Overdraft service demands a decision

Your pricing may be off. Here are thoughts on how to adjust it

- |

- Written by Mike Moebs

- |

- Comments: DISQUS_COMMENTS

Overdraft fee policy can follow two different strategies, according to Mike Moebs, "The Prairie Economist." Financial institutions have a choice of polar opposites—but he says they must do something.

Overdraft fee policy can follow two different strategies, according to Mike Moebs, "The Prairie Economist." Financial institutions have a choice of polar opposites—but he says they must do something.

Financial institutions offering fee-based overdraft service may be nearing a crossroads in their pricing. I’m going to lay out a case to you that your bank should either raise its price or cut its price, but that you can’t stand pat in 2017.

Bear with me while I cover a bit of history and the latest research, and then I’ll hit you with my argument.

Where pricing’s at versus where it “should” be

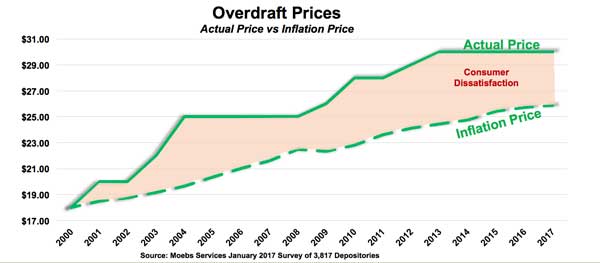

In 2000, the median overdraft price was $18. A price less than $20 was not controversial then, and it is not today. Using the Minneapolis Fed’s Inflation Calculator, the current median price of an overdraft today should be $25.

But it’s not.

According to the latest Moebs $ervices Overdraft Study, released in January, the median price of an overdraft is $30. Matching the current median price of $30 with the inflation-adjusted price of $25, that means that today’s median price is 20% more for a service that has not changed enough in value or cost to warrant this price increase over 17 years. (The report was based on our survey of 3,817 banks, thrifts, and credit unions.)

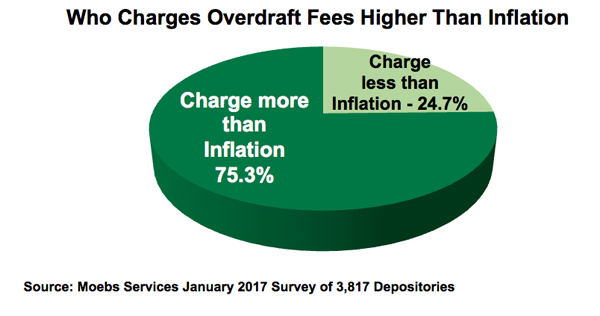

In fact, we found that 75.3% of all financial institutions charge an overdraft fee greater than the inflation-adjusted overdraft price.

But there’s another trend going on here. Taking a look at banks and credit unions separately, there is a clear difference between who prices higher than inflation and who doesn’t.

In 2000 banks and credit unions charged $20 and $15 for an overdraft (median prices), respectively. Therefore, the inflation-adjusted price for banks today would come out to $27.82, while the credit unions would come to $20.86 per item.

Using the inflation-adjusted price for each type of financial institution, about 26.4% of banks are currently priced below or equal to the inflation-adjusted price. By contrast, only about 7.7% of credit unions are priced below or equal to the inflation-adjusted overdraft, with a current median price of $29 per item.

The pricing behavior differences between banks and credit unions also become evident when comparing the 2000 price to the current price. Banks increased their median price 50% from $20 to $30 in 2017. Credit unions, on the other hand, nearly doubled their median price from $15 in 2000 to $29 in 2017—a 93% hike.

Credit unions cultivate an image of being more consumer-friendly providers and by many standards are. Yet when examining the history of overdraft prices, we see that credit unions have been increasing their price at a much quicker rate and now are almost on par with banks.

“But if I lower my price, won’t I lose a lot of revenue?”

Basic micro-economic theory states that lower pricing increases volume. With overdrafts, the question then becomes: How far should the price be reduced to stimulate enough volume to increase revenue?

Here’s how it turns out: Those financial institutions with an overdraft price of $25 or less are producing more volume, which increases revenue over time.

Case in point are the community banks with less than $100 million in assets. They have maintained their overdraft price at a median level of $25 for the past seven years, while their current ratio of service charges on deposit or non-interest revenue to assets—dominated by overdraft fees—is 0.22%.

By comparison, the Too Big To Fail banks have a price of $35, while producing the same service charge revenue-to-assets ratio of 0.22%.

On a relative basis, community banks are maintaining an inflation-adjusted overdraft price and making just as much money due to volume with a much more consumer-friendly price.

Lower prices are showing up

Institutions in the Washington, D.C., and Washington D.C. CBSA* have lowered their median overdraft price in the past nine months. This lower pricing trend also includes the states of West Virginia, Pennsylvania, Maryland, and Virginia.

The reduction of overdraft price has been from 50 cents to $2. While 50 cents may seem small, it is statistically significant in the overdraft business because the prices for overdraft services tend to change every two to five years for most depositories.

The significance of the city and states decreasing their pricing is due to the overall overdraft environment. Neither the banking industry nor the credit union movement has changed their price as an individual group. This rarely happens—for a city and states to change but not industry groups—signaling that overdraft prices are a’changing.

“But how can I lower price and gain revenue?”

Overdraft volume is driven by overdraft limits. That’s how far below $0 a financial institution will allow consumers to take their checking account negative. Most bank, thrift, and credit union limits have not changed their limit in over 15 years. They’ve been stuck at $500.

Changing the limits from $500 to $5,000 will increase overdraft volume.

Of course, that’s extreme.

Instead, consider installing five to ten tiers of limits. These would be based on the financial profiles of overdraft users. This would represent a measured way to increase volume while controlling risk.

Jump or dive? That is the question

Now, let’s get back to my point about this being a time for decisions.

Ultimately it appears that the overdraft price of $30 has peaked.

It is time for all depositories to take a long hard look at how they price overdrafts.

They must decide to:

• Jump ahead with a high price and have less volume, or

• Take a dive with a low price to drive volume up.

This is how you can do it:

1. Get OD friendly. As suggested in the “FDIC Overdraft Guidelines,” implement de minimis balances of $3 to $25, and cap overdraft charges to two to five a day.

2. Increase limits. Limits are volume. Moebs Surveys have shown that overall dollar limits at banks and credit unions have not changed in over 15 years. Most are at $500. Increase these limits from $1,000 to $5,000 and have multiple levels.

3. Change your overdraft pricing—up or down. Then you will see increasing revenue coming into your institution.

Finally, remember my point about where inflation-adjustment says prices ought to be. If your bank’s overdraft revenue is falling or has not increased in the past several years, then lowering the price is a strategy to consider to reverse the trend.

Semper,

Mike Moebs

(Mike will respond to questions at [email protected])

J.V. Proesel, director of client services at Moebs $ervices, Inc., contributed to this blog.

Learn more about the upcoming webinar, “Optimize Overdraft Revenue: Trend & Tactics,” March 30

* “CBSA” stands for “core-based statistical area,” a federal unit that replaced older terminology, such as “metropolitan statistical area.”

Tagged under Bank Performance, Management, Lines of Business, Blogs, Community Banking, The Prairie Economist, Feature, Feature3,