The Other Path to Fintech Fortunes

Roughly speaking, neo-banks have a business model where they spend a dollar to get fifty cents back

- |

- Written by Andrew Steele - Activant Capital

The typical fintech playbook until now has been to build a new tech tool that makes transactions easier, safer, more streamlined, and then sell your tool to the other well-funded tech companies that are promising to be the next generation of banks. Think Chime, Revolut, MoneyLion, Beam, and Trim. These are companies that have collectively raised billions in venture capital.

However, the typical neo-bank makes $10.4 per customer in a year. By contrast, the typical bank (who are unlikely to embrace new technologies) makes $311 per customer per year. This revenue gap wouldn’t be anything to worry about, except for the fact that neo-banks typically spend $21 in marketing and service costs per customer per year. That means, roughly speaking, neo-banks have a business model where they spend a dollar to get fifty cents back.

Even if you get comfortable with their future earnings potential, neo-banks are harder to sell to than you think. Every new fintech startup on earth is lining up to get a meeting with these neo-banks. Simply put, they can’t work with everyone. The “neo-banks” are cool, they are tech-savvy, your investor sits on their boards. But if you are relying on them alone to scale your fintech startup, you’re in for a tough road. So where does this leave fintech founders? Well, it leaves them in search of other, less saturated opportunities.

Luckily for our fearless fintech entrepreneur, the big banks have a cool, rich uncle: credit unions . These are banks with a community feel. Examples are Navy Federal, SchoolsFirst, Alliant, Suncoast, DCU, Teachers Federal, and the Police and Fire Credit Unions. Credit Unions compete against the big banks by focusing on one customer base (teachers, police) and providing more personalized service than big banks can.

You might have read that credit unions are on the decline, that the total number has shrunk from 6,021 to 5,236 in the past 5 years. But what’s not mentioned is their consolidation, their evolution, and their sustained growth in high-value customers.

According to the National Credit Union Association, in the past 5 years, credit unions have added 21.4 million new members to reach over 120 million customers in the US alone. During the same period the “neo-banks” have added roughly the same amount of customers in the United States (our best estimate is around 20-25 million).

New Neobank Customers Since 2015 : 22.5 million

New Credit Union Customers Since 2015: 21.4 million

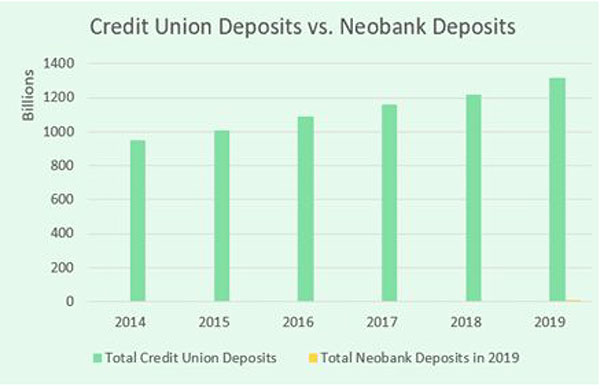

Combining this reach with average deposits tells an even more powerful story. Take a look at the chart below. Do you see that tiny little orange bar in 2019? That’s the total deposits of the top neo-banks compared to the deposits at Credit Unions. If you can’t see it, it’s not because your contact prescription is out of date. It’s because, compared to credit unions, neo-banks barely exist.

Americans are gravitating to credit unions because they see them as more trustworthy, better sources of advice, and more able to fix problems quickly. Credit unions are growing fast. And they are very profitable. Compared to the big banks,credit unions are not nearly as bureaucratic, not as fearful of trying out new tech, and hungrier to offer new services and experiences that help them outcompete the bigger players.

Why are these credit unions so hungry for new tech? Because the big banks they compete against have marketing budgets that would make Don Draper blush, branch coverage from your corner store to Hong Kong, and billion-dollar tech budgets. To the credit unions, the choice is simple: partner with entrepreneurs who make them stand out, or step aside.

Better yet, your venture investor doesn’t know the CEO of these credit unions. So their inbox isn’t flooded with emails from every startup that’s raised venture capital. Instead, credit unions are curious about the latest developments in tech and open to pilots. They want to work with the best fintech entrepreneurs out there. And once you get in the door, they have the scale to help your fintech tool grow. Credit unions can’t afford to keep you busy with multi-year pilots while they build your tool internally. Instead, the only way they can compete effectively with the big banks is by partnering with the best startups out there and bringing those partnerships to every customer they have.

But if our fintech founder wants to get in the door with credit unions, she’s going to need a new approach. Credit Unions don’t want to hear about how your new algorithm or API will transform the future of money transfers. Unlike “neo-banks” credit unions don’t have the luxury of starting from scratch and re-imagining the future of anything. Instead, they are looking for products that tangibly improve their customers’ day-to-day experience and reduce costs. They are looking for cheaper ways to acquire new customers, better ways to deliver customer service, and more helpful, flexible ways to deliver credit.

When you are selling to a Credit Union, start with their customer: a teacher who doesn’t even want to deal with banking. Think about how your product will make that teacher’s life a little bit easier when she needs a loan, or needs to send money to a family member. That teacher doesn’t need anything to be reimagined: she needs things to be a bit simpler, a bit less frustrating, a touch cheaper.

If you can do that, if you can understand the banking needs of everyday Americans, and develop a product that makes things marginally better, the Credit Unions will be interested. They are big customers that can help your new fintech scale in ways the “neo-banks” can’t. They are open to new opportunities.

And now, more than ever, credit unions are capable of adopting new technology. Historically, the credit unions have relied on big tech firms like Fiserv and FIS to build most of the software they use. But the cloud has arrived in banking. Companies like the recently public nCino and the open-sourced Moov have introduced new, flexible, cloud applications that can do what the big, legacy tech firms could do, but better and cheaper. On top of that, companies like Unqork have built no-code platforms that allow credit unions to adopt new tech at the push of the button: no developers needed.

Today, if you want to get in the door at credit unions, you have better options than ever. Fiserv and FIS are eager to keep their combined $150bn market caps, and we’ve seen them begin to partner with startups like never before. Similarly, the new cloud players continue to innovate, and are fast to incorporate the latest fintech tools. Credit unions are open to partnering directly. And, finally, you can integrate your tool into the emerging no-code layer that is quickly gaining adoption at credit unions.

So the bottom line is this: if you want your impressive new algorithm to get media coverage and impress your friends, then target neo-banks. But if you want to build a billion dollar company, focus on the credit unions.

Andrew Steele - Activant Capital

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients