Multichannel Banking 2.0—Customer Ecosystems

- |

- Written by Manish Grover

By Manish Grover, program director with MindTree's Enterprise Solutions and Consulting Group.

Investments in multichannel banking have been focusing on traditional and commonly known media such as mobile, web, branches, paper, email, and ATMs. These strategies have no doubt brought tremendous advances in customer experience, operating cost synergies, and marketing effectiveness. However, with recent industry evolution, the definition of channels is changing.

Previously, largely ignored in the integrated multichannel marketing strategy, aspects such as cross-industry partnerships (retail, nonprofits, airlines, etc.) and changing payments landscape (mobile, web, intermediaries, etc.) present significant opportunities. These trends must be viewed from the perspective of a "Customer Ecosystem" in order to survive. How should financial services organizations alter their investment strategies to attract and retain a relevant audience that can drive the core business?

The answer is in the question: relevance, context, and interactivity. Not only do consumers need a seamless experience across traditional channels, but moments of truth in their transactional patterns must be met head on.

In this article, we examine the tools that will help realize the vision of relevance, context, and interactivity.

Understanding the Banking Needs and Information Framework

This framework measures the potential of customer engagement by classifying the needs and content strategy from an industry characteristics perspective. On the high end of the spectrum lies inherently relationship-based industries such as financial services (consumer banking, insurance, and cards). On the other end are industries such as packaged goods that must work much harder to achieve deeper and persistent customer interaction. The underlying rationale is that industries with a higher index have a customer relationship created by default (e.g. an account). This initial relationship can then be cultivated for improving customer life time value. Companies with a lower index rely on brand awareness, promotions, and emotional connections to receive preferential share of mind. In this model it is also evident that promotional strategies are influenced by the positioning on the customer interaction spectrum.

With this underlying hypothesis that banking enjoys a high customer interaction index, what steps can be taken to enhance the interaction in order to maximize customer engagement and hence acquisition, development and retention?

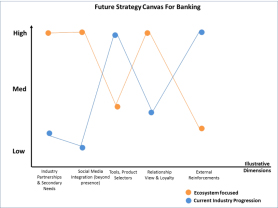

Developing the Multichannel Strategy Map

This simple yet powerful tool forces an exploration of components (horizontal axis) and highlights gaps in traditional wisdom when seen in the context of emerging market trends. While generating insights into competitive differentiators, the tool helps zoom into the offerings which are most impactful for the future.

| Fig1: Illustrative strategy map | |

As we examine the emerging customer ecosystem in this light, the primary difference lies not in the inherent capabilities on the horizontal axes but in how these capabilities are cultivated and evolve over time. For example, external tools and product selectors will still be needed but in the context of customer relationships and context. Similarly, industry partnerships will evolve to harmonize and tailor promotions and offers. To maximize relevance, context, and interactivity, the capabilities needed for an ecosystem should be developed along the following three major dimensions of an emerging ecosystem:

Integration of industry partnerships

Business is not just about retail, banking, or travel anymore. Banks partner with online retailers and travel sites to boost spending and engagement. Similarly supermarkets position their online or mobile presence primarily for information. But supermarket touch points can easily be leveraged by banks with spending on specialty foods, fitness providers, and fulfillment services to tie in more deeply with a consumer's current and desired lifestyle.

With a high customer interaction index, banks are positioned strongly to mutually develop the customer relationships other industries are aspiring for. In the end, partnerships must be seen as tools to develop a customer's ecosystem if they are to really impact the banking business drivers. Customized pricing and service tiers, promotional strategies by suppliers, targeted offerings based on consumer preferences, as well as an appreciation of the customers' existing offline relationships are methods that are yet to be developed fully in the context of partnerships.

Cross-product and cross-business leverage

Customer views must be unified to serve the scope of inbound and outbound marketing, service and operational processes. The current maturity along this dimension can be evaluated by the isolated manner in which offerings and benefits are positioned to customers in addition to limited relationship advantages that are presented. The existence of multiple relationships has empirically yielded higher wallet and mind share. The focus of the future is in packaging and presenting offerings that can then be evaluated and considered together for selection.

This traditional dimension, when viewed in terms of the customer ecosystem, opens up new possibilities where the entire gamut of customers' interests are at play, not just credit cards, checking accounts, loans, and mortgages.

Optimizing customer touch-points

While maturity for this dimension starts with integrating customer experience across channels (e.g. offline offers sent by paper being seen online and by the contact center for follow up), progressively higher levels of maturity move into localizing dialog on the customers' preferred channels and the usage scenarios within the channels. This can be analyzed by examining the process of self-selection that a customer would go through if the constraints were removed. For example, must a customer download retail coupons from a website or can they access them on their mobile phone? Must they then download a separate app for these coupons or use existing apps that customers already use?

As we ponder these questions, it is apparent that channel selection is as much a matter of constraints as it is of possibilities. The factors that define a customers' preferred channel and their usage within channels will be seen as more internally driven that they may be customer driven.

For industries on the higher end of the interaction index spectrum such as banking, the inherent trust in the relationship provides key advantages in establishing persistent and deep interaction. Typical tools which can be successfully leveraged include user communities and partnerships with high index firms such as retailers and banks. In addition, partnerships with lower index firms such as packaged goods companies (beverages, food, etc.) further broaden the horizon mutually. For example, users may not register on the Gerber Foods website for offers and advice, but they may welcome an offer to sign up for deals that come through their credit card's account or are available in their online mall's shopping cart, ready to be redeemed and shipped.

Assessing and Planning for Risks

Even as steps are taken towards defining a robust customer ecosystem strategy, various risks must be assessed and mitigated. The strategic risks will generally arise in the form of regulatory, customer privacy, and technology security aspects. In addition, with the customer relationship strategy straddling industries and companies, managing a singular customer, identifying and defining business rules for communications, offers, and data sharing will become imperative. A top-down view of the long term implementation roadmap must be developed before embarking on individual initiatives. Efficient technology and process integration emerge as the critical success factors. Given organizational alignments and process harmonization complexities, quick wins will be important to define and realize. Finally, a coherent strategy for harnessing data towards customer, offerings, and operational analytics will be important.

Summary

The critical success factors for initiating and sustaining an ecosystem are the three dimensions of offerings integration, industry partnerships, and channel optimization supported by aligned technology, integrated processes, and timely business intelligence. But the most critical success factor is the ability to look as a company, at the company, from a customer's perspective. And that means championing the cause at all levels and driving home the potentially dire implications of the emerging marketplace trends. The ecosystem approach is the required way of the future if companies are to maintain a front runner position in the value chain, or even exist. Examples of companies that dragged their feet are all around us today and have felt the impact within a few short years. The sooner we champion the cause as one company and evaluate the necessary partnerships to harness the emerging ecosystems, the better value we can drive for our customers and our shareholders.

About the author:

Manish Grover focuses on new digital business and marketing paradigms, leveraging social media, mobile, analytics and functional integration to improve customer engagement, profitability, and brand positioning.