Confronting “the wolf” with ALCO

Rate increases mean different things for each bank. But all must prepare for “wolves”

- |

- Written by ALCO Beat

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

ALCO Beat articles featured exclusively on bankingexchange.com are written by the asset-liability management experts at Darling Consulting Group.

By Keith Reagan, managing director, Darling Consulting Group

“To Cry Wolf.”

This is a commonly accepted phrase meaning to “give a false alarm,” to “ask for assistance when you do not need it,” or to “exaggerate and/or lie.”

The phrase comes from one of Aesop’s fables. A shepherd boy found it amusing to repeatedly trick local villagers into believing wolves were attacking his flock of sheep.

Because of his continual lying, the boy lost the villagers’ trust. Inevitably real wolves appeared and because of the mistrust, no one came to help the boy or his sheep.

In the end, the sheep are eaten. In one interpretation, the boy is eaten.

We have all heard this story in one form or another, likely from our parents growing up. And we’ve retold it to our children. Are there parallels to this story in the banking world today?

The FOMC that cried wolf

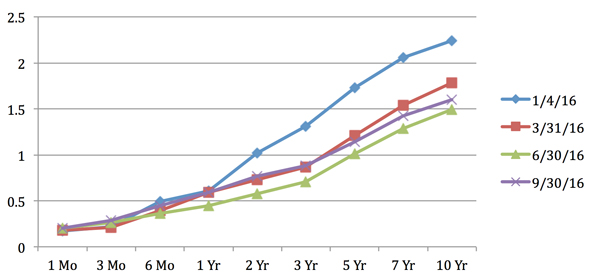

In December 2015, the Federal Open Market Committee increased the Fed funds target rate by 25 basis points, and FOMC minutes suggested that four additional increases in 2016 were imminent.

Only one of those increases occurred, in December 2016. Taking the Fed action out of the equation in 2016, market rates declined. (See graph below.)

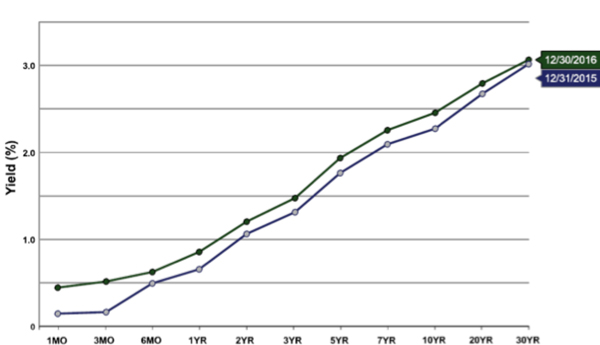

The bond market has sold off since the election, and again FOMC minutes suggest two to three increases are “likely,” yet the yield curve is very close to levels seen this time last year.

So, is the recent sell-off and Fed tightening the start of rising rates? Or is the market crying wolf, again?

Of course, no one knows for sure. However, there seems to be potential for an improving economy and higher interest rates, in both the short and long term.

There is also the possibility for reduced regulatory burden and costs and increased defense and infrastructure spending, as well as lower taxes.

The economy would potentially improve should any or all of these occur, which may lead to higher interest rates.

What impact would a rising rate environment have on your balance sheet? Was one “wolf” (i.e. 25 bps increase) problematic or did it improve earnings? What about 2-3 additional wolves, as the latest minutes seem to suggest?

How many wolves can your bank handle before there is a problem?

For some of you, the wolf in December was enough to cause a problem. For others wolves are a really good thing. At the same time, many fall somewhere in between.

Looking at your wolves

You should run a what-if analysis through your asset/liability model to determine the answer to these questions.

I suggest running increases in short-term market rates (i.e. less than one year) without an increase in managed retail rates to understand the impact of market rate movements. Additional what-if analysis including assumed deposit pricing betas will help complete the picture and serve as a “break-even” analysis.

Market rates are only one piece of the puzzle. Every part of your balance sheet will be impacted differently depending on the amount and timing of rate movements, as well as the eventual shape of the yield curve.

These variables should also be simulated in the asset/liability process. How will the various pieces of your balance sheet react to wolves, and collectively what does that mean to the bottom line?

Investments

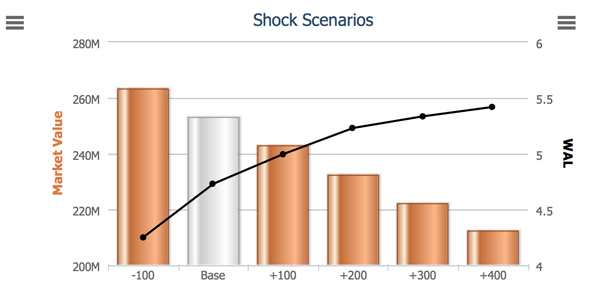

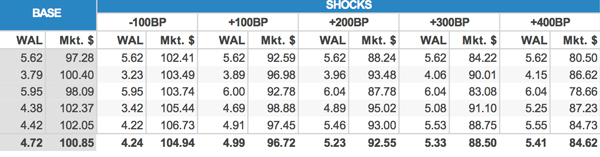

The price volatility within investment portfolios has been a hot button with ALCOs and boards since the post-election sell-off. The inverse relationship between the value of fixed-rate investments and market interest rates is not a new concept. The chart below represents a typical community bank investment portfolio and shows the price and extension impact of different rate environments.

While many banks had unrealized gains evaporate and turn into unrealized losses, what happened to the value of your institution and the banking industry as a whole?

Quite the opposite!

The fact that you have an unrealized loss or gain should not in and of itself change your investment strategy. An investment portfolio serves many important functions on your balance sheet. It provides liquidity, diversity, earnings, and can also serve as a hedge for interest rate risk purposes.

None of these strategic benefits should be trumped by an unrealized value.

Nonetheless, there will be questions about the value and duration of investment portfolios. Be proactive and re-educate everyone about why the investment portfolio has the make-up it has.

Loans

A question I have been asked many, many times since rates have increased is: “Should I continue to put fixed rate loans on my balance sheet?”

Obviously, every bank has a different interest rate risk profile, so there is no “one size fits all” answer.

However, you really need to ask this question: “What would happen to loan volumes if we don’t offer fixed-rate loans in the marketplace?”

Chances are the best loan customers in your market want fixed-rate loans. If you insist that your balance sheet profile no longer supports adding fixed-rate loans, look again. There are other pieces of the balance sheet that can be changed before you should agree to walking away from making loans to the best loan customers. Places to look include: retail deposit strategy, wholesale funds strategy, investment portfolios, adoption of derivatives, and more.

The post-election sell-off has impacted market rates, but have those higher rates translated into higher rates in the pipeline? If not, is competition the likely cause? (Or is it an excuse?).

Educate your customers on what has happened to rates, and why the proposed rate is higher.

Educate your team members so they can have this type of discussion and ensure that there is a consistent message throughout your organization.

Competition is real, and market rates do not instantly translate to higher loan rates. But you need to push. An extra 5-10 basis points on one deal will not impact your bank, but adding 5-10 basis points on overall 2017 loan volume could make or break the budget!

Deposits

Unfortunately, many of you who have not seen material increases in loan rates are experiencing pressure to offer deposit specials and/or increase rates on non-maturity deposits.

There are banks that should be proactive (i.e. playing offense) with specials, given the liquidity and interest rate risk profiles of their balance sheets.

Conversely, there are banks that should be more reactive (i.e. playing defense).

Either strategic approach needs to be fully vetted, understood, and communicated at every level of your institution. And that includes the board.

If the strategy is to offer a new product and/or specials, is it for new money only? (Yes, this can work.)

If not, is the true cost of potential migration (i.e. the marginal cost of funds) fully understood?

I suggest two ways to vet your approach.

First, run stress tests on deposit pricing assumptions through your asset/liability model. Second, stress test cash flow through a comprehensive liquidity model.

Going through both exercises will not only ensure a model’s accuracy, but will also lead to strategic discussion on retail deposit pricing—which of your customers are or are not rate sensitive?—and use of wholesale funding. (Wholesale funding is not a four-letter word. It could play a part in almost every balance sheet).

This type of focused strategic discussion is the backbone of ALCO and will improve your earnings.

Considering rising rates broadly

Whether it has resulted in an unrealized loss in an investment portfolio or discussion of loan pricing or funding strategies, the recent uptick in rates (and potential for more) provides a good opportunity for training and education.

That extra effort should ensure that everyone in your organization is comfortable with the balance sheet position and strategy and has the ability to communicate with customers in a positive way to enhance profitable relationships.

Many banks have used ALCO as a way to train and educate the different levels throughout their organizations. Invite different departments into portions of the meeting, or hold additional meetings to disseminate current balance sheet strategies.

This is not the first article I have written on rising rate preparedness and the importance of strategic focus at ALCO. If recent history holds true, it won’t be the last. (I do feel a bit like the boy who cried wolf).

Nonetheless, ALCO needs to fully understand the impact of wolves arriving at the door. The committee must have a strategic plan to help protect against those wolves and/or benefit from their arrival.

Let ALCO be the fence around your herd, there to protect the bottom line!

About the author

Keith Reagan is a managing director at Darling Consulting Group. He has more than 20 years of experience working directly with community banks, helping them improve their overall performance through proactive management of liquidity, interest rate risk, and capital. He works to develop strategies that best fit the risk/return dynamics of their balance sheets. Reagan has served on the faculty of ABA's Stonier School of Banking, has written many articles for a variety of professional publications, and is the editor of DCG's monthly periodical, the DCG Bulletin.

Tagged under ALCO, Management, Financial Trends, Risk Management, Rate Risk, ALCO Beat, Feature, Feature3,