Using Intelligent Customer Engagement to Acquire, Deepen and Grow Primary Bank Relationships

“The next decade will be about systems of engagement.”

- |

- Written by Jessica Cheney, Vice President Product Management, Strategic Solutions Bottomline Technologies

“The next decade will be about systems of engagement.”

Truer words were never spoken — and the reality of those words is reflected all around us as banks are waking up to the need to create digital experiences that provide value and drive customer growth. Just look at the observations of bankers such as Ian McKintosh, CIO of LegacyTexas Bank, when he realized that the bank couldn’t become the primary relationship for its existing commercial customers (let alone attract new customers) until it could compete with more sophisticated features.

“We’ve noticed a shift in the digital expectations of our clients. As the generation of professionals that were raised in an age of social media, technological advances and instant communication mature into decision making roles, they demand those same digital advances in their business experience. We knew that in order to attract and retain that audience, it was critical to meet those expectations with our banking solutions.”

These are observations that go far deeper even than the audience that McIntosh is referring to. Millennials might be the oft-used rationale for digital transformation, but the reality is, technology has transformed the way consumers of all ages and backgrounds research, choose and pay for products and services. The expectations of allcustomers have changed, and banks need to be ready to respond to those evolving needs.

Because of that, as we close in on the second half of 2019 and round the corner towards 2020, banks are beginning to face the jarring reality that they are no longer being evaluated on the traditional banking measures of reputation or branch proximity -- those days are long gone. Instead, they’re being measured by how effectively, authentically and intelligently they can engage with customers in the digital environments those customers expect and prefer to do business in. To raise the stakes even higher, they’re being judged by customers who have grown accustomed to the levels of service and innovative technology set by organizations such as Venmo, Amazon, Uber and AirBnb.

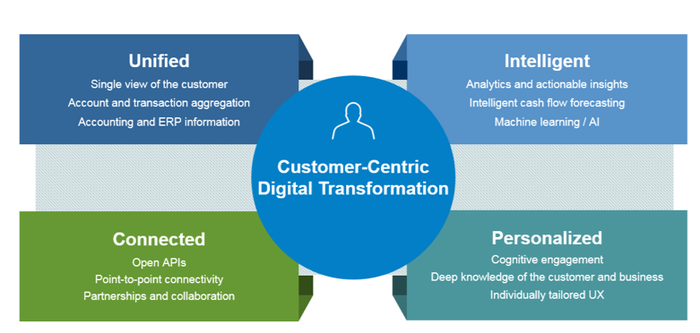

There’s no question that the challenges banks have before them are significant. Upending decades upon decades of status quo, it is no longer enough to simply provide transactionally-based payments and cash management services -- that’s a commodity in this day and age. Winning the primary banking relationship now requires providing customers with a superior digital experience at every single touchpoint, executed in unique and compelling ways and delivering a level of intelligence that makes both the customer and their business smarter.

Opportunity, Risk & Differentiation

Banks that haven’t made the shift to thinking about their organization as a digital experience company whose success requires them to deliver a seamless digital journey from account acquisition through onboarding, digital banking and relationship management are not only losing out, they’re putting themselves at tremendous risk. Long-term customer and franchise value are on the line as banks engage in a do or die battle to deliver actionable, intelligent insights to customers through the digital channels.

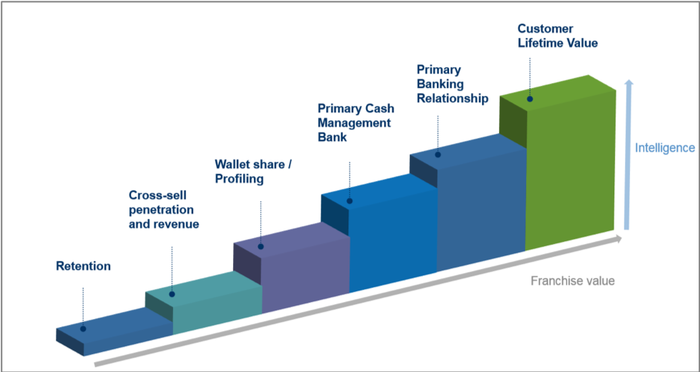

Those banks that can’t make the switch will be relegated to the “also ran” category while successful banks are rewarded with more profitable sales, increased lending opportunities and deeper customer relationships, which is the key to driving greater lifetime value.

The good news in all of this is that making a shift towards systems of engagement represents a tremendous opportunity for banks -- one that is often overlooked in the intense pressure to answer the question of “how can we address changing market need?”

Banks can easily seize the opportunity before them and achieve significant differentiation simply by allowing their digital presence to take precedence over their local scale and geography. They can then further propel their success by taking advantage of the emergence of an open and integrated environment.

Data is king in the world of business today and banks have the good fortune of having tons of it at their disposal. That makes them ideally positioned to provide value-added services that significantly enhance their position with customers.

There is a fundamental shift taking place in financial services. Due to changing customer expectations regarding digital services, more competition and lower switching costs, Banks are facing a serious threat to their primary relationships status that they must address soon, before it’s too late.

Experience as the Product

The ultimate reality in all of this is the fact that the customer experience is now the product in banking. It’s an interesting mind shift for an industry that has always been focused on delivering financial products, but thankfully customers have been clear about what they’re looking for. They want (and need) seamless digital experiences that make their businesses simpler, smarter and more secure, it’s as simple as that.

For banks that can provide that level of digital engagement, victory will be assured.

Tagged under Technology, Financial Trends, Tech Management, Mobile, Online, Customers, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story