Connecting ALCO dots

Is your asset-liability committee talking about the right things?

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Keith Reagan, managing director, Darling Consulting Group

Since December of 2008, there have been countless statements by Federal Reserve officials trying to provide guidance and transparency on future policy actions. Despite these efforts, multiple times in the last seven years, the market “knew” rates were going to increase—yet they have not.

Again, at the September meeting Fed funds remained between 0% and 0.25%. Nonetheless, Fed comments and market sentiment continue to suggest that tightening may occur in 2015.

In the immortal words of the late great Yogi Berra, “Is it déjà vu all over again”?

Was the decision to hold rates a temporary pit stop on the road to higher rates? Or are we going to be at these levels going forward?

Either way, your ALCO should fully understand the impact of rising, falling, and current rates on not only interest rate risk, but also on liquidity, how the two inter-relate and the impact on earnings/capital.

Strategic focus at ALCO

Liquidity management should be the linchpin to strategic action at every ALCO meeting.

• How much liquidity do you have today?

• How much liquidity do you need?

These are two very different questions.

Knowing how much liquidity you have (regardless of the calculation you use) isn’t nearly as important as knowing how much you need? And you must weigh the latter in terms of today, this month, this quarter, and beyond.

Will there be loan growth requiring additional funds? Will there be deposit fluctuations that need to be supplemented?

A forward-looking, cashflow-based liquidity process for both operating and contingency purposes are no longer “nice to have” tools, they are required critical elements to effectively manage your balance sheet. Asking these questions should automatically jump-start strategic discussion at ALCO.

Having too much liquidity—or not enough—going forward will clearly impact every other aspect of the balance sheet: loans, investments, retail deposits, and wholesale funds.

If a change in liquidity strategy is needed (i.e. you have too much or not enough), it will impact the loan and investment strategy of the bank (put on more or less, fixed or variable, etc.), the retail and wholesale funding strategies, interest rate risk management and, therefore, growth and earnings strategies.

If the answers to these questions are not continuously discussed at ALCO, you are missing strategic opportunities to increase income and reduce risk on your balance sheet.

Start with disciplined forecasting

Disciplined loan forecasting is critical to managing operating liquidity. Variance in forecast is inevitable; however, continued substantial variances should be unacceptable as it will negatively impact strategic action and, therefore, earnings. If this doesn’t work well at your institution, you can fix it simply by making it the priority it should be.

The wholesale portion of your balance sheet should be easy to factor into liquidity management. Investment and borrowing maturity schedules are readily available.

Retail deposit forecasting is much more difficult—both today and in different rate environments.

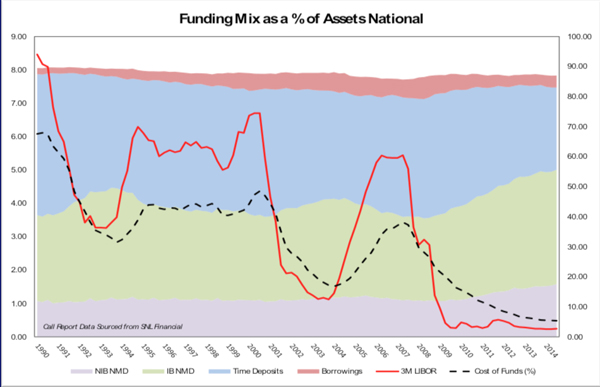

Non-maturity deposits have grown industry-wide since rates bottomed out in December 2008. This growth in non-maturity deposits has been a combination of more dollars on bank balance sheets, but has also been a change in mix from time deposits. This trend can be seen in the chart below of deposit balances for all FDIC-insured institutions.

Going back through multiple interest rate cycles over the last 25 years, a number of trends grow quite clear.

Non-maturity deposits increase, while time deposits decrease, when market rates decline (with the opposite occurring as rates rise). These mix change trends occurred in the early 1990s, 2000s, and again since 2008.

Is this trend and mix change identifiable on your balance sheet? How many of the customers will shift back into CDs once they are incented to? Prior to 2008, when rates were rising or falling, industry-wide deposits were declining. There was a mix change, but overall deposits were declining.

Since 2008 industry deposits have been increasing. Will this change the amount of potentially volatile liabilities on balance sheets and cause more mix change than in previous cycles?

Qualitatively and quantitatively support assumptions

Chances are your institution has had non-maturity deposit growth above its normal trendline since 2008. Can you identify these accounts? Are these core accounts that have multiple relationships with the bank? How many dollars are represented and can you afford:

1. To increase deposit rates to maintain balances?

2. To allow balances to leave for a higher rate somewhere else?

3. To make a shift in mix back from non-maturity to time deposits?

You can answer these questions with anything from management’s experience (i.e. gut feel) to quantitatively supported deposit studies/analysis.

The answers to these questions can materially change the interest rate risk profile of a balance sheet and potentially lead to poor decision making if the incorrect assumptions are used.

Interest rate risk

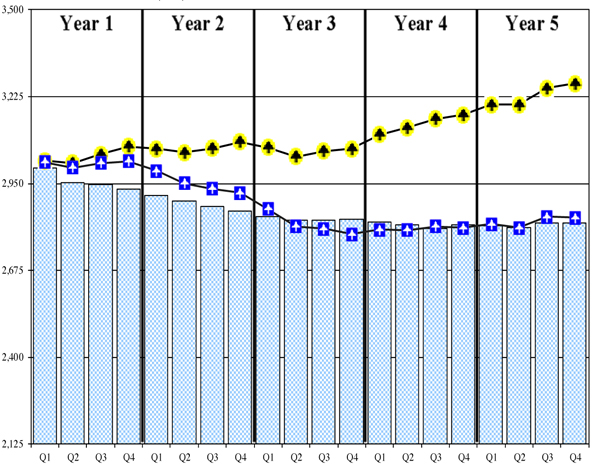

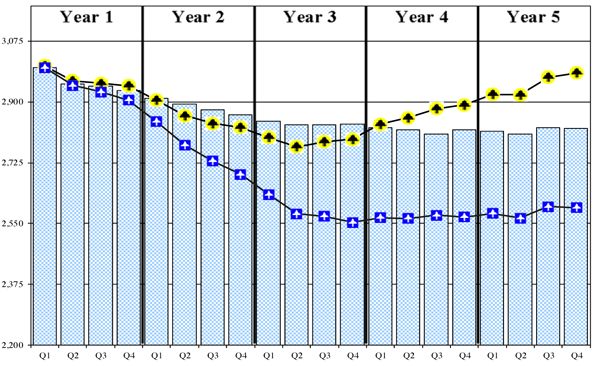

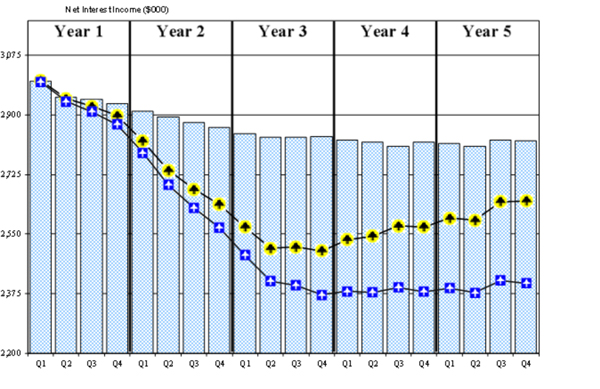

Depending on the assumptions used in the models, your balance sheet could be well matched, liability sensitive, or asset sensitive. See the graphs below changing deposit pricing beta assumptions and mix change from non-maturity to time deposits.

All three of these simulations are of the same bank. The bar graph is rates unchanged (without balance sheet growth), the yellow line is a parallel 200 basis points rising-rate scenario and the blue line represents a 200 basis point non-parallel rising rate environment (i.e. “bull flattening”).

Base Scenario (Figure 1)

Increased Non-maturity Deposit Betas (Figure 2)

Increased Non-maturity Deposit Betas and Shifting Potentially Volatile Accounts into CD Specials Figure 3)

Is this bank well matched, liability sensitive, or asset sensitive? It clearly depends.

When was the last time you updated and/or stress tested the beta and mix change assumptions in your asset/liability model? The vast difference in the simulations above will clearly impact strategies employed at your ALCO. The assumptions need to be as accurate and realistic as possible (remember the old adage, garbage in=garbage out) and supported by quantitative and qualitative arguments.

Connecting interest rate risk and liquidity

What about the impact of changes in mix/balances on your liquidity position? How many potentially volatile liabilities do you have? How many are you willing to lose? How many can you afford to lose?

By definition, rising rates means liquidity being taken out of the system. The interest rate risk impact of beta and volatility changes is clear in the simulations above, but what do those changes do to the liquidity position? Have you stress tested it under low/medium/high risk scenarios? And have you established triggers at which point action will be taken, and run relief scenarios?

The inter-relation between interest rate risk, liquidity, and capital needs to be fully understood by all stakeholders—ALCO, senior management, the board.

Managing risk, not avoiding risk

You cannot be in banking without taking risk.

There is interest rate risk on your balance sheet. There is liquidity risk on your balance sheet. Too much interest rate risk (exposure to rising rates, for instance) can be offset by strong liquidity and the ability to grow your way through that scenario. However, what if that rising rate scenario is combined with high levels of deposit volatility and a tight liquidity position?

Whether or not short-term rates rise any time soon is out of your control. Understanding the impact of different rate scenarios (not just rising, as long-term rates could come down) on all aspects of your balance sheet (interest rate risk, liquidity, earnings, and capital) and how they inter-relate is not.

About the author

Keith Reagan is a managing director at Darling Consulting Group. He has more than 20 years of experience working directly with community banks, helping them improve their overall performance through proactive management of liquidity, interest rate risk, and capital. He works to develop strategies that best fit the risk/return dynamics of their balance sheets. Reagan has served on the faculty of ABA's Stonier School of Banking, has written many articles for a variety of professional publications, and is the editor of DCG's monthly periodical, the DCG Bulletin.

Tagged under ALCO, Management, Financial Trends, Risk Management, Rate Risk, ALCO Beat, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story