Will online opening secure millennials?

Looking at assumption that opening accounts via web will lock in tomorrow’s customer today

- |

- Written by Achim Griesel, Haberfeld Associates

Is opening accounts online going to make or break your bank’s foothold with the next generation?

Let’s examine the basic premise first, and then the methodology.

Chasing millennials

There are two sides to attracting a younger customer segment.

On one side most of the deposits and financial needs sit with older customers groups. On the other side, banks must not ignore that they need to engage with younger customers to position themselves for the future.

In a recent article I read about the “talent” gap at community banks. The author started out by sharing a community bank CEO’s analysis of his leadership team—nobody was under 40. The CEO ultimately came to the conclusion that he had to attract younger talent, or position the bank to be sold. Isn’t the same true for your customer base?

At industry conferences marketers and new fintech start-ups constantly remind us that we cannot ignore millennials when building profitable and sustainable financial institutions for the future. But this is not so much about millennials; it is more about the digitalization of banks’ customer base.

Millennials are on the forefront of this, and if we look at the millennials’ utilization of digital channels it was at the same point for them a few years back as it is today for Gen X or Gen Y customers.

In other words, older customers adopt digital channel usage as well, they are just a few years behind.

Migration to online relationships

In the banking industry customers have shifted from utilizing branches to utilizing digital channels. This is not only true for large banks, it also holds true for community banks as shown in the statistics below.

In 2008 our firm started tracking digital channel adoption among the customers of our clients—100+ community-based financial institutions ranging from $100 million in assets to over $20 billion. Here is what we found for that year:

• Mobile banking—non-existent

• eStatement penetration—8.45% of checking account households

• Debit card usage—46.75% of checking customers

• Interchange income (net)—$26.51 per checking account

• Bill pay penetration—9.23% of checking customers

Now, fast-forward to 2015:

• Mobile banking—16.04%

• eStatement penetration—28.06% of checking account households, with top performing community financial institutions at almost 40%

• Debit card usage—52.17% of checking customers

• Interchange income (net)—$46.34 per checking account with top performers at $56.88

• Bill pay penetration—17.43% of checking customers

There is no question digital channels have become an integral part of the banking industry. In today’s environment, it would be hard to imagine a relationship with your primary financial institution without these channels.

However, the fact that customers are transitioning transactions to digital channels can guide bankers down the wrong path in customer acquisition. If customers, younger or older customers, prefer digital channels is the digital channel also the right one to focus on for acquiring new core customer relationships?

Customer acquisition: Online versus traditional

For several years, we have tracked traditional and online checking account openings at over 15 financial institutions ranging from $200 million in assets to over $5 billion in assets. All of these institutions consider customer acquisition a strategic priority. They cover rural, suburban, and metropolitan markets. They invest marketing dollars into traditional marketing in branches and through direct mail, as well as digital channels. Most of them are active in social media.

During the study participating FIs opened 340,384 core consumer relationships in the form of checking accounts, which equals approximately 350 per branch per year. From that larger number, 8,874 of these were opened online—2.6%.

Let’s look at the most recent figures.

• New primary financial institution relationships (checking accounts) in the first six months of 2015

The financial institutions in this case study opened 50,188 new checking accounts in that period, of which 1,989, or 4.13%, were opened online. On average they opened 105 online accounts, which would result in a run-rate of 210 per year. On average 37.7% of online account openings were attracted though a traditional marketing channel.

Over the same six months these organizations opened 185 new core checking relationships per branch.

Thus, any average performing branch at these institutions has generated almost twice the new core relationships that their online openings have generated. Interestingly, this ratio has stayed fairly consistent throughout the last few years.

The numbers above and the customer characteristics below are based on customers that went through the actual account opening process online, not on customers that researched the institution online and then opened an account in a branch.

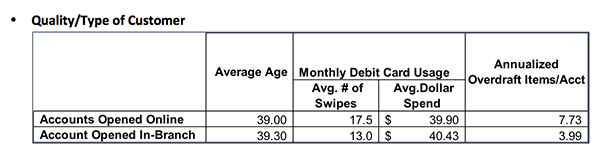

• Quality/type of customer

The average age of the new customer attracted from both channels is almost identical.

• The online-acquired customer swipes their card an average of 17.5 times per month, compared to 13 times per month for the customer that opens their account at the branch—a 35% higher frequency for the online customer.

• Both segments spend $40 per average debit card swipe.

• The online-acquired customer has a significantly higher number of overdrafts per year. At an annual figure of 7.73 for the online customer vs. 3.99 for the customer that opened their account at the branch, it almost doubles.

While there are positive trends on fee-revenue opportunities, the outlook is not as good when it comes to balances, share-of-wallet, and customer retention.

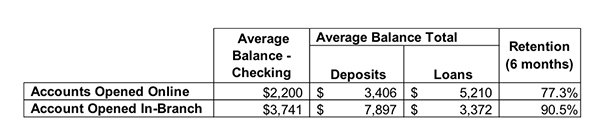

Customers that opened their account online have significantly lower balances—41% lower checking deposits and 57% lower household deposits.

On the flipside, they have higher loan balances, but still relatively small amounts.

Lastly, and probably most critically, attrition for customers that opened their accounts online is twice as high. Considering that acquisition cost for a new core relationship can eat up most of the first-year profit from these customers, retention is a very important measurement.

Where does that leave you?

Don’t get confused. There is a difference between the urgency to offer online openings versus customer preferences for digital channel usage.

While digital channel usage may still be more prominent at large financial institutions, it also has dramatically increased for community financial institutions–and it won’t stop there. Mobile banking, remote deposit products, and apps for product usage will continue to rise in popularity. Being able to compete in these product areas with larger organizations will be critical for core customer acquisition and retention as well as the overall customer experience.

But don’t confuse this with online account opening as a key to core customer growth.

Opening checking accounts online is not wrong. But it is not the answer to the industry’s desire to get more tech-savvy and younger customers. Be aware that you will likely get a more transitional and fee-based customer, and that it will almost certainly fail to materially drive new customer growth for your organization.

And don’t ignore your branches.

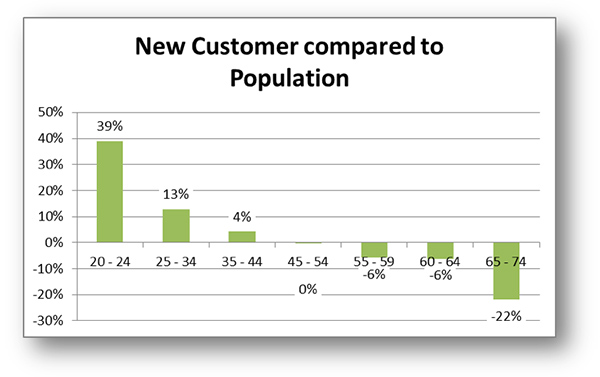

The majority of community bank customers still want to start their banking relationship in the branch, we find. A focused core customer acquisition strategy incorporating your branch and your people will actually attract an outsized proportion of the younger generation. For example, the percentage of new core customers from the age group that is 20-24 years old is 39% higher than the percentage of the population that group represents.

For the foreseeable future the branch, your people, your core products, and your policies will have a lot more impact on your success in acquiring millennials or core customers in general than opening accounts online.

About the author

Achim Griesel is Chief Operating Officer at Haberfeld Associates. Haberfeld provides consulting, marketing, and training services for community financial institutions. Griesel can be reached at [email protected].

Tagged under Retail Banking, Customers, Feature, Feature3,