Loss-share headaches not ending soon

SNL Report: And the clock keeps running…

- |

- Written by SNL Financial

Loss-sharing deals struck with FDIC have proven a challenging deal for the agency’s partner banks.

Loss-sharing deals struck with FDIC have proven a challenging deal for the agency’s partner banks.

By Marshall Schraibman and Nathan Stovall, SNL Financial staff writers

Many banks have had their issues with FDIC loss-share agreements, and those concerns likely will not disappear after the agreements expire.

Banks still hold billions of dollars in assets covered under loss-share agreements and need to work hard to squeeze out the value of the assets before the agreements expire.

For a larger version, click on the image.

For a larger version, click on the image.

Earliest commercial deals approach expiration

Loss-share agreements for single-family assets last 10 years, while loss-sharing for commercial assets last five years. The latter means that there are fewer than 12 months remaining for the earliest commercial loss-share agreements tied to failed-bank deals.

When the agreements expire, banks will still have to manage the assets tied to the agreements in accordance with the terms FDIC laid out in the contracts. That means that banks likely will not be able to purge those assets through bulk sales after loss-sharing ends.

Bankers had hoped that they could purge their balance sheets after the fourth anniversary of commercial loss-share agreements was reached. The agreements included a provision that allowed banks to sell shared-loss assets in bulk, subject to FDIC approval.

However, advisers say that no bulk sales of covered assets have occurred, because the agency has no incentive to permit transactions that would result in substantial losses. FDIC spokesman David Barr confirmed that no real bulk sales of covered assets have occurred.

Barr also said that the provisions that are in place for assets covered under loss-share agreements will remain in place even after the agreements expire. That likely will keep bulk sales from occurring then.

Performance of loss-share assets flags

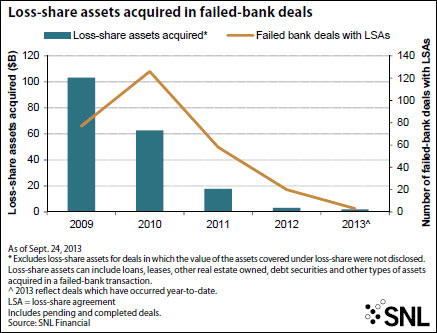

It is difficult to assess just how many assets will no longer be covered under loss-share soon, because banks and the FDIC do not provide updated values of covered assets with the related date of their loss-share agreement. As of June 30, FDIC had entered into 302 loss-share agreements with banks on initial asset balances totaling $214.8 billion. The amount of assets covered under loss-share stood at $91.3 billion at the end of the second quarter.

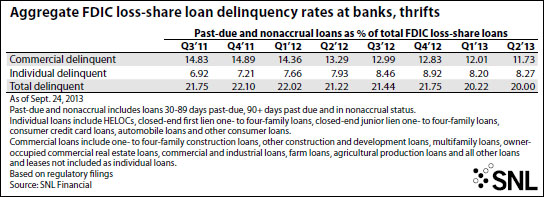

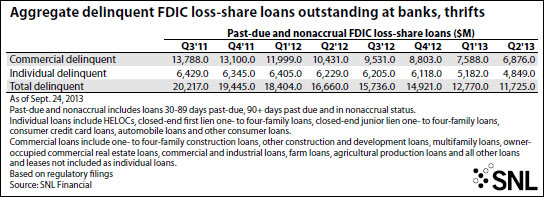

Many of those assets continue to experience elevated levels of delinquencies. The banking industry disclosed that $11.73 billion of loans covered under loss-share were delinquent at end of the second quarter, or 20.0% of all loss-share loans. Banks disclosed that $6.88 billion in commercial loans covered under loss-share were delinquent at the end of the second quarter, or 11.73% of commercial loans covered under loss-share.

Real estate values have risen in some of the most heavily hit markets like Georgia and Florida, but banks looking to foreclose on properties in some states with judicial review have faced a long and arduous process of working through those assets.

In Florida, for instance, foreclosing on some assets took almost 1,000 days at the peak of foreclosure filings, advisers say. The timeline has since improved and real estate prices have rebounded from the depths of the credit crisis.

If the real estate recovery allows banks that entered into loss-share agreements to record recoveries on covered assets, the institutions will have to share any recoveries on the assets with FDIC for three years after the commercial loss-share agreements expire. Banks will split the recoveries with FDIC by the same percentages they agreed to in the original loss-share agreement.

At the point of expiration, banks will also have to write down the receivable that accounts for the value of loss-sharing—deemed an indemnification asset—to zero, assuming banks have not squeezed out all the value of the agreement when taking losses on the management of covered assets. Randy Dennis, president of DD&F Consulting, which has assisted banks on many failed-bank deals, said banks seem confident they will have realized most of the value of their loss-share agreement before it expires.

For a larger version, click on the image.

For a larger version, click on the image.

For a larger version, click on the image.

For a larger version, click on the image.

"Most of the banks I talk to feel pretty good that they have recognized the losses and the market is turning around. They're breathing a sigh of relief. They don't think their indemnification asset is going to bite them. But we are actually seeing some recoveries," Dennis said. "Most banks seem to be fairly comfortable with where they are in the life cycle of their loss-share."

Accounting for loss-sharing is a bear

Some banks already recorded impairments related to their loss-share agreements last year. The FASB forced some hands last October, clarifying that receivables had to match the length of loss-share agreements. A few institutions reacted to the clarification and recorded impairments, proving that they had run schedules that did not match the length of their loss-share agreements.

The accounting for loss-sharing has been the bane of many bankers' existence, but loss-sharing clearly helped FDIC market failed banks and raised the offers that acquirers made when bidding on failed institutions. FDIC estimates that loss-share has saved in excess of $41.1 billion, compared to an outright cash sale of those assets.

Many bankers on the conference circuit bemoan having participated in loss-share deals, given the complex accounting, limitations on managing assets and substantial infrastructure and cost required to accurately report on the pools under loss share. Bankers now look at loss-sharing quite differently at this point in the cycle, and most institutions are no longer including loss-sharing when bidding on failed banks.

Several advisers that SNL spoke with noted that acquiring an institution without loss-share at this point in the cycle is just less expensive because it does not require the substantial infrastructure required to manage loss-sharing. Since 2012, loss-share agreements have been attached to just 33.9% of failed-bank deals, compared to 73.9% between 2009 and 2012, according to SNL data.

FDIC mulls changes to handling loss-sharing

Advisers say FDIC has discussed terminating loss-share agreements on small pools of covered assets—often as little as $20 million—to reduce the expense of managing loss-share for both parties. However, few of those deals have occurred because the agency and banks disagree over what value is left in the contract.

Advisers say FDIC has resumed discussions with banks that still have small amounts of covered assets under loss share. Barr said that both the FDIC and the institution has to agree voluntarily to end the loss-share agreement and the idea came after receiving feedback from smaller acquirers who contacted the agency after dealing with the detailed reporting requirements associated with loss-sharing.

"Once we got that feedback we did start contacting some other acquirers on our own. We took a more proactive approach," Barr said.

Many smaller banks will likely continue to work through the assets until the agreements expire rather than trying to exit the agreement due to discrepancies over the value of loss-sharing. Banks with larger agreements just might need to work hard before the agreement expires to remove uncertainty of what the future could hold as they operate with the restrictions of loss-share agreements but without the protection of loss-sharing itself.

Tagged under Management, Financial Trends,

Related items

- How Banks Can Unlock Their Full Potential

- JP Morgan Drops Almost 5% After Disappointing Wall Street

- Banks Compromise NetZero Goals with Livestock Financing

- OakNorth’s Pre-Tax Profits Increase by 23% While Expanding Its Offering to The US

- Unlocking Digital Excellence: Lessons for Banking from eCommerce Titans