CRE buildup slows

Fewer banks concentrated in CRE as industry returns to late 2013 growth levels

- |

- Written by S&P Global Market Intelligence

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

S&P Global Market Intelligence, formerly S&P Capital IQ and SNL, is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the SNL subscriber side of S&P Global's website.

By Maria Tor and Venkatesh Iyer, S&P Global Market Intelligence staff writers

As commercial real estate loan growth slows after a boom in 2015 and 2016, fewer banks are concentrated in these loans.

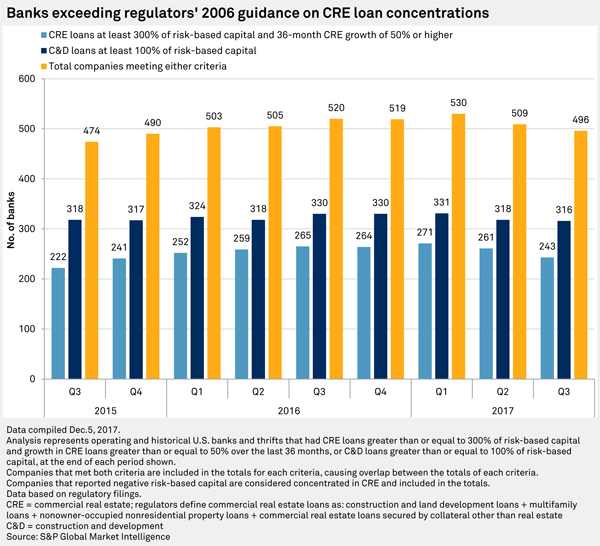

The number of banks concentrated in CRE loans fell to 496 at the end of the third quarter of 2017, from 509 at the end of the second quarter and 520 at the end of the third quarter of 2016. It is the first time that the number of banks concentrated in CRE has been under 500 since the fourth quarter of 2015. (Totals reported in prior articles may not match the totals reported in this article due to the frequency of call report restatements.)

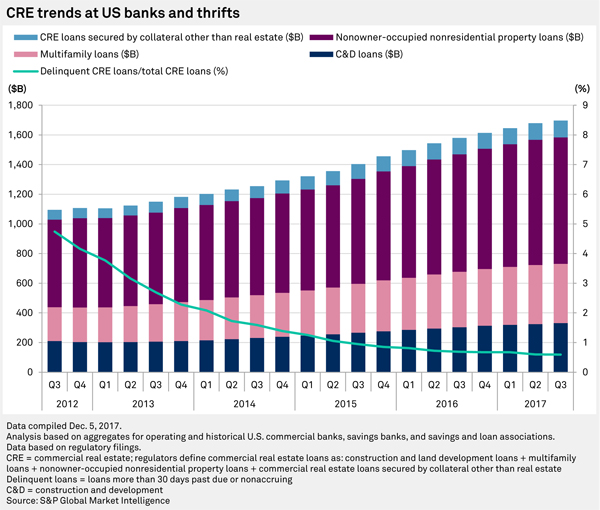

Banks are pulling back on growth in CRE, which is composed of construction and land development loans, nonowner-occupied nonresidential nonfarm loans, multifamily loans, and loans for commercial real estate secured by collateral other than real estate. The year-over-year increase in CRE in the third quarter was down to 7.4%, the lowest growth rate since the fourth quarter of 2013.

Growth was down across all the loan categories that make up CRE. Twelve-month growth in construction and land development as of Sept. 30 was in the single digits for the first time since the second quarter of 2014.

Regulators have guided banks since 2006 that they could be subject to increased regulatory scrutiny if they became concentrated in CRE loans. The banking regulatory agencies reissued their CRE guidance in late 2015 after noting substantial growth in CRE loan types.

The guidance states that banks may be considered concentrated in CRE loans if they meet at least one of two thresholds:

• CRE loans are greater than 300% of risk-based capital, and CRE loans have grown by more than 50% during the prior three years.

• Construction and land development loans are above 100% of risk-based capital.

While the overall delinquency rate of CRE loans remained flat at 0.59% as of the end of the third quarter, the largest category of CRE loans, nonowner-occupied nonresidential properties, saw an uptick in delinquencies during the period to 0.67% from 0.63%.

Sixty-four banks became concentrated in CRE during the quarter, while 78 banks dropped off the list.

The largest banks concentrated in CRE are three New York-area banks: Signature Bank, Investors Bancorp Inc. and Valley National Bancorp. The largest bank to become newly considered concentrated in CRE was Banco Popular North America, also based in New York.

This article originally appeared on S&P Global Market Intelligence’s website on Dec. 13, 2017, under the title, "Fewer banks are concentrated in CRE as loan growth slows to late 2013 levels"

Tagged under Mortgage/CRE, Commercial, Feature, Feature3,

Related items

- Banking Exchange Hosts Expert on Lending Regulatory Compliance

- Merger & Acquisition Round Up: MidFirst Bank, Provident

- FinCEN Underestimates Time Required to File Suspicious Activity Report

- Retirement Planning Creates Discord Among Couples

- Wall Street Looks at Big Bank Earnings, but Regional Banks Tell the Story