Talent competition: missed opportunities as battle intensifies

Evolution in types of recruits banks seek plays a part

- |

- Written by Crowe Compensation Survey 2017

First of a series: Many bank incentive programs bear no connection to individual performance, according to Crowe Horwath’s most recent human resources survey. The survey also uncovered deficiencies in some basic HR practices.

First of a series: Many bank incentive programs bear no connection to individual performance, according to Crowe Horwath’s most recent human resources survey. The survey also uncovered deficiencies in some basic HR practices.

As competition for productive employees in the banking industry intensifies, a recent survey suggests many banks may be overlooking some effective techniques that could help them compete more effectively for high-performing talent. This is further complicated because banks have begun seeking people with skill sets new to the industry for jobs rapidly changing in nature and expectations.

Today’s competitive hiring environment

For the past several years in our firm’s surveys, many banking executives have expressed concerns that the competition for talented employees seems to be intensifying.

Human resource officers have reported that the task of finding capable and motivated employees seems to be growing more difficult, and the challenge of retaining proven performers seemed harder than it was in years past. The most recent survey confirms that impression and helps identify some of the factors that likely are driving the competition.

Every year, Crowe Horwath LLP surveys financial institutions throughout the United States about compensation trends, benefits, incentives, and other human resource issues. The 2016 Crowe Financial Institutions Compensation and Benefits Survey of 378 banks and thrifts confirms that the contest for talented employees is becoming increasingly competitive, as the market responds to the basic law of supply and demand.

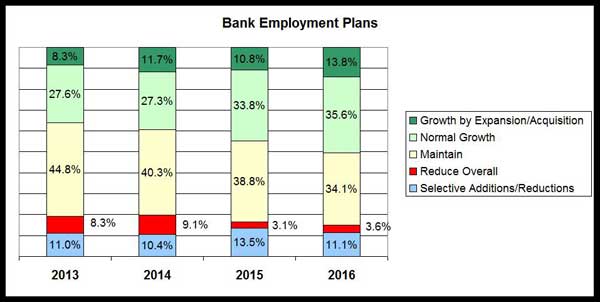

Nearly half (49.4%) of survey respondents reported that they plan to increase their staffing levels in the coming year, either in response to normal growth or as a function of expansions or acquisitions.

As Exhibit 1 illustrates, the number of survey respondents who plan to increase staffing levels has been growing steadily over the past four years, while the number who plan to reduce or maintain current staffing levels has been declining.

Exhibit 1: Employment Plans

Source: 2013-2016 Crowe Horwath LLP Financial Institutions Compensation and Benefits Surveys. Numbers may not total 100% due to rounding.

Other survey responses support this observation. For example, employee turnover has reached its highest levels in more than a decade, with nonofficer turnover averaging nearly 18.7% during 2016.

It is no surprise, then, that finding and hiring the right people has ranked consistently among the top three human resource management issues in recent surveys. In 2016, 81.6% rated this effort as being of high importance.

Not just a matter of more dollars

Finding and hiring talented people is not simply a matter of offering higher pay in order to boost staffing levels.

In fact, boosting pay and benefits can have unexpected consequences.

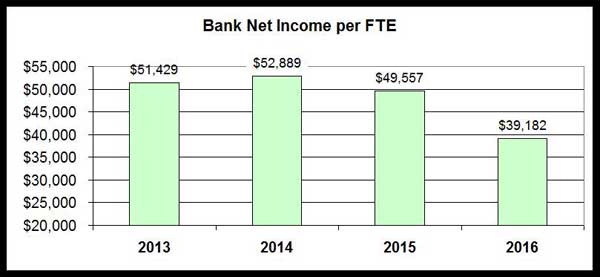

As shown in Exhibit 2, the steady increase in staffing levels over the past few years has not always produced desirable results.

Exhibit 2: Net income Per Employee

Source: 2013-2016 Crowe Horwath LLP Financial Institutions Compensation and Benefits Surveys

When survey respondents were asked to measure their organizations’ net income against total staffing levels, the results indicated a steady downward trend in net income per full-time equivalent (FTE) staff.

There could be many varying reasons for such a declining return on investment. These include outside market and economic factors that are beyond the organization’s control.

Nevertheless, a comparison of several other survey responses suggests one recurring problem within many banks is a lack of consistency in many of their hiring and staffing practices. In addition, this is compounded by some notable discrepancies between their stated human resource priorities and the actual programs that are in place to address human resource issues.

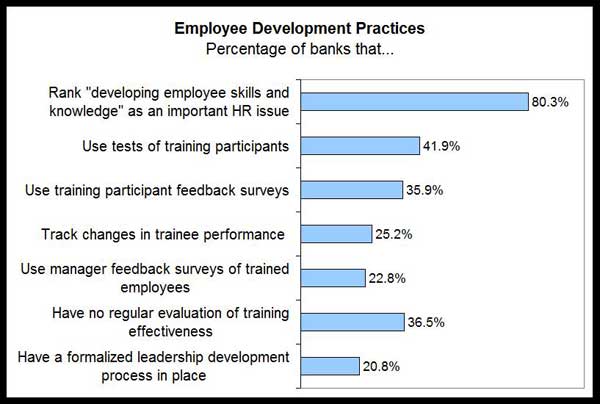

For example, 80.3% of the 2016 survey participants said “developing employee skills and knowledge” is an important human resources management issue. Yet the proportion of respondents who use various well-established methods for evaluating the effectiveness of their training is significantly smaller (Exhibit 3).

In fact, more than a third (36.5%) of the respondents said they have no program for evaluating training effectiveness at all— and barely one-fifth of the responding institutions said they have a formal leadership development program in place.

Exhibit 3: Employee Development: Priority Versus Practice

Source: 2016 Crowe Horwath LLP Financial Institutions Compensation and Benefits Survey

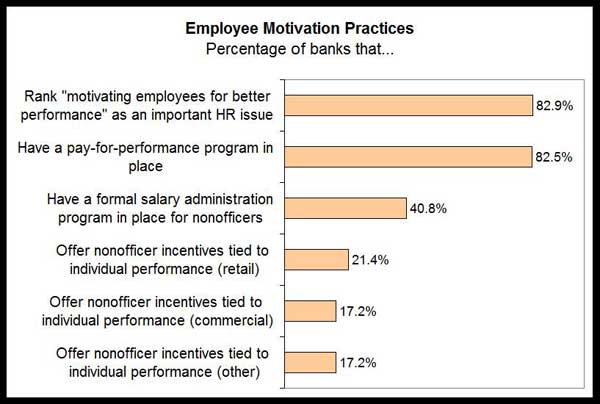

Similarly, 82.9% of responding banks rated “motivating employees for better performance” as an issue of high importance. A nearly equal number report they have pay-for-performance programs in place (Exhibit 4).

But let’s take a closer look at the details of the respondents’ incentive programs. This reveals that many incentives take the form of annual discretionary cash bonuses, holiday bonuses, profit-sharing plans, and similar awards that are not tied directly to individual performance.

Only about one-fifth of the respondents award their nonofficer employees incentives that are tied to individual performance.

Another significant finding is that only 40.8% of the participants have a formal salary administration program in place. Such a program normally would be considered a basic starting point for developing pay strategies that are effective at motivating employees and incentivizing performance.

Exhibit 4: Motivating Performance: Priority v. Practice

Source: 2016 Crowe Horwath LLP Financial Institutions Compensation and Benefits Survey

These disparities suggest that, while bank executives recognize the importance of basic human resource management processes such as effective training and a well-developed salary administration program, the execution of specific tactics to carry out these priorities often is incomplete or inadequate.

Rapid evolution in needed skills complicates search

Banks’ efforts to develop more coherent and consistent staffing strategies can be further complicated by another factor: Their rapidly changing business needs are altering the basic skills they look for in their employees.

Consider, for example, the most visible customer-facing position in most banks—the front-line teller in the branch.

Tellers’ basic duties, along with the tools and techniques they employ, have changed significantly over the past decade or so—and so have the skills that are needed in branch personnel. Compared to the tellers of days gone by, today’s branch employees spend less time taking care of routine transactions (which can be handled more efficiently either online or automatically) while spending more time proactively building relationships or engaging in consultative selling.

Today’s branch visit is more likely to be focused on a special problem or situation, which means branch personnel need a different set of skills.

Technology also has had a profound effect on the skills that are needed not only in customer-facing positions but also in administrative or managerial functions.

The advent of paperless processing systems has transformed many traditional back-office positions, while marketing and strategic planning positions now require an understanding of big data principles and data-driven decision-making.

At the same time, of course, the demand for skilled IT personnel continues to grow.

Finally, it is important to recognize the generational dynamics that are underway in the banking industry—and in the rest of the economy as well. The combination of pay, incentives, and benefits that attracted and retained baby boomers is often less effective in motivating Generation X employees or millennials.

Strategic staffing becomes essential

The complexities and complications of today’s competitive labor market make it increasingly important that banks approach their staffing challenges strategically. They must make sure that their organizations’ hiring, training, and compensation systems are well-aligned to their overall business strategy.

Broadly speaking, the practice of strategic staffing encompasses several fundamental subpractices:

• Organizational effectiveness. First, overall organizational structure must be designed to accomplish the organization’s mission in the most effective way. Following on that, the individual job design and duties must support that structure and mission.

• Workforce planning. Once job design and duties are appropriately defined, the next challenge is identifying the talent and skills that will be needed—in both the immediate future and in the longer term—to accomplish the organization’s strategic goals.

• Targeted recruiting. Rather than merely filling job openings as they arise, strategic staffing involves recruiting for specific skills and abilities, including both technical skills and broader capabilities such as critical thinking and learning ability.

• Talent development. Continuous, planned, and measured skill development—also known as “upskilling”—helps improve specific job performance while also keeping employees motivated by helping them to move along a clear career path.

• Total rewards compensation. A total rewards approach that encompasses pay, incentives, and benefits as well as important cultural and work-life balance considerations can help motivate and retain high-performing employees.

Finding, recruiting, motivating, and retaining talented employees is always a critical concern for financial services organizations, and banks can expect the competition for the best performers will continue to intensify.

As it does, developing consistent, coherent staffing strategies will become even more essential to improving bank performance, enhancing overall value, and achieving the organization’s long-term goals.

Read Part 2 of series: Employee turnover: Dealing with costs seen and hidden

Read Part 3 of series: Employee incentive plans leave room for improvement

Tagged under Human Resources, Management, CSuite, Community Banking, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story