Banks sheltering under HTM bucket

SNL Report: Basel, rate picture influences strategies

- |

- Written by SNL Financial

By Nathan Stovall and Salman Aleem Khan, SNL Financial staff writers

Banks continued to build their held-to-maturity investment portfolios considerably in the first quarter, looking for a safe haven from swings in market valuations.

For a larger version, click on the image.

For a larger version, click on the image.

Banks watched unrealized gains in their investment portfolios wash away in 2013, when long-term interest rates rose off historical lows.

Many of the bonds in their portfolios are rate-sensitive assets, often acquired to satisfy regulatory demands for greater liquidity. They came under pressure when rates rose. Changes in the value of banks' available-for-sale, or AFS, portfolios flow through accumulated other comprehensive income, or AOCI, and impact tangible common equity. Many banks have looked to their held-to-maturity, or HTM, portfolios to mitigate that impact.

Banks give up some flexibility when transferring securities out of their AFS portfolios to their HTM portfolios. However, institutions feel comfortable with the credit risk in many securities they own and want to avoid volatility that comes with rising rates. Banks are not required to make mark-to-market adjustments to their HTM buckets on a quarterly basis.

Larger banks have led the way in building their HTM portfolios, classifying many of the liquid securities they have acquired to prepare for new provisions such as the liquidity coverage ratio, or LCR, and the net stable funding ratio, or NSFR, as held-to-maturity.

Larger banks are not only trying to protect those liquid securities from mark-to-market adjustments that could negatively impact tangible common equity, but under the Basel III rules, at the nation's largest institutions, changes in the value of AFS portfolios would also flow through regulatory capital.

Shift in portfolio management

The new rules have banks taking a different approach to investment portfolio management than in the past.

"These are economic decisions that are being made differently than was the case prior to Dodd Frank," F. Greg Hertrich, managing director and head of U.S. Institutional Strategies at Nomura Securities International, told SNL. "You have to hold Level 1 assets. Many banks believe they have to have some assets in HTM and that was simply not the case pre-Dodd Frank."

The majority of banks' securities remain in their AFS portfolios, which are subject to changes to market values. Banks show those changes in values, and whether they have recognized gains or losses, by disclosing the level of unrealized gains and losses in their AFS portfolio every quarter.

As the yield on the 5-year Treasury rose more than 100 basis points in 2013 and the yield on the 10-year Treasury increased more than 125 basis points in the period, the level of unrealized gains in bank portfolios evaporated and, in many cases, changed into unrealized losses.

Long-term rates actually declined in the first quarter, leaving banks' investment portfolios in more favorable positions. However, the prospect of higher rates has some institutions investing cautiously.

Banks have also prepared for increases in rates by moving more and more securities to held-to-maturity, increasing the portfolios by $48.79 billion in the first quarter and by $79.46 billion in the fourth quarter, while AFS portfolios declined by $10.03 billion and $22.06 billion during the same periods, respectively, according to SNL data.

Many of the securities that banks are moving into their HTM portfolios would likely come under pressure if interest rates rose. SNL data show that most of the linked-quarter increase in banks' HTM portfolios came from the addition of Treasuries, municipal bonds, and residential mortgage-backed securities in the first quarter.

A number of those bonds were purchased to satisfy regulators' demands and often can come with lower yields than other alternative investment strategies. In the event that rates rise, those securities will not be subject to changes in market valuations. But banks will have to keep the lower-yielding assets on their books and that could put pressure on margins as deposit costs will likely rise from 10-year lows.

"I think the potential for tighter margins across the board and ultimately lower shareholder returns is driven by decisions like this that are made in conjunction with new regulations that frankly require banks to maintain much more stable balance sheets and simultaneously be much more liquid and much more highly capitalized," Hertrich said.

For a larger version, click on the image.

For a larger version, click on the image.

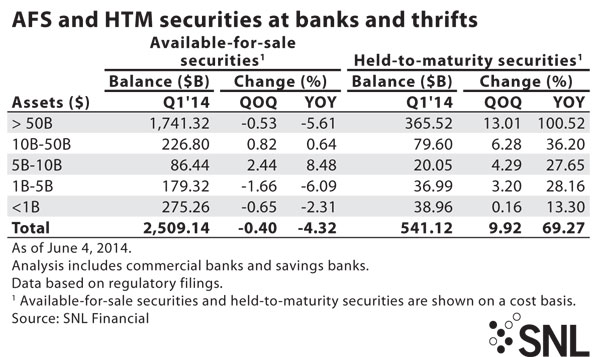

Banks with more than $50 billion in assets have relied on the held-to-maturity classification the most, increasing their HTM portfolios in the first quarter by 13.01% from the linked quarter and 100.52% from a year earlier. Some of those banks have acted in response to regulatory changes as they have sought to protect assets acquired for certain liquidity measures from changes in market valuations.

Impact of Basel III deliberations

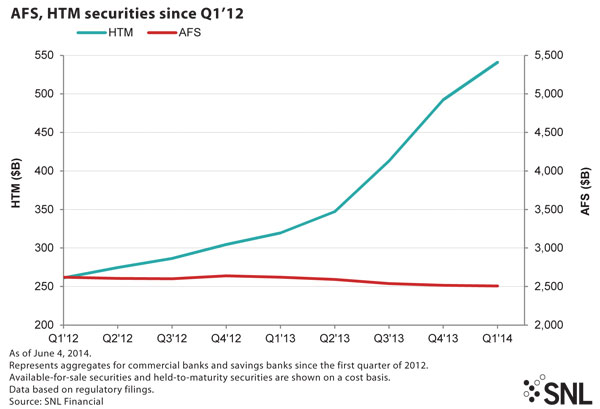

Banks have also reacted to the originally proposed Basel III rules, which required AOCI to flow through regulatory capital. SNL has found that the inclusion of AOCI in regulatory capital would have caused volatility in banks' regulatory capital ratios, and institutions have ramped up transfers of securities to HTM portfolios significantly since the provision was first proposed in the summer of 2012. Since the second quarter of 2012, HTM portfolios have risen by $266.28 billion, or 96.9%, according to SNL data. AFS portfolios, meanwhile, have actually declined by $98.10 billion, or 3.8%, during the same period.

The final Basel III rules will require AOCI to flow through regulatory capital at institutions with more than $250 billion in assets, while smaller banks will have the opportunity to make a one-time election to not include most elements of AOCI in regulatory capital.

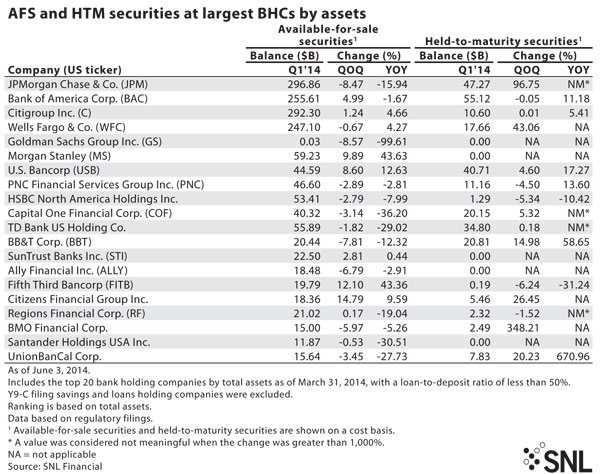

Some banks that cannot opt out of the AOCI provision have actively increased their HTM portfolios over the last two quarters. For instance, JPMorgan Chase & Co., moved close to $23.2 billion in securities to held-to-maturity in the period, building on the $19.5 billion in securities it added in its HTM bucket in the prior quarter.

Small banks also lean on HTM

Still, smaller banks that will not be subject to certain Basel III provisions such as the LCR or AOCI provision have also relied on their HTM buckets more in recent quarters.

SNL data shows that banks with between $10 billion and $50 billion in assets increased the size of their HTM portfolios in the first quarter by 6.28% from the linked quarter, building on the 12.22% quarter-over-quarter increase in HTM portfolios those institutions reported in the fourth quarter.

More than a handful of smaller institutions have said they prefer to hold bonds in HTM portfolios opposed to their AFS portfolios to avoid the negative impact that rising rates would have on their tangible common equity ratios.

Tagged under ALCO, Management, Financial Trends, Feature,