financial institutions grew its insurance revenue by 8.1%.

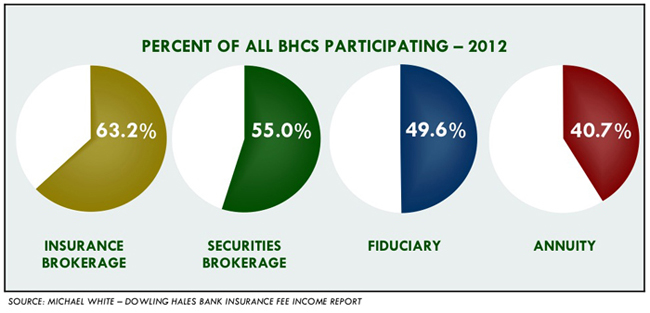

In 2012, as in every year, insurance brokerage attained the highest rate of participation by BHCs, outdistancing the number of BHCs engaged in annuity, fiduciary, or securities brokerage activities. [GRAPHIC-1] Three in five (63.2%) large BHCs reported participating in insurance sales activities.

GRAPHIC-1

Historic bank insurance industry growth

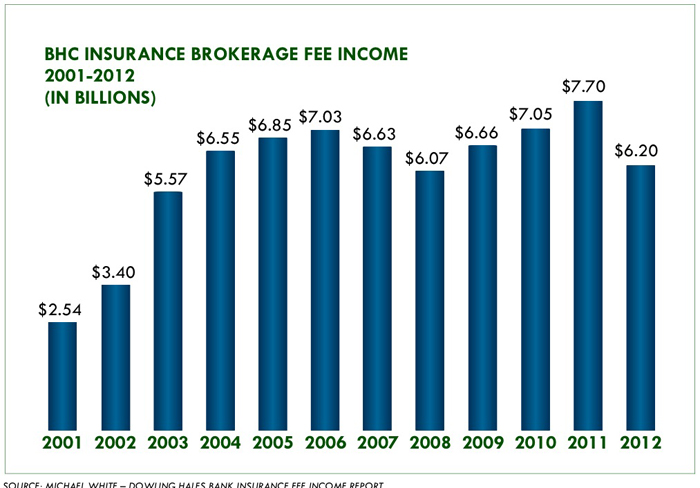

Annual bank holding company insurance brokerage fee income rose from $2.54 billion in 2001, when we were first able to measure it, to $6.20 billion in 2012. [GRAPHIC-2]

GRAPHIC-2

Nationally, bank holding company insurance brokerage revenue grew at a compound annual rate of 8.44% from 2001 through 2012, slowing from the compound annual growth rate (CAGR) of 13.1% achieved for the period 2001 through 2008.

From 2008 to 2012, the industry grew annually by 0.8%, due to the two declines of aggregate insurance brokerage income in 2008 and 2012, which, along with the slower CAGR of 8.3% among BHCs with assets between $1 billion and $10 billion since 2001, caused this lower CAGR for the industry. BHCs with assets over $10 billion grew 8.76% annually since 2001, while BHCs with assets between $500 million and $1 billion grew at a compound annual rate of 13.1% from 2001 to 2012.

Despite the slowing of growth in insurance brokerage income in 2008 and 2012, BHCs have attained a strong position in insurance brokerage revenue since 2001, one that enables them to prepare for future growth as the market hardens and the general economy and acquisition market improve.

Recent years

Through 2005, the year after the onset of the seemingly unending soft property-casualty market, bank insurance brokerage income had been growing at phenomenal rates. (The soft market is one where premiums decline as insurance underwriters compete to gain or preserve market share.) Of course, much of the early growth was due to continued acquisition activity, which peaked in 2003, subsided, bumped up in 2006, subsided again, and in 2012 began to bubble up again. Since December 2011, market premiums began rising consistently, although no one yet wishes to declare the new environment a hard market.

Despite the longstanding soft market in commercial property-casualty insurance in the period 2004-2011, BHCs achieved record insurance brokerage income in 2011. Still, the bank insurance industry has been up against it, as they say, over the last few years, as:

(1) The industry's numbers suffered from these occasional major decreases in insurance brokerage revenue at a huge banking organization, such as occurred at Bank of America in 2010 and 2012.

(2) There were more frequent instances of decreases in contingent commissions.

(3) The complete removal, starting in 2007, of annuity commissions from the insurance brokerage income data field. Combining annuity commissions with insurance brokerage income, as used to be done, would significantly increase the total insurance-product revenue for banking organizations to over $8.66 billion in 2007, to a high of $10.54 billion in 2011, and to $9.35 billion in 2012.

(4) Certain large bank holding companies exited the property-casualty insurance brokerage business by selling agencies or business lines. These have included Bank of America Corporation (NC), BNCCORP, Inc. (ND), Capital One (VA), Citizens Financial Group, Inc. (RI), Commerce Bancorp (NJ), First Horizon National Corp. (TN), Fifth Third Bancorp (OH), PNC’s National City agencies (PA), and Webster Financial Corp. (CT). At the time of their divestiture, these agencies represented a loss to the banking industry of $391 million in insurance brokerage income. Those agency sales related quite specifically to each financial institution’s particular circumstances, strategic aims, or degree of commitment to insurance.

What the future holds

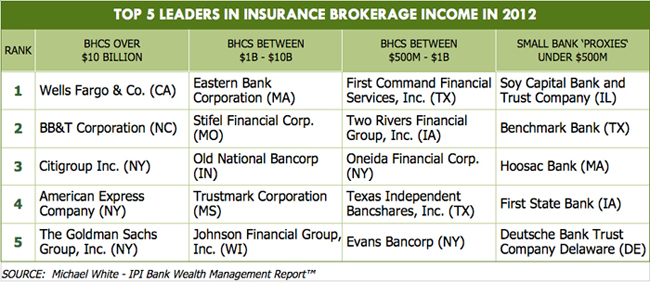

Considering the removal of these fairly significant chunks of insurance-related income from the industry total, the bank industry's revenue from insurance brokerage actually looks even better than it is. We can see that the sales of some large bank insurance units to nonbanks do not represent a trend. So far, the sales of bank-owned agencies have largely been conducted either because a bank needed capital or insurance was unable to become a relevant or meaningful proportion of income. Truth be told, in the last few years, many more banks and thrifts acquired agencies than sold them. Since 2007, dozens of banks have acquired agencies; in fact, quite a number have purchased multiple agencies. [GRAPHIC-3]

GRAPHIC-3

MWA also saw real progress in the expansion of insurance programs in 2012 that earned a minimum of $1 million. In our research, we examined 160 BHCs in 2012 and 154 BHCs in 2011 that generated $1 million or more in insurance brokerage income. At the end of 2012, 116 of these BHCs (72.5% of total) showed positive growth in their insurance income, up 33.3% from 87 BHCs (56.5% of total) with positive growth at the end of 2011. The number of BHCs with double-digit increases in insurance brokerage rose 75.8% from 33 in 2011 to 58 in 2012.

BHCs with declines in their insurance brokerage income numbered 42 (26.3% of total) in 2012, down 37.3% from 67 (43.5% of total) in 2011. The number of BHCs with double-digit declines in insurance brokerage fell by 39.3% from 28 in 2011 to 17 in 2012. These changes signal improvement among BHC insurance agencies. At a time when revenues from other bank activities such as lending and deposit account service charges are down, insurance brokerage stands out as a natural business for banks and useful addition to the income statement.

Relevance in bank insurance brokerage

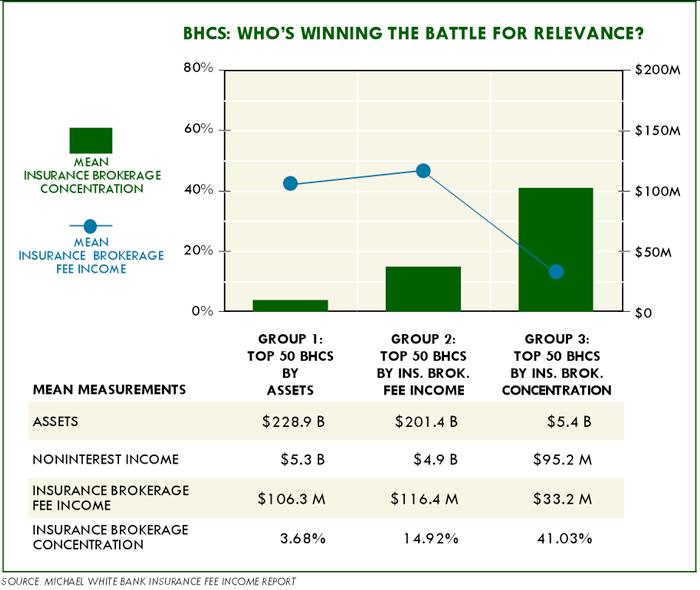

So, who’s winning the battle for relevance or significance in bank insurance brokerage? That’s an important thing to keep in mind, and this illustration serves as a powerful reminder. An important measure of relevance or significance is the Insurance Program Concentration Ratio, which is the percentage of total noninterest income attributable to insurance fee income. This ratio enables us to know how concentrated or meaningful bank insurance programs are among their BHCs’ nonlending activities. [GRAPHIC-4]

GRAPHIC-4

In 2012, the top 50 BHCs by Assets (Group 1) averaged $228.9 billion in assets and $106.3 million in insurance brokerage fee income. Their mean Insurance Program Concentration Ratio, that is, the percentage of noninterest income derived from insurance brokerage, was 3.68%.

With an average asset size of $201.4 billion in assets, the top 50 BHCs by Insurance Brokerage Fee Income (Group 2) averaged $116.4 million in insurance brokerage income. They generated an average Insurance Program Concentration Ratio of 14.92%.

Group 3 consists of the top 50 BHCs by Insurance Program Concentration. They averaged only $5.4 billion in assets, but generated on average $33.2 million in insurance brokerage income and averaged an Insurance Program Concentration Ratio of 41.03%.

This exercise demonstrates that Assets and Insurance Program Concentration are inversely correlated. The largest banks may have generated a greater volume of insurance brokerage income, but its relevance or significance to them was the lowest among the three groups because the largest banks’ ratio of insurance brokerage income to noninterest income was the lowest. Part of the reason for this is that large BHCs have more resources to engage more sources of noninterest income.

There are, of course, individual exceptions among the large banking organizations; a couple that come to mind are BancorpSouth Inc. (MS) and BB&T Corporation (NC), where Program Concentration Ratios are regularly more than 30%. BancorpSouth and BB&T have more resources to undertake other revenue-making activities, but that does not prevent them from recognizing the opportunities of insurance distribution and taking advantage of them.

And, yet, relevance is relative. While Program Concentration can be greater as a quantitative measurement among smaller institutions, smaller measures of Concentration can still be relevant to larger institutions that obtain noninterest fee income from more numerous sources. Few would dispute the relevance or significance of $1.56 billion in insurance brokerage fee income at Wells Fargo, even though its “relevance reading” is 3.67%.

Most community banks can achieve relevant scale with $1 million to $5 million in insurance commissions and even less, depending on their asset-size. Indeed, last year, the mean Program Concentration of the top 50 BHC leaders in Program Concentration exceeded the mean value of Concentration among all BHCs by a factor of 6.0, and among the top 50 bank leaders in that measure by 14.5 times.

Among the top 50 BHCs in insurance brokerage income as a percent of noninterest income, the mean Concentration Ratio in 2012 was 35.87%. Among the top 50 banks in Insurance Brokerage Concentration, the mean was 73.94% of noninterest income. Relevance is high for those who strive to be relevant.

Positive contribution of bank insurance brokerage

As we can see, insurance activities are a meaningful source of income for a large number of banks and BHCs. It is perhaps a simple truism, even a tautology: banks strongly committed to insurance fare better at it. Even the smallest community banks can have great success in insurance brokerage activities. We might even say, especially the smallest community banks can have great success in insurance brokerage activities.

Unfortunately, too many banking organizations have not gotten serious about insurance brokerage. Community banks with high Tier 1 and total risk-based capital ratios continue to earn sub-par returns and ignore the opportunities in other financial services like insurance and investment programs. Too many banks and BHCs have not gotten serious about insurance brokerage income and have not devoted meaningful attention, capital, marketing and sales efforts to develop it. This is true of many institutions already reporting small sums of insurance brokerage revenue. And, that's not to mention more than half the banks and better than one-third of the large BHCs that are not engaged at all in the activity.

Insurance brokerage is one of the least risky, steady, profitable, publicly needed financial services there is. The return on investment can be good, with the application of sound criteria in selecting acquisition targets. And, in many cases, the returns from an insurance agency will exceed the ROE of a bank.

We hold onto the hope that more banking organizations will recognize their customers’ widespread insurance needs, society’s prevalent use of insurance products for protection against harm, and the positive impact that insurance fee income can have on the financials and the future of their institutions.

ENDNOTES

1 In 2006, the Federal Reserve redefined top-tier “large” BHCs as those with more than $500 million in consolidated assets. With few exceptions, only those BHCs defined as “large” report detailed revenue line items like insurance brokerage income. Hence, this report uses the smallest community banks, i.e., those with assets under $500 million, and their insurance brokerage fee income as a “proxies” for the smallest BHCs.

Michael White, Ph.D., CLU, ChFC is president of Michael White Associates, a bank insurance consulting firm headquartered in Radnor, PA, and at www.BankInsurance.com. He may be reached at 610-254-0440 or [email protected].

Tagged under Retail Banking, Revenue,