Banks most reliant on interchange fees

Looking at Durbin amendment’s effect as fifth anniversary of rule nears

- |

- Written by SNL Financial

SNL Financial, part of S&P Global Market Intelligence, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial, part of S&P Global Market Intelligence, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Maria Tor and Venkatesh Iyer, SNL Financial staff writers

Despite earning a dismal rate on loans, the banking industry has grown profits in the years since the financial crisis, finding other ways to increase income.

One of those ways is through interchange fees, or the fees paid by merchants to banks when bank customers use a debit or credit card to make a purchase. Interchange income has grown after new regulation imposed limits on debit card fees in late 2011.

Durbin amendment approaching fifth anniversary

The Dodd-Frank Act of 2010 included the "Durbin amendment," the more common name for Regulation II, which mandated that banking regulators limit the amount of debit card interchange fees that banks could charge merchants.

The Federal Reserve rule went into effect Oct. 1, 2011, and only applies to banks with assets above $10 billion. The regulation capped the maximum permissible interchange fee that an issuer may receive for an electronic debit transaction at the sum of 21 cents per transaction, plus 5 basis points multiplied by the value of the transaction, plus up to an additional 1 cent per transaction if the issuer implements fraud-prevention policies and procedures.

The Fed said that for the average debit card transaction of $38, a debit card issuer above $10 billion in assets could charge no more than 24 cents. The rule does not apply to credit card or prepaid debit card transactions.

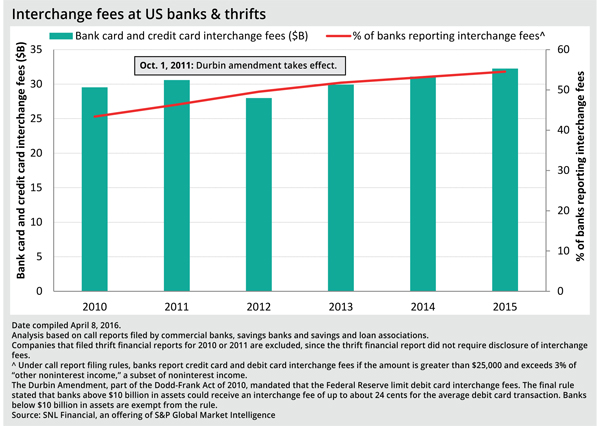

While the banking industry's interchange income took a hit in 2012 after the rule went into effect, the aggregate interchange income has risen back to pre-Durbin levels, according to regulatory data.

Banks report "bank card and credit card interchange fees" in Form Y-9Cs and call reports. Data is somewhat limited because banks only have to disclose the line item if their interchange fees equate to more than 3% of "other noninterest income" and total more than $25,000; 54.5% of banks reported the figure for 2015, up from 43.4% who reported it for 2011.

Analyzing institutions’ numbers

To allow comparisons across years since 2010 in the above graph, the analysis excludes institutions from the aggregates that filed a thrift financial report for either 2010 or 2011. The thrift financial report did not require filers to break out interchange fees, and so including these companies causes an artificial increase in the aggregate figure in 2012 when thrifts had to begin filing call reports.

Excluding these former thrifts, aggregate interchange fees from debit and credit card transactions fell to $27.97 billion in 2012 from $30.58 billion in 2011. But since then, interchange fees rose to $32.25 billion in 2015, an increase of 15.3% from 2012 levels, while overall operating revenue for banks, excluding former thrifts, grew by only 1.7% over the same time period.

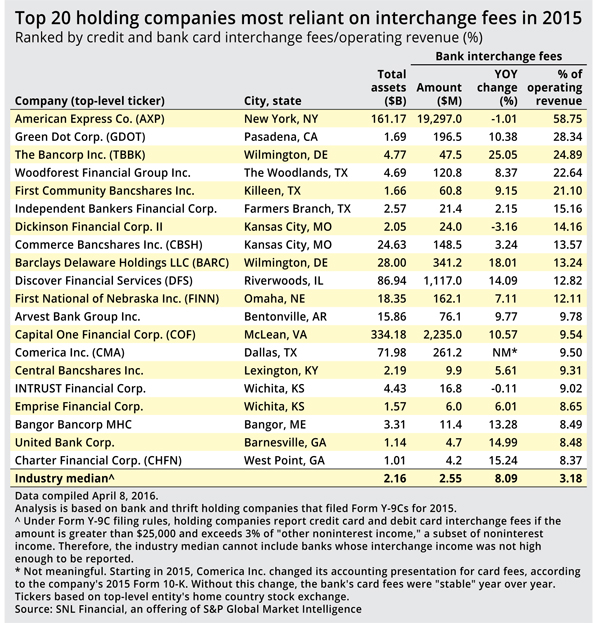

The potential loss of interchange income is a major reason banks approach growth above $10 billion in assets with caution. Banks that earn significant income from debit card interchange fees will almost certainly see a decline after they become subject to the Durbin amendment. Credit cards and prepaid debit cards are not subject to the interchange cap, so it's not surprising to see American Express Co. and Green Dot Corp. at the top of the ranking of holding companies most reliant on interchange income as a percentage of operating revenue. Twelve of the top 20 banks most reliant on interchange income have less than $10 billion in assets.

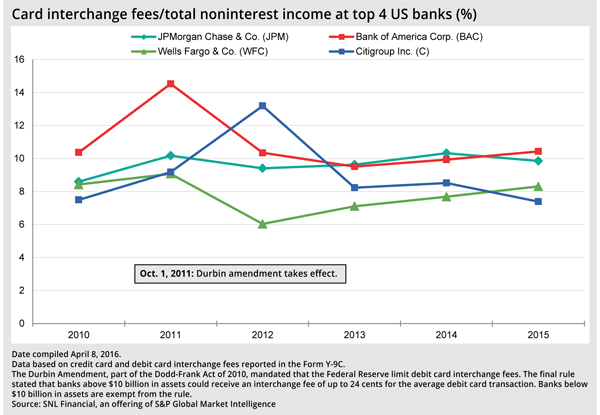

At the largest four U.S. banks, which hold nearly 40% of the country's deposits, growth in interchange income has been mixed.

JPMorgan Chase & Co. saw its 2015 interchange income fall to $4.89 billion in 2015 from $5.31 billion in 2014, or to 9.9% of noninterest income from 10.3% of noninterest income. Bank of America Corp., on the other hand, reported interchange income rose to $4.34 billion in 2015 from $4.30 billion in 2014, or to 10.4% of noninterest income from 9.9% of noninterest income.

Regulatory data is not yet available for the first quarter of 2016, but some of the early reporters have seen positive trends in card purchase volume.

Wells Fargo & Co. CFO John Shrewsberry said during the company's earnings conference call April 14 that debit card purchase volume was $72.4 billion, up 9% from the year-ago quarter, and credit card purchase volume was up 13% from a year ago to $17.5 billion.

Bank of America CFO Paul Donofrio also said April 14 during the company's earnings call that credit card spending was up 8% in the first quarter compared to the year-ago quarter, adjusted for the divestiture of a $1.6 billion credit card portfolio to U.S. Bancorp.

This article originally appeared on SNL Financial’s website under the title, "Banks most reliant on interchange fees"

Tagged under Management, Lines of Business, Payments, Cards,

Related items

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- JP Morgan Drops Almost 5% After Disappointing Wall Street

- Banks Compromise NetZero Goals with Livestock Financing

- Banks, Mastercard and Visa Settle Antitrust Case

- OakNorth’s Pre-Tax Profits Increase by 23% While Expanding Its Offering to The US