Weighing your options for cross-selling

Wells Fargo scandal demands a fresh look at how you pay for sales

- |

- Written by Mike Moebs

- |

Which factor ranks in your bank's sales program, a transaction orientation or a relationshiip orientation?

Which factor ranks in your bank's sales program, a transaction orientation or a relationshiip orientation?

In recent weeks we have asked our bloggers to look at the Wells Fargo affair through their specialized viewpoints. Our newest blogger, “The Prairie Economist,” Mike Moebs, continues a theme he began in his inaugural blog.—Steve Cocheo, executive editor and digital content manager

The word “crisis,” in simplified Chinese, translates loosely into two characters meaning “danger” and “opportunity.” The Wells Fargo Bank crisis is an opportunity for financial institutions to evaluate and adjust their own sales process.

An integral component for any successful sales process is compensation structure. Unlike Wells, you must compensate service effort over time, not only for the initial sale but for the ongoing service itself.

Whether your bank’s methodology is transaction-oriented or relationship-oriented, the sales process has to fit your operating style. Compensation will only help improve it. But it is not your strategy.

What will you measure?

Measuring the sales process is also very important. Cross-selling services needs to be constantly evaluated.

Many institutions, like Wells Fargo, have had trouble distinguishing between a service and a feature. (See my previous blog, “Banks sell services, not products.”)

Features like online banking and a debit card come with a checking account. By definition, the account is the centerpiece there. A typical measure of cross-selling looks at checking accounts, deposits, loans, retirement accounts, wealth management accounts, insurance, and securities per customer.

Services must be properly defined with an institution-wide understanding. This will help with the capability to measure and evaluate cross-selling abilities.

While financial service sales are often qualitative, compensation and cross-sell are two metrics which can make service sales more empirical. Incorporating these metrics into a solid sales structure—backed up with standard audits—will help avoid the pitfalls of the Wells Fargo blunders.

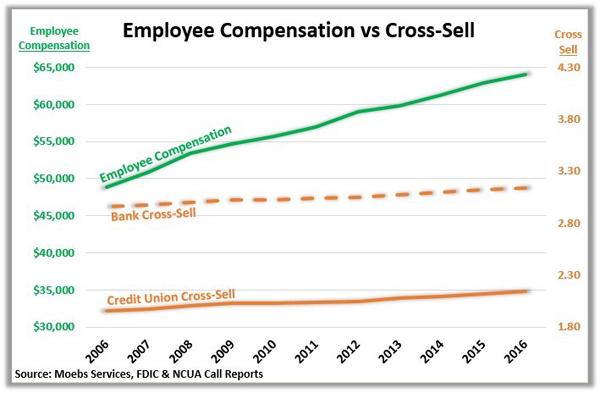

CPI compared to compensation and cross-sell

Average Employee Compensation for banks, thrifts, and credit unions can be measured by dividing the total compensation per institution by the total number of employees per institution.

In 2007, according to my firm’s research, employee compensation for all depositories came to $50,929, growing to $63,996 in the first half of 2016. That’s a 25.7% increase over nearly a 10-year period. During the same time period, cross-selling has been increasing at only 5.6%, a much smaller rate of change.

Employee pay and cross-selling rates of change can be compared to inflation, which expanded at 16.2% from 2007 to 2016.

Thus, compensation grew much faster than both the cross-sell rates and the inflation rate (as expressed by the Consumer Price Index).

However, at 5.6%, the cross-sell rate did not match up to either the pay or inflation rates. This indicates a positive or direct relationship between compensation and CPI, while cross-sell is negative or indirect to CPI.

Compensation does not align with cross-sell rates from 2007 to present day, but reflects more of an inverse relationship.

That means that something is amiss.

Well-executed incentive programs would indicate more compensation comes with more cross-sell. There may be many valid explanations for this. Cross-sell rates are typically higher in expansive economic times, but less in difficult economic conditions, which certainly has been the case for many since the Great Recession started in 2008.

This bears looking into, institution by institution.

Selling methodology: banks versus credit unions

While there are many different selling techniques, two methods lead both banks and credit unions: transaction versus relationship.

• Transaction oriented institutions focus more on securing a large number of checking accounts in order to maximize transaction and interchange revenue.

The focus is on selling the initial service, in this case a checking account, and not on cross-selling or up-selling additional services, such as credit cards or loans. This method can be successful—as long as the overall checking account portfolio is profitable.

• Relationship-oriented institutions, on the other hand, focus more on cross-selling other services.

Instead of relying on checking account volume to create a profitable checking portfolio, this method relies on the sale of other services to offset the checking account costs. This method can be successful if there are enough other services being sold to offset the net costs of the checking account portfolio.

Revealing a fundamental philosophical difference

Often people in financial services speak about credit unions and banks becoming more and more alike. However, frequently this supposed trend is not seen in sales philosophy.

How so? Credit unions typically apply a transaction-oriented marketing strategy. That’s why a majority continue offering the free checking account—to bring in more accounts. Overall, we see that credit union’s cross-sell rate is thus lower than banks because of their focus on account volume, rather than relationship building.

On the other hand, banks are moving away from their primary service being the checking account.

Banks are now focusing more on a relationship-oriented marketing strategy. Other services banks offer alongside the checking account include: large deposits, loans, securities, insurance, retirement accounts, wealth management, and small business accounts.

At many banks, checking is treated as a no-charge secondary account supplementing other services with higher margins.

Banks shifted to a relationship marketing strategy to gain profitability with fewer customers. In contrast, credit unions remained with the more basic strategy of transaction services to gain the maximum number of members.

These different approaches to financial services allow banks to be more sales-oriented, while credit unions remain more order takers.

Weighing comparative performance

The question is, which sales method orientation works best: transaction or relationship?

It solely depends on the operating style of each institution.

There are two critical factors that apply to both approaches:

1. Consumers must have their needs fulfilled with proper selling techniques.

2. Service salespeople must be compensated based on net measures over a period of time.

Compensation in financial services is key

A strong link in the financial service sales process exists between the metrics of selling services and long-term employee compensation. Wells Fargo Bank failed at selling because it rewarded employees immediately instead of enabling them to earn bonuses, incentivizing people over time, and measuring the process to achieve the most important indicator of long-term sales success: satisfied consumers.

Semper,

Mike

Moebs $ervices has a Financial Service Sales webinar on Oct. 27, “Best Practices for Successful Cross-Selling.” Learn more here

Tagged under Human Resources, Mergers Acquisitions, Tokenization, Blogs, The Prairie Economist, Feature, Feature3,

Related items

- Global Instability and Rising Treasury Yields, but Markets Open Higher

- “Stablecoin Strategy” Is a 2026 Question for Banks, Not a 2027 One

- Banks Need to Reconsider their Role in an AI-Driven Future

- Tokenization Could Reshape Financial Markets, Says IMF

- UBS Expands US Banking Push for Affluent Wealth Clients