How APIs will change retail banking

New study sets out models for collaboration between banks and fintech

- |

- Written by Steve Cocheo

APIs may be banks' opportunity to cash in, says a new report by Capgemini and Efma.

APIs may be banks' opportunity to cash in, says a new report by Capgemini and Efma.

Not so long ago, banks used the word “legacy” as a positive—heritage, staying power. Now, when “banks” and “legacy” appear in the same sentence, it’s more in the sense of watching someone trying to run the 50-yard dash standing in a burlap sack.

Fintech companies come off as the cool kids on the block. However, that’s not the end of the story, according to the 2017 World Retail Banking Report from CapGemini and Efma. The future looks less like a race, and more like a journey built on collaboration.

Fintech firms come into the world with big ideas, new technology, and no “legacy” dragging behind. Like other newborns they also seem to have a voracious appetite compared to their size. Attend any event devoted to fintech and the centerpiece, or at least a side-show, consists of opportunities for young firms to strut their stuff before venture capitalists. Fintech firms suck down millions in funding, and that money turns into the front-end eye candy and back-end data analytics that help make them exciting.

The retail banking study found that, throughout the international sampling, many retail financial services customers have voted with their feet—both ways. The report states that almost one-third of banking customers—29.4%—use products and services from nontraditional providers. Of that fat slice, more than half has relationships with three or more nontraditional firms. (The 2016 report indicated that the researchers saw a “tipping point” coming in fintech acceptance. That appears to have arrived.)

The influence of younger customers and tech-savvy customers on those aggregate numbers can’t be ignored, but those aren’t the only factors.

Banks aren’t chopped liver

What can banks put on the table against all that? The new report says banks need not surrender the playing field to the “upstarts.”

“Banks have vast and deep reservoirs of knowledge on how to navigate banking networks and regulations,” the report states. “And they are no strangers to many of the advanced technologies being used by newer firms, though they may not be as quick to deploy them. Large banks have resources that far outstrip what even the most venture-capital flush tech firms can access. And, perhaps most important, they’ve already got the customers.”

That’s to the industry’s good, but the report also notes that those advantages aren’t enough. Customers have seen what fintech provides and they like it.

“Clunky interfaces and disjointed service channels will not cut it once customers become accustomed to slick designs and conveniences like biometric IDs and one-click transactions,” the report says.

And the industry’s efforts to fight back on fintech’s own terms, the report says, “have largely fallen flat with many firms.”

Can fintech firms do no wrong? Asked that, two senior analysts at CapGemini said no one has all the answers or all the cards. Collaboration is the natural result, and is what they are hearing from the consulting firm’s banking clients.

Bill Sullivan, global head of Financial Services Market Intelligence at Capgemini, says there’s been a rapid shift in the viewpoint of both sides.

First, fintechs arrived on the scene, brash and ready to bulldoze the incumbents, Sullivan says, and banks denied any impact. Then logos for all the new players began popping up everywhere and the competition began in earnest. But more recently, the trend has been for banks to recognize what fintechs have going for them, and for fintechs, struggling to grow, to recognize what advantages banks have been sitting on.

“There’s a more pragmatic view now,” says Sullivan.

Nilesh Vaidya, senior vice-president, Capgemini Financial Services, explains that the key theme of the 2017 report is the promise of collaboration. Fintech is coming to be seen as the product, and banks as the established distribution channel.

Collaboration thus plays to the strengths of each, says Sullivan.” Banks have gotten the message and are adapting rapidly,” say Vaidya.

Partners or vendors?

Will major banks, with their deep pockets, behave like white corpuscles, engulfing and absorbing the newcomers?

Acquisitions have and will come, says Vaidya, but massive absorption of fintech by banking doesn’t appear to be the future.

Instead, he says, if you are going to hark back to basic biology for an analogy, he prefers symbiosis, a relationship where two organisms co-exist, each providing something the other needs.

Co-dependence is important, but so is the independence that is also implied. Vaidya suggests that fintechs that remain independent from bank partners can serve an important role as a source of research and development that might not occur inside a traditional bank.

As the idea of partnering has caught on, the actual role of fintech players has been debated. Are they truly “partners”? Or are they solely vendors to the banks, operating under a trendier label?

Vaidya and Sullivan point out that the lines can blur a bit here. Some fintechs collaborating with banks aren’t just providing their technology to the bank for its use, but are playing an active role where the customer relationship is concerned. Onboarding serves as one example. A tech partner may be taking a decisive role in the onboarding process. This sets things apart from a vendor providing software and playing no active role.

“It becomes more of a partner relationship,” rather than a customer-vendor relationship, according to Sullivan, “because the fintech holds some client responsibility.” Further, where fintechs play such a role, they take on a measure of risk, and thus also seek a share in the rewards of the ultimate customer relationship.

Importance of APIs

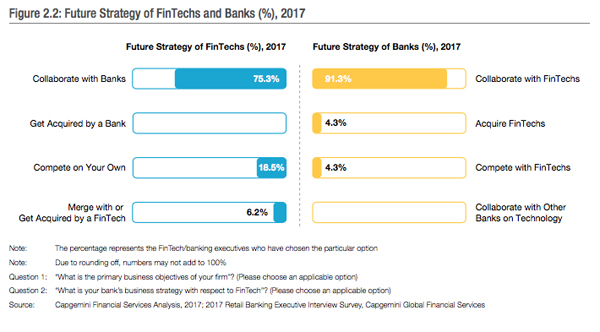

The future as one of collaboration isn’t just a pet theory of the study’s authors. According to the survey report 91.3% of banks sampled and 75.3% of fintechs say that they expect to partner with each other.

There’s more to the relationship than this take on partnership structure. Vaidya says it is important to understand that fintechs bring ideas to the table, but major banks bring muscle. A tech-savvy bank may be able to apply 100 staff engineers to a priority project.

In Vaidya’s view, fintech delivers ideas, and such banks “can industrialize them.”

The bridge between these two industries, explored at length in the CapGemini/Efma report, is the API (application program interface). A fundamental here is that APIs can help banks and fintech firms to collaborate by going around technological incompatibilities. The term “API” has many nuances, but put simply, APIs offer an ability to build or change software more easily using existing “parts” that offer better functionality—like upgrading a computer with better memory.

“There may be nothing more crucial to the future of banking,” says the report about APIs. The population of APIs has exploded, surpassing 50,000 worldwide, and the population has grown since that 2016 estimate.

“APIs form the basis of partnerships with nimbler fintechs, allowing banks to shed their traditional sluggish approach to technology and begin embracing creativity and customer-focused innovation,” the report states.

Another advantage offered by APIs, the report suggests, is that the flexibility that APIs offer reduces banks’ feeling that they will be locked into a particular approach as they develop and launch new products.

The report places heavy reliance on the advent of open APIs. These make both data and functionality available to players with which the bank may have not formal business relationship. By contrast, private APIs are used internally to make bank systems “talk” to each other, and partner APIs smooth collaboration between banks and formal partners.

Regulatory landscape differs

In Europe, the growth of open APIs has been chivvied along by regulators, through the European Union’s Payment Services Directive 2. This effort is pushing banks to open customer data to third-party access via APIs. This practice is, naturally enough, called “open banking.”

In this country, regulators have not been as forward in forcing the issue. In a speech earlier this year, Federal Reserve Board Gov. Lael Brainard spoke of the challenges and risks of opening customer data to third parties, including the issue of whether customers fully appreciate the risks of allowing their information to be accessed by such companies. The speech was high on cautionary notes, and not what one would call a ringing endorsement of open banking. [Read “Mobile apps, connectivity, and banking’s future”]

Yet Vaidya thinks movement is in the offing. While he acknowledged that U.S. regulators have hung back, publicly, he predicts that “you’re going to start to see change in spite of that.” He believes that banks will start to see opportunities in this area, and there is a strong possibility that this will be because they see the possibility of making fee income through open APIs.

“As third-party providers increasingly tap into bank APIs, banks have the opportunity to charge for their data and create new revenue sources,” the study observes.

The report outlines several models for such revenue generation. One option that seems to be favored by both fintechs and banks is a fee per transaction executed via API—essentially, a user fee or “toll.” Alternatively, both partners would share in any revenue generated through use of a bank’s API.

Security concerns everyone

One wrinkle in APIs is that they open things up to smaller players.

“Smaller banks can do different things than was possible earlier,” says Vaidya, “and it comes at a lower price point. This opens new doors for them. The playing field is getting leveled.”

They will have to keep their eye on compliance issues, Vaidya cautions. As always with third-party elements, the bank offering the product to the consumer is where the compliance duty resides. Thus each bank’s team will need to validate APIs that the institution wants to implement.

“Security is very important,” says Vaidya.

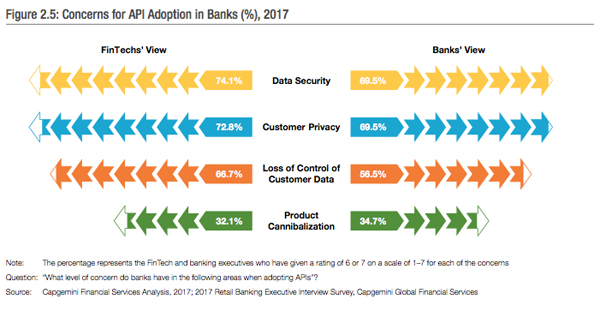

Indeed, in these days of hacks and ransomware, data security continues to be a concern, the report noted. Nearly seven out of ten banks raised this issue and 74.1% of fintechs did as well. Similar concerns surfaced regarding customer privacy.

The consultants think assurance on this score is coming.

“It is going in the right direction,” says Vaidya, “though right now there is the potential for exposing information to third parties.”

Download the Capgemini/Efma 2017 World Retail Banking Report

Tagged under Retail Banking, Channels, Feature, Feature3,