Deposit questions going into next year

SNL Report: SOD report shows deposits growing, but rate hike could play a role in 2016

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Ken McCarthy and Tahir Ali, SNL Financial staff writers

Bank industry deposits continued to climb during the 12 months ended June 30, but a looming interest rate hike could hamper that trend.

The FDIC's annual Summary of Deposits included data from July 1, 2014, through June 30, 2015. Deposits grew substantially during that period, rising to nearly $10.66 trillion from about $10.11 trillion a year earlier.

But many industry observers expect interest rates to finally begin to rise at the end of 2015. Keefe Bruyette & Woods is forecasting the first rate hike in December with a gradual increase through 2016. Thirteen participants in the most recent FOMC meeting believe the first increase in the target range for the federal funds rate should be in 2015, while three said 2016 is the more appropriate time.

What’s around the corner?

The long-awaited rate increase will likely lead to a slowdown in the pace of deposit growth but not cause significant contraction—at least not in the short term, according to Keefe Bruyette & Woods analyst Damon DelMonte. He told SNL there is a lot of excess liquidity on balance sheets, and the expectation of "lower rates for longer" is likely to keep deposits at banks.

As rates rise, banks are likely to see increased competition on products such as CDs. "I think you may have some aggressive pricing by internet-based banks," DelMonte said.

On the retail side, there will likely be some shifting between deposit types as customers become more sensitive to rates. But there is unlikely to be a large outflow headed into the stock market or other places. "Banks will try to protect the deposits that they have, and they may end up having to pay up a little bit in rates," DelMonte said.

Click to Enlarge

Click to Enlarge

Trends among the largest

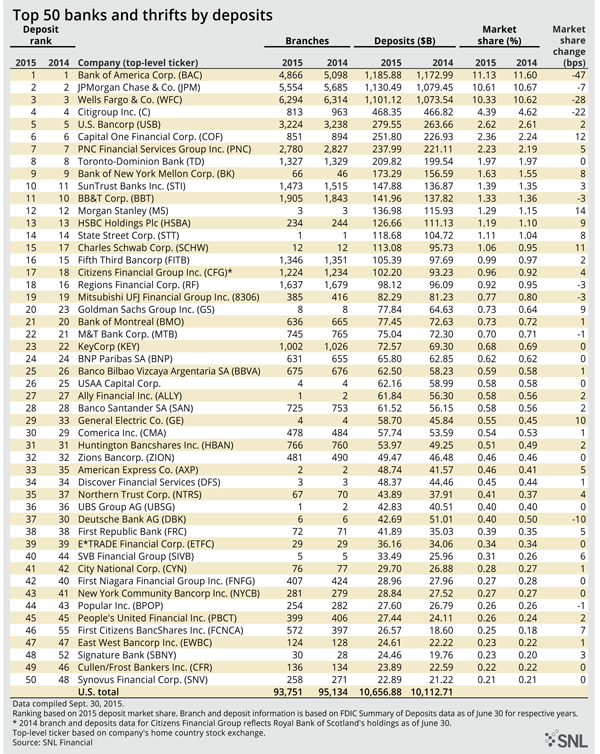

In terms of deposit market share, the nation's four largest banks all took a step back in the past 12 months. Bank of America Corp.'s share of the national market dropped 47 basis points and Wells Fargo & Co.'s declined by 28 basis points. On the flip side, Morgan Stanley's national market share rose 14 basis points and Capital One Financial Corp.'s increased 12 basis points.

Bank of America again had the most deposits in the nation, at $1.186 trillion. JPMorgan Chase & Co.'s deposits climbed to $1.130 trillion and Wells Fargo's totaled $1.101 trillion.

Speaking during a recent conference, Wells Fargo CFO John Shrewsberry said deposit growth has remained strong during the past five years. Average deposits were up 8% in the second quarter, and the bank managed to reduce average deposit costs to 8 basis points, which was 2 basis points lower compared to a year ago and down 20 basis points from five years ago. Shrewsberry said the deposit growth reflects Wells Fargo's success in growing checking accounts as primary consumer accounts were up 5.6% from a year earlier.

Stephens Inc. analyst Matt Olney said that a move in rates could impact the growth in deposits that sprung up in the low interest rate environment.

"If it's just one movement between now and next year then I'm not sure how much that's going to slow it, but obviously there has been a tailwind there for a number of years and that's going to slow at some point," he told SNL.

Olney said savings accounts in particular could be vulnerable in a higher rate environment as depositors seek better rates elsewhere.

Enlarge Image.

Enlarge Image.

Deposits and branch strategies

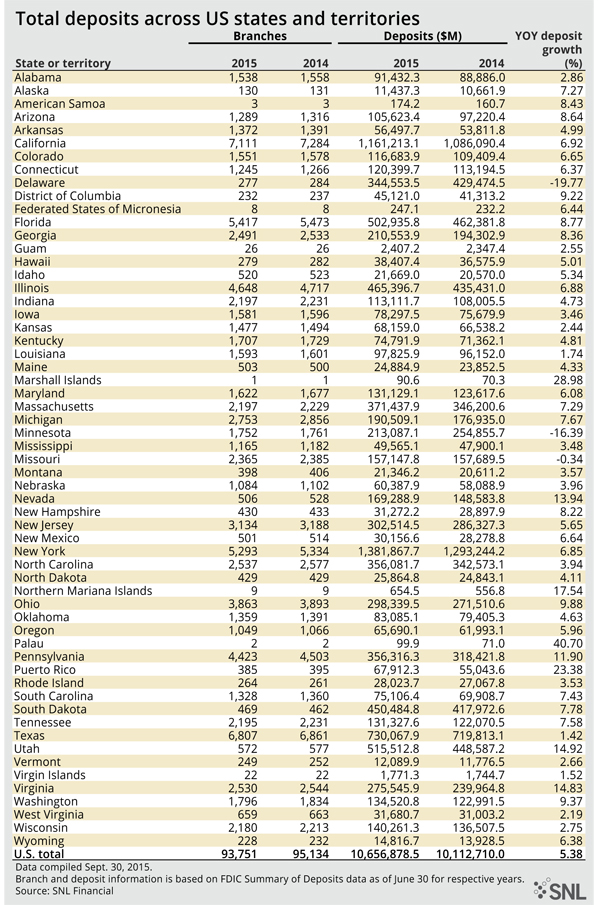

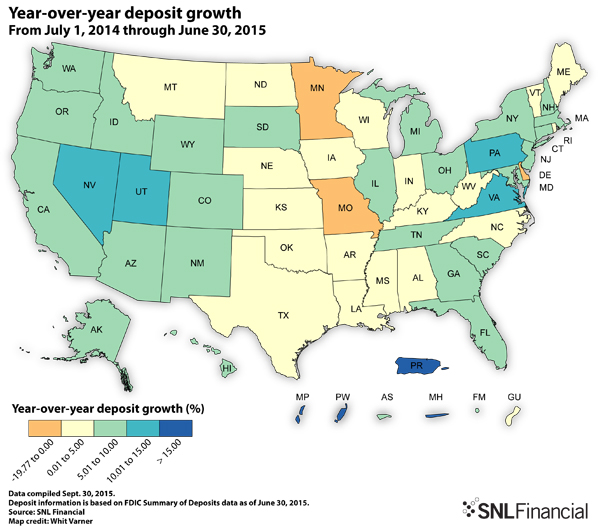

Broken down by geography, 47 out of 50 states posted year-over-year gains in total deposits. The data also highlighted the continued shrinking of banks' branch networks. There were 93,751 U.S. branches at June 30, down from 95,134 a year earlier; these numbers have been adjusted to incorporate SNL data on banks that do not file SOD data.

But DelMonte noted that branches will always have some place in the U.S. banking landscape. He said the decline in branches will be an ongoing process as banks move more into mobile and online offerings while also looking to address their expense structures.

"There's a cost of running a physical branch but there's also a cost of not having a physical branch," DelMonte said. "It's important and you have to find the right balance."

On Sept. 30, Springfield, Mo.-based Great Southern Bancorp Inc. announced plans to acquire 12 branches and related deposits and loans in the St. Louis area from Cincinnati-based Fifth Third Bancorp. DelMonte said that deal is a good example of the branch dynamic often seen today.

Great Southern already had several branches in the St. Louis market, and the deal will double its deposit market share there. Fifth Third, meanwhile, is pulling its retail operations out of the market while keeping the commercial lenders in place. "So you can make the argument for each company as to why they are doing it," DelMonte said. "Some people are going to want to get rid of branches and others will be there to take them off their hands."

Olney said the overall industry branch count will continue to decline but added that some banks are hesitant to get overly aggressive with branch closures due to the looming rate hike. "These bank CEOs have long memories of higher rates and how important these deposits are with higher rates," he said.

Enlarge Image.

Enlarge Image.

This article originally appeared on SNL Financial’s website under the title, “SOD report shows deposits growing, but rate hike could play a role in 2016.”

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- UBS Expands US Banking Push for Affluent Wealth Clients

- Securitize Set for NYSE Debut Following SPAC Merger Approval

- Colony Bankcorp Agrees $163m First Reliance Deal