Reserves for commercial loans rise

SNL Report: Higher business credit risks in the picture?

- |

- Written by SNL Financial

By Tahir Ali and Zach Fox, SNL Financial staff writers

Loan loss reserves shrank yet again, overall, during the second quarter, but reserves for commercial loans increased, in what appears to be a trend.

With competition for commercial and investment loans heating up, the increase in reserves could represent a move deeper into the risk pool, though an increase in loan volume has accompanied the higher reserves. That means reserves for commercial loans as a portion of outstanding loans have been relatively flat.

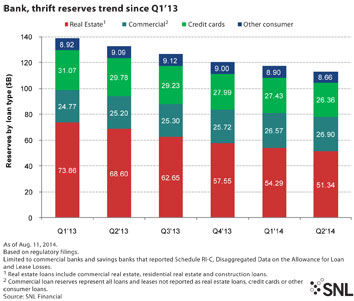

Reserves rise, but loans do too

Since the first quarter of 2013, reserves for commercial loans have increased each quarter, while overall reserves steadily declined for all commercial banks and savings banks. (See related article: "Overall credit buffers turn down.") In the second quarter, reserves for commercial loans totaled $26.90 billion, up from $26.57 billion in the first quarter and $25.20 billion in the 2013 second quarter.

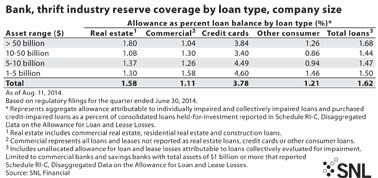

For the second quarter, reserve coverage for commercial loans represented 1.11% of all loans among commercial banks and savings banks with total assets of $1 billion or more. Even though aggregate reserves for commercial loans have been increasing, loan growth has more than matched that growth. The coverage ratio for commercial loans was actually down slightly relative to the year-ago quarter.

Reserves by lending sector

Reserves for real estate loans, which includes commercial and residential real estate as well as construction loans, have fallen dramatically over the past year, helping guide down aggregate reserves across loan types.

For the second quarter, reserves for real estate loans totaled $51.34 billion, down from $54.29 billion in the first quarter and $68.60 billion in the year-ago quarter.

For a larger version, click on the image.

For a larger version, click on the image.

Overall, total reserves for commercial and savings banks came to $114.95 billion in the second quarter, down from $118.84 billion in the first quarter and $134.59 billion in the second quarter of 2013. Those figures include unallocated reserves, as opposed to the bar graph above, which shows only reserves that have been allocated for real estate, commercial, credit cards, or other consumer loans.

Unallocated reserves are typically much smaller than any single category; for the second quarter, unallocated reserves totaled $1.70 billion.

For a larger version, click on the image.

For a larger version, click on the image.

The decline in aggregate reserves across loan types while they rise for commercial loans fits a general theme of increased competition in the sector, said Steven Reider, president of Bancography, a bank consulting firm. Hot competition for loans has forced some banks to go a little riskier than they would have previously, he said.

"I can't tell you how many clients we've come across who have told us that the goal, in commercial lending, is really to do much more [commercial and industrial] and much more [commercial real estate]," Reider told SNL.

First Republic Bank’s major add to provision

That narrative also seems to apply to First Republic Bank, which saw a massive increase in its second-quarter loan loss provisioning.

The company's loan loss provision increased to $21.80 million in the second quarter from $7.10 million in the first quarter. That pushed up the bank's aggregate loan loss reserves to $181.31 million in the second quarter, compared to $159.64 million in the first quarter and $148.31 million in the prior-year period.

The jump in loan loss provisioning attracted several questions during the company's July 16 conference call discussing second-quarter results. Management had said in prepared remarks that the bank would target a reserve allocation of 55 basis points to 60 basis points.

Ken Zerbe, an analyst with Morgan Stanley, asked whether the leap in provisioning was driven by more commercial and investment loans, which typically require higher reserve allocations.

"Ken, I think you're on the right direction," Michael Roffler, First Republic Bank deputy CFO, said in response, according to a transcript of the call.

"Obviously,” continued Roffler, “the business lending does come into the process at higher than the 55 basis points to 60 basis points, compared to the home loan, which is much less than that. So given the increase in utilization that occurred in business lines, and it did help increase the outstanding during the quarter, that led to higher provision levels given that little bit of change in mix that occurred compared to what you may have seen in prior periods."

For a larger version, click on the image.

For a larger version, click on the image.

Tagged under Management, Financial Trends, Risk Management, Credit Risk,