Stressing on Climate Change

Climate Change is the greatest threat of our time and one that cannot be ignored or waited upon

- |

- Written by Ajay Katara, Tata Consultancy Services (TCS)

Climate Change is the greatest threat of our time and one that cannot be ignored or waited upon. Climate change is real and so are the Risks associated with it, it is no surprise that climate change as a topic has catapulted to the forefront for Banking and Insurance Firms today.

Unlike financial risks which have seen multiple crises and matured over a period, climate change is relatively new, and the associated risks are still being understood by the industry.

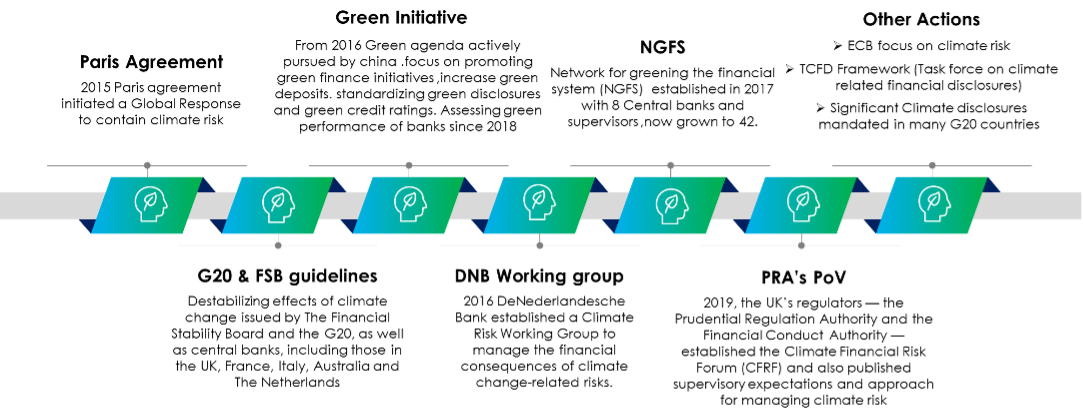

Climate Risk started gaining prominence with the Paris Accord in 2015 and post that many regulatory bodies across the world have started putting pointed efforts in Managing Climate Risk. The below diagram provides a view of key efforts taken so far.

While the above efforts have laid a foundation for the Climate Risk Management Globally, it is also becoming more evident that Banks and Financial institutions will have to brace themselves for Climate related Stress Test soon as supervisors become increasingly cognizant of the exigency in gauging the jeopardies from climate change.

The concept of Stress testing is gaining more prominence especially in UK and EU and the tests promulgated will not test capital adequacy but may lead companies to look more proximately at whether they require to hold more capital to cover potential losses from climate-change jeopardies. Due to the advent of climate change many banks and insurers have also started to rejig their balance sheets and move away from sectors exposed to climate change and move towards financing Go green initiatives.

There are two main Risks in climate change which should ideally be covered in climate change stress scenarios.

- Physical Risk – emanates from climate and weather-related change events, such as floods, heatwaves, floods, storms, and sea level rise, which potentially result in large financial losses, impairing asset values and the creditworthiness of borrowers.

- Transition Risk – Occurs from the process of moving towards a low carbon economy. Changes in Tax policies, technology and laws relate to climate can result in assessment changes for assets and liabilities held, which in turn alters the risk profile of the institution.

The key objective of Climate Change Stress scenarios is to enable Banks and FI’s to better manage and better respond to climate change threats. The results of stress test will enable them to establish remediation measures, develop strategies, maintain sufficient liquidity and capital buffers to better manage the risks emanating from climate change.

The idea of stress testing is also not new to the Banks and FI’s and they already have established stress testing methodologies, model management capabilities and other necessary infrastructure in place which can be easily leveraged to expand the scope of climate related stress test. The critical factors that would need to be considered will be

- Data Availability – Data constitutes a key ingredient in Stress testing activities, while for traditional risk the historical data reflects the areas where they are more exposed to, in case of climate change there are multiple uncertain risk events which have a bearing on it, hence displaying a fat tailed or a heavy tailed distribution which implies that climate related risk under extreme cases will be larger than that observed in typical statistical assumptions. Hence it is imperative to ensure hypothetical data sets are also used as inputs in stress test models and to better assess the risk arising from extreme events.

- Calibrating Existing Business Processes – Climate Change Management must be imbibed in existing Business process which will require changes to existing Business processes. For e.g. In case of Credit Lending, climate related specifics can be bought in to the underwriting process to understand the climate related risk associated with various counterparties in different industries like energy, manufacturing etc.and categorize them into sectors which are more susceptible to climate risk and accordingly monitor and manage them.

- Time Horizon for stress test – Given the complexity and uncertainty over climate changes. The stress Tests in this case would need longer time horizons than financial risks. Many regulators are taking cognizance of this fact and for e.g., ECB climate stress test captures and quantifies its results using a 30-year timeline to take account of the long-run impact.

- Climate Related Scenarios – Apart from Regulatory climate change scenarios which will be published by regulatory authorities, Banks will require to establish idiosyncratic Scenarios and conduct Stress Testing exercise to quantify resilience and susceptibilities with veneration to climate change. It will additionally need to Conduct long term assessments predicated on forecast to avail in strategic orchestrating and decision making.

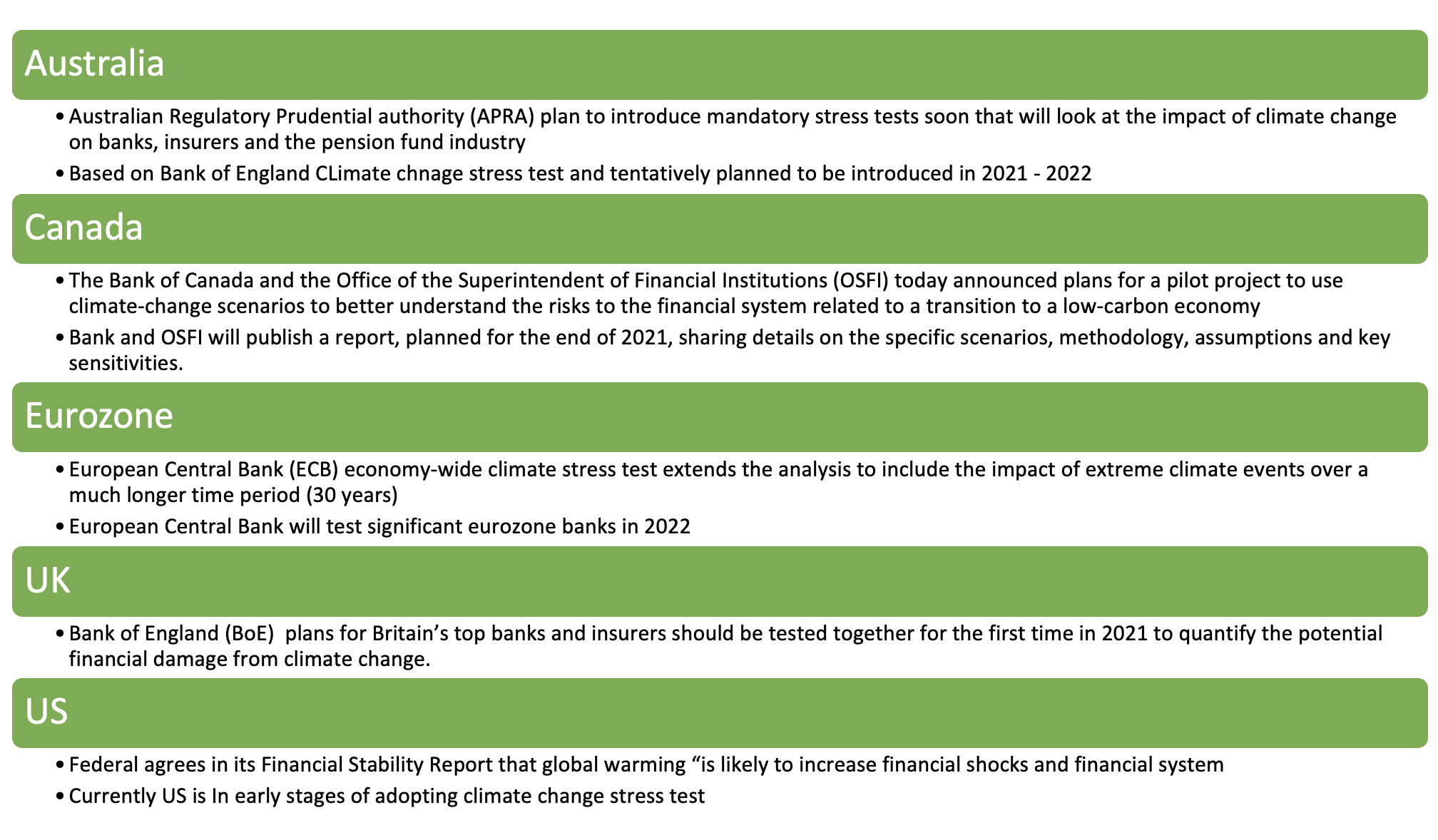

Most of the Regulatory authorities have initiated efforts on climate related stress test, a brief synopsis highlighting the efforts underway in few geographies is provided below.

While the current Regulatory efforts are steps in right direction, lot more efforts need to be put in to get the desired results and a good starting point towards that is to leverage existing Stress testing frameworks related to financial risks.

Post the financial crisis of 2008, stress testing started gaining prominence at a global level and guidelines were issued and implemented across geographies, if we were to look at today’s scenario banks and financial institutions are not starting from scratch and have access to established financial stress testing capabilities which can be leveraged and repurposed to conduct climate related stress test.

Climate change management calls for concentrated efforts from both regulatory authorities and banks alike, as the saying goes Climate Change is happening right now, its impact is real and the time to act is now.

About the Author:

Ajay Katara is a Domain Consultant in Banking Risk Management area at Tata Consultancy Services (TCS). He has extensive experience of more than 15 years in Consulting & Solution design space cutting across CCAR Consulting, AML, Basel II implementation and Credit risk, and has worked with several financial enterprises across geographies.

Related items

- Deutsche Bank Supports $50m Climate Fund for Southeast Asian Agriculture

- Trump Administration Going Light on Bank Exams

- US Pensions Invested $1.5 Trillion in Hedge Funds Last Year

- One-in-Four UK Pension Schemes Consider Reducing US exposure

- Investors Retreat from US Markets Amid Demand for Global Diversification