The darkness side and long honeymoons of token sales

What happens after the “initial coin offering”?

- |

- Written by William Mougayar

- |

- Comments: DISQUS_COMMENTS

Much excitement accompanies the launch of a new cryptocurrency. But eventually, according to blogger William Mougayar, business gravity will take over.

Much excitement accompanies the launch of a new cryptocurrency. But eventually, according to blogger William Mougayar, business gravity will take over.

There is a period between the initial token offering and overall market rollout/acceptance where darkness prevails.

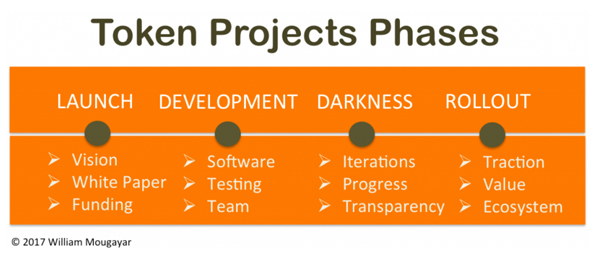

If we look at the lifecycle of a crowdsourced crypto technology project, there are three apparent evolutionary phases:

• Initial launch

• Development

• Market rollout

The Initial Launch steps include explaining the vision, writing a white paper, and obtaining funding via the initial crowd sale offering. In this stage, lots of excitement prevails.

The Development stage is primarily devoted to software development of the technology, protocol and capabilities, team buildout, and early testnet or beta usage.

The Market Rollout focuses on entering the marketplace via user acquisition and growth, ecosystem development, user engagement, and overall market acceptance.

In some cases, software development has already started before the token sale, and there are degrees of readiness and elapsed time ahead of the market rollout.

Shortly after Launch, however, most projects quickly step into a Darkness stage.

When darkness arrives

Darkness relates to the scant amount of transparency that prevails, relating to exactly how they are doing. Outsiders do not really know the precise status of the project, despite transparency attempts.

This prevailing darkness also relates to how the cryptocurrency markets value the company (or speculate on it), as the public tries to interpret progress and evolution from the development stage into the market installation phase, by reading the tea leaves.

Especially in the first year, optimism continues to prevail for most projects, and the market is told what the founders want it to hear, making the darkness appear to be less frightening. Whereas a half-empty glass stance sees this period as darkness, a half-full position would see it as a long honeymoon.

Along the journey to the market rollout, there is an interim step,—a transitional period where early signs of market acceptance and usage begin to appear, but clarity on the product-to-market fit hasn’t necessarily taken hold yet.

The ultimate destination is, of course when the market begins to accept the technology. At least at that stage, users should be able to start extracting value from the product, protocol, application, or technology offering. In essence, we can start seeing a reality unfold, and quantifiable metrics start to emerge that could be correlated to market valuation. It can take a good two years before these real market signals emerge.

From transparency to real valuation metrics

In the traditional venture capital segment, investors are privy to how companies are doing. In the case of these ICO-driven projects, as I’ve stated several times before ("Watch Out, the ICOs Are Coming"), the level and quality of public transparency is varied, and there is a lot of dressing-up going on. [Editor’s note: ICO stands for “Initial Coin Offering”]

I am interested in better understanding the relationship between the speculatory and real intrinsic valuations for these projects.

Of course there is value in the degree of transparency provided, but self-transparency can be incomplete, resulting in subjective interpretations.

In many cases, the markets are giving forward valuations that are based on the speculatory expectation for what the technology can do, or promises to do. But these forward valuations are not squarely related to where the project really is.

So, how do you value these companies, projects, decentralized protocols, applications or technologies?

New performance metrics or old ones?

In traditional venture investing, we are used to relatively well-defined stages: angel; seed; Series A, B, C, D, E, F; then IPO. Each one of these phases has generally accepted stage characteristics pertaining to product evolution (alpha, beta, launch), product-to-market fit, and continued user growth, and resulting market acceptance and share.

In public companies, analysts and investors use metrics such as revenues; net income; EBITDA (earnings before interest, taxes, depreciation and amortization); EPS (earnings per share); P/E ratio (price to earnings ratio); and sales growth in order to correlate market capitalization justifications.

For ICOs and token-based projects, what are the equivalent performance metrics?

In the long term, there is no escaping real metrics, and these are only visible after the market launch stage. Perhaps they will be similar to traditional financial performance metrics, and maybe there will be new ones that emerge.

Ultimately, how do we achieve valuation rationality? What will replace the price to earnings ratio, a key driver to market capitalization values?

Some argue that a decentralized protocol doesn’t need a direct revenue model, because an open protocol is free to use. It is typically driven by an open source community and/or a foundation. However, even non-profit foundations need an operational budget which could come either from donations, or from a percentage of token ownership.

Foundations and ICO projects can theoretically continue selling some of their tokens in order to finance their operations indefinitely, as long as the markets continue to give them healthy valuations, based on the strength of their ecosystem, volume of transactions, or real revenues.

However, it is still unsure whether continuously dipping into the publicly crowdsourced markets to finance operations is a long-term viable approach.

Not all ICOs are created equal, and not all of them are protocols that can live on the strength of an ecosystem around them, let alone the token that gave them birth.

Although all projects have visions of being the next Bitcoin or Ethereum (just as regular startups dream of being the next Google or Facebook), we are seeing many ICOs looking just like applications, marketplace products, or technology solutions. They will need to eventually show real revenues or viable business models in order to strengthen and support the public valuations they will be receiving.

On the positive side, some metrics are starting to emerge.

For example, consider SIA and Storj Labs, both providing decentralized cloud storage services. SIA has stated it will retain 3.5% of contracts revenues, and Storj will be charging users a flat cost for their service. ICONOMI will keep 30% of the fees generated by fund managers that use their platform. In essence, these three companies are implying that they will be eventually profitable, and we will eventually be able to correlate their financial performance to their market valuations.

The above examples can lead to quantifiable metrics, and they will be helpful in proving whether a real business supports the longevity of a project.

I believe we will eventually return to more palpable metrics to guide us in measuring the valuation characteristics for marketplace, product, and applications-based ICOs because they will have revenue expectations.

Protocols are a bit different, and they are still a new beast whose success characteristics may still be unclear. To make things more interesting, not all decentralized applications need a special protocol, and not all protocols necessarily need a special token. Keep in mind that some decentralized applications rely on an underlying protocol that only serves the application itself, which means that the protocol’s market importance could be over-stated.

I’m looking forward to seeing more ICO projects provide increased clarity about the performance metrics expectations they plan to exhibit during their future adult lives, in addition to the assumptive utility of that token they are selling.

Tagged under Technology, Blogs, Blockchain, Business of Blockchains,

Related items

- CRS Report Highlights Regulatory Obstacles for Pension Plans

- How Banks Can Unlock Their Full Potential

- Banking Exchange Interview: Soups Ranjan Founder and CEO of Sardine Discusses AI

- Digital Wallets Account for Half of Online Sales

- Unlocking Digital Excellence: Lessons for Banking from eCommerce Titans