Locking up longer-term bucks

SNL Report: Some banks running CD specials, while LCR banks build term funding

- |

- Written by SNL Financial

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

SNL Financial is the premier provider of breaking news, financial data, and expert analysis on business sectors critical to the global economy. This article originally appeared on the subscriber side of SNL Financial's website.

By Nathan Stovall and Zuhaib Gull, SNL Financial staff writers

Some banks are building term funding and offering higher rates on CDs in hopes of locking in lower cost funds before short-term rates rise further.

The Federal Reserve finally increased short-term rates in mid-December 2015, and more hikes are expected later this year. Prepping for a potential turn in the rate cycle, some institutions took actions in the third quarter of 2015 to build term funding and marketed CDs to their customers while costs remained low.

CD role on today’s balance sheets

Even with those efforts, CDs remained a relatively small portion of banks' deposit bases, representing 13.5% of total industry deposits at Sept. 30, 2015. This was down from 14.2% at year-end 2014, according to SNL data. Those balances exclude several hundred institutions that hold bank charters but do not principally engage in banking activities, among them industrial banks, nondepository trusts and cooperative banks.

However, larger banks, the price setters in the industry, have begun to increase the relatively small concentrations of CDs on their balance sheets. Some of those institutions have grown CDs modestly in the past quarter, possibly responding to the regulations such as the liquidity coverage ratio, or LCR, which places greater value on retail deposits.

The LCR applies to banks with more than $50 billion in assets, while institutions with more than $250 billion in assets are subject to a more stringent provision. Both groups essentially need to hold "high quality liquid assets" nearly equaling or exceeding projected cash outflows minus their inflows during a 30-calendar-day stressed scenario. At banks with more than $250 billion in assets, FDIC-insured deposits are assigned a 3% outflow rate under the LCR, while noninsured deposits, including corporate deposits, receive outflow rates of 10% to 40%. Those two categories of deposits will receive outflow rates of 2.1% and between 7% and 28%, respectively, at banks subject to the less stringent LCR.

Banks with more than $250 billion in assets have grown CDs the most among the larger banks. Those institutions, which held 48.6% of overall deposits in the industry at the end of the third quarter, increased CDs to a median of 5.4% of their deposits from 4.5% at year-end 2014.

Those institutions seem focused on growing their retail CDs in particular, increasing those accounts to a median of 3.3% of their deposits by the end of the third quarter from 2.6% at year-end 2014. Jumbo CDs at banks with more than $250 billion in assets climbed to a median of 2.1% of deposits at the end of the third quarter from 1.9% at year-end 2014.

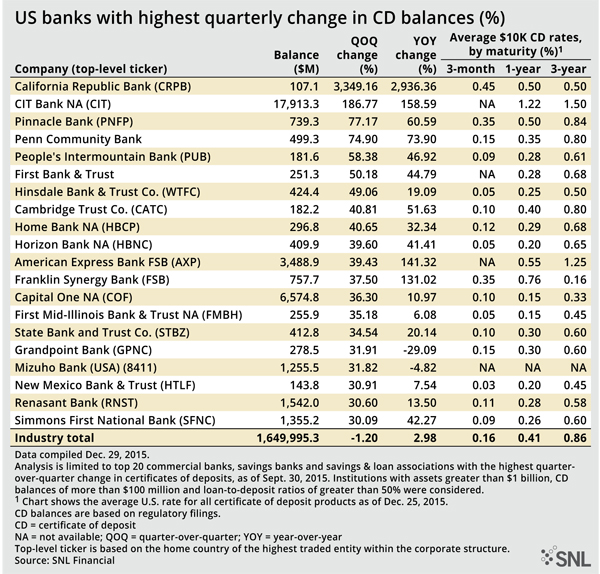

Some banks have reported outsized growth in CDs. SNL found 11 banks—when excluding those that had completed an acquisition in the third quarter—that increased their CD balances by more than 30% from June 30, 2015, to Sept. 30, 2015.

Two big banks sweeten offers to consumers

Some banks are currently running "CD specials," campaigns aimed at building term funding. TCF Financial Corp. is one of those institutions and said the CD campaign aided in deposit growth in the third quarter, but caused the average interest rate on its deposits to rise to 0.31%, up 3 basis points from the prior quarter.

TCF is offering CDs with durations between 10 months and 18 months at prices ranging from 90 basis points to 120 basis points depending on the product and market. TCF said during its third-quarter earnings call that it has seen deposit rates in markets where it competes with banks subject to the LCR be impacted by the rule.

"And so the marketplace as it relates to the bigger banks and some of the LCRs as it relates to building their liquidity, that's been an impact to us as we have seen larger competitors, with longer rates," Michael Jones, then the TCF CFO, said on the call, according to the transcript.

In addition to TCF running special campaigns, Ally Financial Inc. recently rolled out a new tiered CD system, with plans to offer customers different rates based on the amount held in the account. The new tiers took effect Nov. 7 for new and renewal business and set different rates for accounts with less than $5,000; between $5,000 and $24,999.99; and $25,000 or more.

State of CDs at community banks

Notwithstanding the recent efforts by larger banks, their smaller counterparts tend to hold far bigger balances of CDs. But smaller banks did shrink the relative level of CDs on their balance sheets in the third quarter. CDs at banks with assets between $1 billion to $10 billion dipped to a median of 21.2% of deposits at the end of the third quarter from 22.2% at year-end 2014, while banks with less than $1 billion in assets reported that CDs declined to a median of 31.1% of deposits at the end of the third quarter from 32.3% at year-end 2014.

While the relative size of CD balances declined at smaller banks, some institutions increased CD rates in the third quarter even before the Fed raised short-term rates late in 2015. SNL data show that over the last year, average rates across the banking industry for one-, three- and five-year CDs rose 3, 5 and 6 basis points, respectively, as of Jan. 6.

When the Fed increased its federal funds rate to a target range of 0.25% to 0.50% in December 2015, it marked the first rate hike since the credit crisis. Market observers expect the central bank to raise rates by 75 basis points or more in 2016, according to a survey of more than 60 economists conducted by The Wall Street Journal.

Projecting CD trend

If history repeats itself, CDs will increase on bank balance sheets as interest rates rise and the cost of those products will climb. CDs became larger portions of banks' deposit bases during the last tightening cycle, while noninterest bearing deposits declined. Some advisers believe the shift will occur again and many of the funds that flooded into money market accounts in recent years will move to higher-yielding accounts like CDs.

CDs totaled 25.6% of banks' deposits in 2004, but rose to 29.1% of deposits by year-end 2006 after the Fed had increased the target fed funds rate by 400 basis points during that period.

While expectations vary for just how much higher rates will change the composition of banks' deposit bases, most observers believe that CDs will grow and their cost will rise.

Need help getting back into raising deposits? Read consultant Neil Stanley’s “Will ‘deposit atrophy’ strike your bank?”

This article originally appeared on SNL Financial’s website under the title, "Some banks running CD specials, while LCR banks build term funding"

Tagged under ALCO; Mergers Acquisitions; Financial Trends; Risk Management; Rate Risk; Feature; Feature3;

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients