Regulatory limits on CRE lending need a re-think

Spotlight on quantity should shift to quality

- |

- Written by Dennis Gibney, managing director FinPro, Inc.

Community bankers across the country dread the thought of their next regulatory exam and the new rules, both written and unwritten, that will be applied by examiners. Many banking executives wonder whether the business model still works at their bank’s asset size. Traditional profit centers are being squeezed, including commercial real estate (“CRE”) lending.

While some in the industry look at these factors with dread, FinPro believes that the community banking sector remains viable. However, proactive steps need to be taken to demonstrate management’s knowledge and control of credit quality in order to moderate the impact of the more stringent examinations. Later in this article, some thoughts and ideas about improving credit data tracking and reporting will be provided.

Regulators don’t have CRE numbers goal right

The published regulatory limitations on commercial real estate lending are not warranted, based upon the current delinquency and loss severity levels. The focus should be on loan quality, rather than dollar volumes by loan type. However, to facilitate this focus on quality rather than quantity, notably at the bank level, additional data retention and reporting by banks is necessary.

CRE loans are an important profit center for the banking industry, with over $1.2 trillion in outstanding CRE loans on banks’ balance sheets as of Sept. 30, 2010. The Interagency Guidance based upon capital limits the portfolio size as a percentage of assets. Assuming 10% risk-based capital, the CRE portfolio is limited to 30% of assets. This would require that 70% of assets be invested in: residential loans, consumer loans, commercial and industrial loans, securities, and cash.

Community banks do not have the experience or infrastructure to be an expert in all lending categories. Therefore, the unintended consequences will likely include the following: reduction of available credit; entry of new lending lines without adequate expertise or infrastructure; and/or acceleration of the consolidation of community banking industry.

Let’s consider the regulatory guidance I referred to a moment ago in more detail. In December 2006, the federal regulators issued their final guidance on concentrations of commercial real estate lending and sound risk management process. This regulatory guidance provided the following supervisory criteria, beyond which the bank’s holdings became of greater concern and required enhanced risk-management practices—or a shrinking down to get back below :

• Total reported loans for construction, land development, and other land represent 100% or more of the institution’s total capital; or

• Total commercial real estate loans (as defined in the guidance) represent 300% or more of the institution's total capital, and the outstanding balance of the institution's CRE loan portfolio has increased 50% or more during the prior 36 months.

While this supervisory criteria was intended to be guidance, many examiners have been implementing the limitation as a “bright line in the sand.” Additionally, in some instances the 50% growth trigger for the 300% CRE limitation has been ignored.

The published regulatory limitations on commercial real estate lending are not warranted, based upon the current delinquency and loss severity levels. The focus should be on loan quality, rather than dollar volumes by loan type. However, to facilitate this focus on quality rather than quantity, notably at the bank level, additional data retention and reporting by banks is necessary.

CRE loans are an important profit center for the banking industry, with over $1.2 trillion in outstanding CRE loans on banks’ balance sheets as of Sept. 30, 2010. The Interagency Guidance based upon capital limits the portfolio size as a percentage of assets. Assuming 10% risk-based capital, the CRE portfolio is limited to 30% of assets. This would require that 70% of assets be invested in: residential loans, consumer loans, commercial and industrial loans, securities, and cash.

Community banks do not have the experience or infrastructure to be an expert in all lending categories. Therefore, the unintended consequences will likely include the following: reduction of available credit; entry of new lending lines without adequate expertise or infrastructure; and/or acceleration of the consolidation of community banking industry.

Let’s consider the regulatory guidance I referred to a moment ago in more detail. In December 2006, the federal regulators issued their final guidance on concentrations of commercial real estate lending and sound risk management process. This regulatory guidance provided the following supervisory criteria, beyond which the bank’s holdings became of greater concern and required enhanced risk-management practices—or a shrinking down to get back below :

• Total reported loans for construction, land development, and other land represent 100% or more of the institution’s total capital; or

• Total commercial real estate loans (as defined in the guidance) represent 300% or more of the institution's total capital, and the outstanding balance of the institution's CRE loan portfolio has increased 50% or more during the prior 36 months.

While this supervisory criteria was intended to be guidance, many examiners have been implementing the limitation as a “bright line in the sand.” Additionally, in some instances the 50% growth trigger for the 300% CRE limitation has been ignored.

A deeper look at what the numbers say

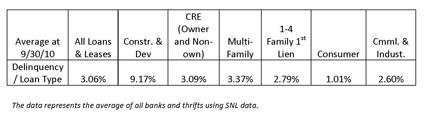

The following table illustrates the average delinquency (90+ days past due and nonaccrual) rates by loan type for all banks and thrifts as provided by regulatory call and thrift financial reports at Sept. 30, 2010. Commercial real estate loan types are generally performing in line with the delinquency level for all loans. However, construction loans have substantially higher levels of delinquency.

The data represents the average of all banks and thrifts using SNL data.

For a larger PDF of this table, click here

The following table illustrates the average delinquency (90+ days past due and nonaccrual) rates by loan type for all banks and thrifts as provided by regulatory call and thrift financial reports at Sept. 30, 2010. Commercial real estate loan types are generally performing in line with the delinquency level for all loans. However, construction loans have substantially higher levels of delinquency.

The data represents the average of all banks and thrifts using SNL data.

For a larger PDF of this table, click here

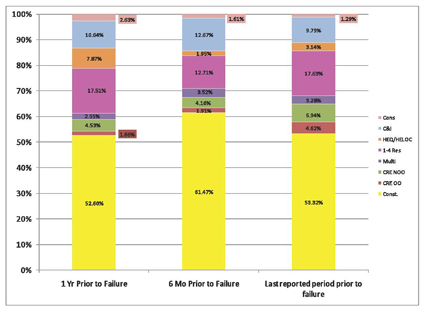

Furthermore, FinPro examined the charge-off levels by loan type for all institutions that failed between Jan. 1, 2009, and Sept. 30, 2010. While failed banks did experience some losses on commercial real estate loans, the loss levels are dwarfed by the losses on construction loans and 1-4 family mortgages.

For a larger PDF of this chart, click here

FinPro also believes that the delinquency and loss levels on CRE are skewed upward as many speculative commercial construction projections are rolled into permanent loans. These loans are then included in the CRE category once the construction phase of the project is complete but the property is not occupied and the loan is termed out.

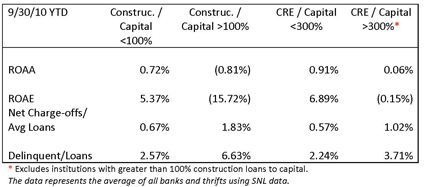

The following table segments the financial performance and conditions for banks and thrifts at, or for, the nine months ended Sept. 30, 2010. This table clearly illustrates that financial condition and performance are materially worse for institutions that exceeded the 100% construction threshold, while those institutions that exceeded the 300% CRE threshold have weaker earnings and higher problem assets, but to a much lesser extent.

* Excludes institutions with greater than 100% construction loans to capital. The data represents the average of all banks and thrifts using SNL data.

For a larger PDF of this table, click here

Putting blame where the credit is overdue

While CRE has not been the largest contributor to asset quality problems, some institutions do have problem CRE portfolios. FinPro believes that the asset quality problems result from poor underwriting, rather than sheer dollar volume of CRE loans. Therefore, the focus should be on loan quality and the volume of weak credits.

In order to facilitate the loan quality focus, financial institutions need to improve data retention and reporting. Data elements that should be tracked in a centralized system include: real estate appraised value, date of last appraisal, debt service coverage, average rental amount, largest rental amount, loan to one borrower, geographic proximity to the bank’s market, property type, etc.

By tracking these data elements on a centralized system, community banks can effectively track and stress test collateral values and debt service coverage ratios. This will enable institutions to more easily demonstrate their knowledge and control of credit quality and address regulatory and investor concerns. By proactively analyzing this data, institutions have the ability to establish their own guidelines before the guidelines are dictated by their regulators.

In summary, not all CRE loans are created equal. The regulatory limitations on CRE loans appear unjustified based upon credit performance, while the limitations on construction loans appear prudent. In some instances, application of the guidance by regulators appears overzealous and has adversely impacted credit to the real estate market. FinPro urges a re-examination of the 300% CRE limitation and a regulatory focus on loan quality, rather than dollar volume by loan type. In order to accomplish this focus on loan quality, financial institutions need to improve data tracking and reporting of credit quality.

About the author:

Dennis Gibney, managing partner at FinPro, Inc., in Liberty Corner, N.J., is an expert in capital markets engagements including mergers and acquisitions, stock valuations, and fairness opinions. He is a CFA Charterholder and a member of the New York Society of Security Analysts. FinPro professionals are frequent contributors to Banking Exchange.

Dennis Gibney, managing partner at FinPro, Inc., in Liberty Corner, N.J., is an expert in capital markets engagements including mergers and acquisitions, stock valuations, and fairness opinions. He is a CFA Charterholder and a member of the New York Society of Security Analysts. FinPro professionals are frequent contributors to Banking Exchange.

Bankers: Share your CRE examination experiences below. Have you tried an approach such as FinPro’s with your exam team? How did it go?

Tagged under Mergers Acquisitions; Lines of Business; Big Data;

Related items

- UBS Expands US Banking Push for Affluent Wealth Clients

- Why most European challenger banks fail in the US — and where the real opportunity lies

- Securitize Set for NYSE Debut Following SPAC Merger Approval

- Colony Bankcorp Agrees $163m First Reliance Deal

- Cross River and Fireblocks Discuss How to Build and Scale Products